Mobile Menu Overlay

The White House 1600 Pennsylvania Ave NW Washington, DC 20500

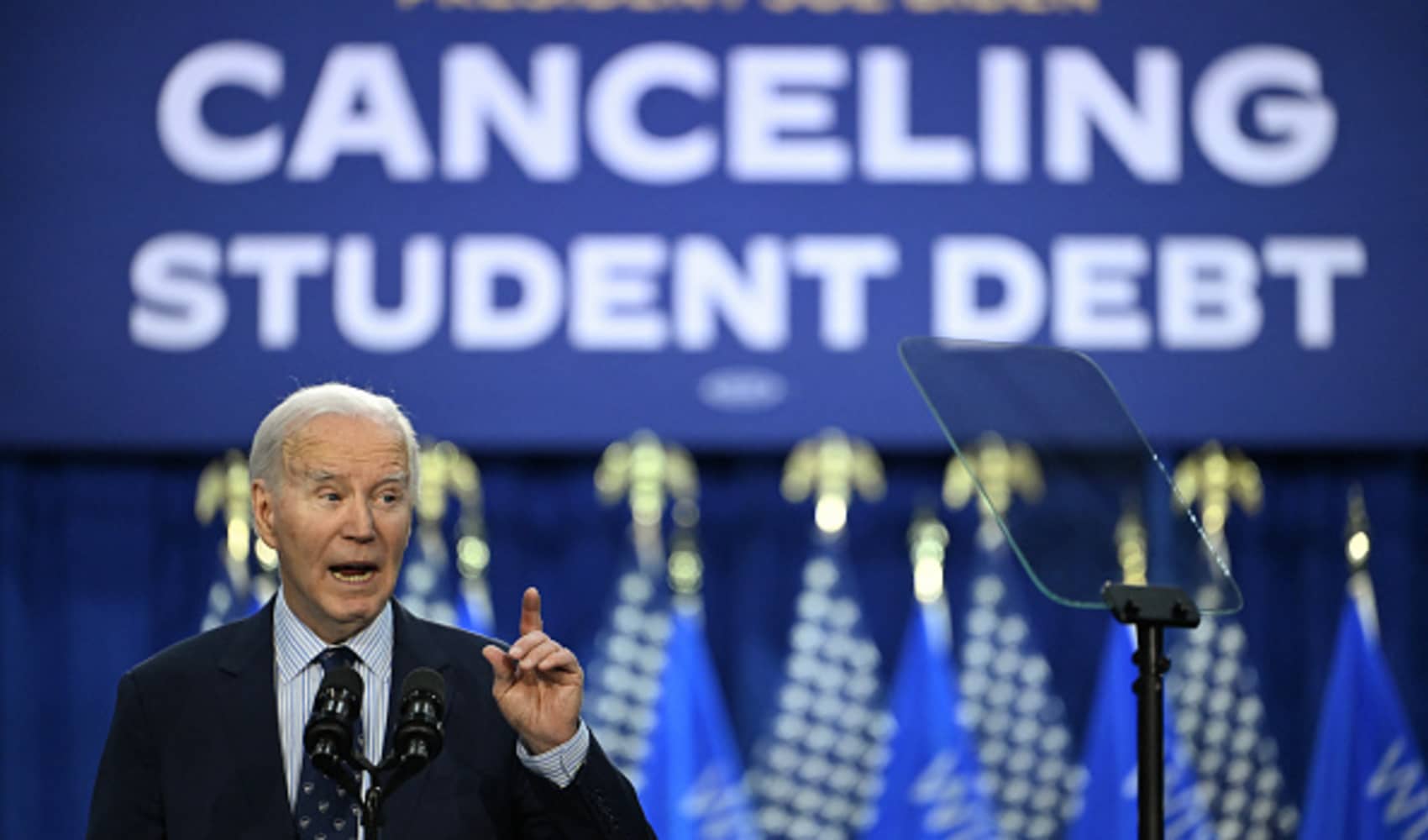

President Joe Biden Outlines New Plans to Deliver Student Debt Relief to Over 30 Million Americans Under the Biden- Harris Administration

Today, Biden-Harris Administration leaders will fan out across the country as President Biden announces his Administration’s new plans to cancel student debt for tens of millions of Americans . The plans, if implemented, would provide debt relief to over 30 million Americans when combined with actions the Biden-Harris Administration has already taken to cancel student debt over the past three years. While Republican elected officials try every which way to block millions of their own constituents from receiving student debt cancellation, President Biden has vowed to use every tool available to cancel student debt for as many borrowers as possible, as quickly as possible. Today, President Biden will travel to Madison, Wisconsin to announce these new plans, while Vice President Harris will travel to Philadelphia, Pennsylvania, Second Gentleman Douglas Emhoff will travel to Phoenix, Arizona, and Secretary of Education Miguel Cardona will travel to New York City to meet with borrowers benefitting from the Administration’s student debt relief actions.

President Biden from Day One has worked to fix the student loan system and make sure higher education is a ticket to the middle class – not a barrier to opportunity – because he knows that debt cancellation not only benefits borrowers, it benefits the entire economy.

To date, the Biden-Harris Administration has approved $146 billion in student debt relief for 4 million Americans through more than two dozen executive actions. That includes fixing Public Service Loan Forgiveness and Income-Driven Repayment plans, so borrowers finally get the relief they are entitled to under the law. It also includes launching the most affordable student loan repayment plan ever – the SAVE plan – which cuts undergraduate loan payments in half, ensures borrowers never see their balance grow from unpaid interest, helps drop millions of borrowers’ monthly payments down to $0, and cancels debt for low-balance borrowers faster. Nearly 8 million borrowers have enrolled in the SAVE plan, 4.5 million borrowers have a monthly payment of $0 under the plan, and an additional 1 million borrowers have a monthly payment of less than $100. The Biden-Administration has also secured the largest increase to Pell Grants in a decade and has taken significant steps to hold colleges accountable for leaving borrowers with mountains of debt and without good job prospects.

Last June, in the wake of the Supreme Court’s decision blocking the Biden-Harris Administration’s original student debt relief plan, President Biden vowed to keep fighting to deliver student debt relief to borrowers held back by the burden of student loan debt. Immediately following that, the Department of Education began pursuing an alternative path to debt relief through negotiated rulemaking under the Higher Education Act.

Today’s announcement lays out the plans the Biden-Harris Administration is pursuing through that effort. In total, these plans would fully eliminate accrued interest for 23 million borrowers, would cancel the full amount of student debt for over 4 million borrowers, and provide more than 10 million borrowers with at least $5,000 in debt relief or more.

Canceling runaway interest for millions of borrowers

More than 25 million borrowers owe more than they originally borrowed, including many who have made years of payments, due to the interest rates on Federal student loans. President Biden will announce plans that, if finalized as proposed, would cancel up to $20,000 of the amount a borrower’s balance has grown due to unpaid interest on their loans after entering repayment, regardless of their income. Low and middle-income borrowers enrolled in the SAVE plan or any other income-driven repayment (IDR) plan would be eligible for the entire amount their balance has grown since entering repayment to be canceled under the Administration’s plans. This group of borrowers includes single borrowers who earn $120,000 or less and married borrowers who earn $240,000 or less. No application will be needed for borrowers to receive this relief if the plan is implemented as proposed.

Millions of the borrowers who could be helped by these plans have continued to see their balances grow because of accrued interest, despite making their monthly payments. Many have also had this unpaid interest capitalized, meaning it is added to their principal balance and borrowers are now paying interest on that higher amount. The Administration’s plan would forgive interest balances built up to date for 25 million borrowers, with 23 million likely to have all of their balance growth forgiven.

This plan builds off the actions the Biden-Harris Administration has already taken to prevent the negative effects of excessive interest accrual on student loans going forward by eliminating all interest capitalization not required by law. The SAVE Plan does not charge unpaid interest for borrowers who make their monthly payments, and has canceled interest for at least 4.5 million borrowers to date.

Automatically canceling debt for borrowers eligible for loan forgiveness under SAVE, PSLF, closed school discharge, or other forgiveness programs but not enrolled

Too many borrowers eligible for relief – including immediate cancellation –have not been able to overcome paperwork requirements, bad advice, or other obstacles. Since its first days in office, the Biden-Harris Administration has worked to get borrowers the relief to which they are entitled.

Today, the Administration is proposing to automatically cancel debt for borrowers otherwise eligible for relief through the SAVE plan, Public Service Loan Forgiveness, or other forgiveness opportunities like closed school loan discharges but who have not successfully applied for that assistance.

Under SAVE, borrowers who originally took out $12,000 or less in loans and have been in repayment for 10 years are eligible to get their remaining debt canceled. For every additional $1,000 in loans they took out (up to $21,000 total for undergraduate loans and $26,000 total for graduate loans), a borrower is eligible for relief after an additional year of repayment. For example, if a borrower took out $13,000 in loans, they would be eligible for debt cancellation after 11 years in repayment.

Under Public Service Loan Forgiveness, borrowers in public service for 10 years who have made 120 months of qualifying payments can get their remaining student debt canceled.

The Administration’s plans would allow the Department of Education to use data it has on hand to identify borrowers otherwise eligible for this type of relief without requiring them to apply for these programs. The Administration expects this action would cancel debt for around 2 million borrowers across the country.

Canceling student debt for borrowers who entered repayment over 20 years ago

More than 2.5 million borrowers have had their share of student loans for two decades or longer and still carry debt from long-ago loans. The Biden-Harris Administration has already cancelled $45.6 billion in student debt so far for nearly 1 million borrowers who have been in repayment for at least 20 years, but never got the relief they were entitled to because of administrative problems with income-driven repayment plans. The Administration’s new proposals, if finalized as proposed, would cancel student debt for borrowers who first entered repayment 20 or more years ago. Borrowers with only undergraduate debt would qualify for forgiveness if they first entered repayment 20 years ago (on or before July 1, 2005), and borrowers with any graduate school debt would qualify if they first entered repayment 25 or more years ago (on or before July 1, 2000). Both Direct Loans and Direct Consolidation Loans that repay only undergraduate study or graduate study for 20 or 25 years respectively are eligible for relief in this proposal. Borrowers would not need to be on an income-driven repayment plan to qualify.

Canceling student debt for borrowers who enrolled in low-financial-value programs

One of the Biden-Harris Administration’s top priorities when it comes to higher education is holding colleges accountable when they leave students with mountains of debt and without good job prospects. To this end, the Department has taken significant steps to crack down on colleges that provide low-value programs to borrowers, when they cheat students and families, and when they close unexpectedly – leaving borrowers and taxpayers to foot the bill.

Today, President Biden is announcing his Administration’s plans that, if finalized as proposed, would cancel student debt for loans associated with institutions or programs that lost their eligibility to participate in the Federal student aid program or were denied recertification because they cheated or took advantage of students. Further, borrowers who attended institutions or programs that closed and failed to provide sufficient value— for example that leave graduates with unaffordable loan payments or earnings no better than what someone with a high school diploma earns— would be eligible for relief under this proposal.

Canceling student debt for borrowers experiencing hardship paying back their loans

President Biden and his Administration recognize that the current student loan system and repayment programs don’t reach all borrowers, and for many Americans student loans continue to be a barrier for them participating in the economy, accessing economic mobility, or pursuing their dreams. The Administration’s plan for student debt relief will also include a plan that would cancel student debt for borrowers experiencing hardship in their daily lives that prevents them from fully paying back their loans now or in the future.

This plan could provide relief to millions of borrowers who experience hardship—such as borrowers who are at high risk of defaulting on their student loans, who could be eligible for automatic relief, or families who are burdened with other expenses like medical debt or child care who can apply for relief in the future.

Providing relief to millions of borrowers this year

The Biden-Harris Administration plans to release proposed rules on these plans over the coming months. If these plans are finalized as proposed, this fall the Administration would begin canceling up to $20,000 in interest for millions of borrowers and full loan forgiveness for millions more.

Building off unparalleled record canceling student debt under President Biden

Today’s announcements follow historic actions the President and his Administration have already taken to approve student debt cancellation for nearly 4 million Americans and make student loan payments easier for millions more through the SAVE plan. These actions have benefited borrowers from all 50 states and U.S. territories, borrowers from different walks of life, and borrowers of all ages. To date:

- The Administration has canceled over $62.5 billion in student debt for 871,000 public service workers, including teachers, firefighters, nurses, and more. Prior to the Biden Administration, only 7,000 people in total had received debt forgiveness through Public Service Loan Forgiveness in the over 15 years since the program was put in place. The Biden Administration implemented fixes to make sure public service workers received the relief they are entitled to under the law, helping nearly 900,000 public service workers receive relief to date.

- The Administration has approved $45.6 billion in debt cancellation for nearly 1 million borrowers through fixes to income-driven repayment. For too long, as a result of administrative failures and loan servicer errors, borrowers never got credit for being in repayment. The Biden-Harris Administration fixed that, and has approved debt cancellation for over 930,000 borrowers who have been in repayment for over 20 years.

- The Administration has approved $22.5 billion in debt cancellation for borrowers cheated by their schools, who saw their schools abruptly close, or who were covered by related court settlements. The Administration has approved borrower defense and closed school discharges to provide debt cancellation for students that attended and were cheated by for-profit institutions like Corinthian Colleges and ITT Technical Institute. Less than $600 million in debt relief had been approved through borrower defense, closed school discharges, and related court settlements from all prior administrations combined, compared to the $22.5 billion approved under the Biden-Harris Administration alone.

- The Administration has approved $14 billion in debt cancellation for over 548,000 borrowers with a total and permanent disability. Through automatic matches with the Social Security Administration and other actions, the Biden-Harris Administration has approved debt cancellation for over half a million borrowers with total and permanent disabilities.

- The Administration launched the SAVE plan – helping borrowers of all ages and walks of life manage their monthly payments, not charging interest for millions of borrowers, and setting $0 payments for 4.5 million borrowers every month. To date, nearly 8 million borrowers have enrolled in SAVE, and 4.5 million of them have a monthly payment of $0, meaning they are also not accumulating interest that would otherwise be due. An additional million borrowers have a monthly payment of less than $100. Already the Administration has canceled debt for 153,000 borrowers enrolled in SAVE who took out low balances and have been in repayment for at least 10 years. And in July, the SAVE plan will cap monthly payments for undergraduate loans at 5% of income compared to the 10% threshold now – which will save many young borrowers money on their monthly payments. The Administration continues to encourage borrowers to sign up for the SAVE plan at studentaid.gov/SAVE to save money on their monthly payments and reach loan forgiveness faster.

- The Administration secured the largest increase to Pell Grants in a decade, and has expanded eligibility for the maximum Pell Grant to 1.7 million more Americans. The President has taken historic steps to bring college in reach for more Americans, including low-income Americans. The President secured the largest increase to Pell Grants in a decade, expanded eligibility to Pell to 665,000 new students, and expanded eligibility for the maximum Pell Grant to 1.7 million more students. The President has also proposed making community college free so more Americans can access the promise of higher education.

President Biden will not stop fighting to cancel more student debt for as many Americans as possible, and today’s announcements are a key step forward in that effort.

Stay Connected

We'll be in touch with the latest information on how President Biden and his administration are working for the American people, as well as ways you can get involved and help our country build back better.

Opt in to send and receive text messages from President Biden.

More From Forbes

5 student loan forgiveness application updates borrowers should know about.

- Share to Facebook

- Share to Twitter

- Share to Linkedin

US Education Secretary Miguel Cardona (R) looks on as US President Joe Biden delivers remarks on ... [+] student loan forgiveness in the South Court Auditorium of the Eisenhower Executive Office Building, next to the White House, in Washington, DC, on October 17, 2022. (Photo by Brendan SMIALOWSKI / AFP) (Photo by BRENDAN SMIALOWSKI/AFP via Getty Images)

The Biden administration has approved an unprecedented amount of student loan forgiveness for more than four million borrowers, and more relief may be on the way. But there have been many changes and updates to student debt programs and application processes, with some big updates in just the last few weeks. Navigating the already-complex student loan system amid this tumult can present challenges.

President Biden has taken a two-track approach to enacting broad student debt relief. He has implemented a number of program changes and temporary waivers to several existing loan forgiveness programs. Collectively, these “targeted” initiatives have led to $153 billion in student loan forgiveness. At the same time, the administration has been moving forward with a new student debt relief program that, if implemented, could dramatically expand these approvals . The Education Department released draft regulations for this new program last week. The plan must clear a few more steps before relief would be available, but that could happen this fall.

Here’s what borrowers need to know about applying for current and forthcoming student loan forgiveness initiatives.

Applying For Student Loan Forgiveness Under the Account Adjustment

The Biden administration has approved upwards of $49 billion in loan forgiveness for just under a million borrowers under the IDR Account Adjustment. This temporary initiative can accelerate progress toward loan forgiveness under income-driven plans, a type of federal student loan repayment plan that allows borrowers to make payments based on a formula applied to their income.

IDR enrollees can typically qualify for a discharge after 20 or 25 years in repayment, depending on their specific circumstances. The account adjustment allows past loan periods that may not have counted toward IDR loan forgiveness — such as payments made under other plans, and certain periods of deferment and forbearance — to count.

Microsoft Warns Windows Users Of Ongoing Russian Hack Attack

New apple id password reset issue hitting iphone ipad and macbook users, new ios 18 ai security move changes the game for all iphone users.

There is no formal application for student loan forgiveness under the IDR Account Adjustment. The Education Department is implementing the relief automatically for borrowers who have government-held federal student loans . The department has been approving discharges on a rolling basis every two months, and expects to complete implementation this July.

But some borrowers will need to submit some type of application in order to qualify for relief under the adjustment:

- Borrowers who have federal student loans not directly owned or held by the Education Department — such as commercial FFEL loans, school-issued Perkins loans, and HEAL loans for medical professionals — must submit a Direct consolidation application by April 30th in order to receive the benefits of the IDR Account Adjustment. This represents the most recent deadline extension by the department. As of this writing, the department has not extended the deadline again, suggesting April 30th is the final submission cutoff.

- Those who expect to receive IDR credit under the adjustment but will be short of the threshold for immediate loan forgiveness would need to apply to switch to an IDR plan (if they are not already in one) so they can continue progressing toward an eventual discharge.

The Direct consolidation and IDR applications can be accessed online at StudentAid.gov .

Applying For Student Loan Forgiveness Through PSLF

The Public Service Loan Forgiveness program can shorten a borrower’s student loan forgiveness timeline to as little as 10 years if they work in qualifying nonprofit or public employment. The Biden administration has made meaningful changes to the PSLF program through a combination of temporary waivers and more-lasting regulatory reforms, resulting in 876,000 borrowers getting approved for over $60 billion in loan forgiveness, according to the Education Department.

Only Direct loans qualify for PSLF, meaning borrowers who have non-Direct federal student loans would need to apply to consolidate through the Direct loan program. And borrowers seeking PSLF credit under the IDR Account Adjustment would need to do this prior to April 30th.

In addition, to get PSLF credit borrowers must certify their employment using the online PSLF application system. However, the entire PSLF application and processing system is temporarily shutting down starting on May 1st. During that time, borrowers can submit PSLF forms, but they will not be processed and no one will get student loan forgiveness under the program until processing resumes in July. At that time, borrowers will be able to access their PSLF information through a new StudentAid.gov dashboard.

Applying For Student Loan Forgiveness Based On A Borrower’s Medical Condition

Close to 550,000 borrowers have received $14.1 billion in student loan forgiveness due to changes and improvements to the Total and Permanent Disability discharge program, according to the Education Department. The TPD discharge program can wipe out the federal student loan debt for those who are unable to maintain significant employment due to a disabling medical condition, whether physical or psychological.

The Biden administration recently updated the TPD discharge application to reflect new regulations that went into effect last summer. The reforms expand the types of medical providers who can certify that a borrower meets the TPD standard, and broaden the categories of people who can qualify for automatic relief based on receiving Social Security disability benefits.

The TPD discharge program will likely go through an application processing pause similar to PSLF later this year, although the administration has not yet provided a specific timeline.

Applying For Student Loan Forgiveness Through Borrower Defense To Repayment

The Education Department has approved upwards of $22 billion in student loan forgiveness for more than a million borrowers who were subject to certain types of school misconduct. A portion of that relief was approved through the Borrower Defense to Repayment program, with allows borrowers to request a discharge if their school misled them about core elements of their degree or certificate program.

The Borrower Defense program typically requires a long application detailing how the school engaged in misrepresentations. The Biden administration updated regulations governing the program last summer, providing additional avenues for relief and removing some previous restrictions (such as a statute of limitations) that could have blocked some borrowers from receiving any loan forgiveness under the program.

But a legal challenge has resulted in those new regulations being blocked. In a ruling earlier this month, a federal appeals court suggested that these new, more borrower-favorable rules are likely to ultimately get struck down . That puts the Education Department in a bind — officials cannot currently use the new regulations when evaluating Borrower Defense applications because of the court injunction, but they don’t necessarily want to deny people under the older set of rules while the legal process plays out (unless they have to under other court orders).

Consequently, many applications for student loan forgiveness under Borrower Defense are effectively stuck in a limbo status. Borrowers can apply, but they may not get a decision for quite some time.

“The Department will not adjudicate any borrower defense applications under the latest rule unless and until the effective date is reinstated,” says the department. “While this injunction is in effect, borrowers may still apply online for borrower defense relief. The Department will continue to adjudicate borrower defense applications using an earlier version of the regulations where required under a court settlement.”

Applying For Forthcoming Biden Student Loan Forgiveness Plan

Earlier this month, President Biden announced that a new student loan forgiveness plan is coming. The new initiative, billed as a replacement for the one that the Supreme Court struck down last year, is designed to provide relief to several groups of borrowers based on their circumstances.

According to draft regulations, many borrowers could receive loan forgiveness automatically under the new program, without needing to submit an application. This includes those who have experienced significant compounded interest , borrowers who first entered repayment 20 or 25 years ago, and people who would be eligible for loan forgiveness under other programs but haven’t applied or enrolled.

Other borrowers, such as those experiencing financial hardship, will likely need to submit an application for loan forgiveness. However, that application is not yet available. The new program must first undergo several more steps, including completing a public comment period followed by the adoption of the final version of the rules. Officials have indicated that the program, and any associated loan forgiveness application, could launch by this fall, although it will almost certainly face legal challenges.

- Editorial Standards

- Reprints & Permissions

Student loan forgiveness: What you need to know before April 30

To be eligible for cancellation of your debt, you might have to first consolidate your loans., by noreen o'donnell • published 2 hours ago.

A key deadline is approaching fast for an opportunity for a student loan cancellation.

If you are a federal student loan borrower you could have the chance to receive a full cancellation of your debt or credit towards cancellation through a one-time U.S. Department of Education payment-count adjustment. But to be eligible you might have to first consolidate your loans.

And you must take that step by Tuesday, April 30.

The Biden administration is cancelling federal student debt for millions of undergraduate or graduate students and providing some relief to millions of others. In all more than 30 million Americans will benefit, according to NBC News.

Get Tri-state area news and weather forecasts to your inbox. Sign up for NBC New York newsletters.

More than four million borrowers will have the full amount of their student debt cancelled, 10 million will be eligible for at least $5,000 in debt relief and 23 million borrowers will see their accrued interest eliminated.

The U.S. Department of Education will make the one-time adjustment over summer.

Here’s what you need to know.

US & World

As more borrowers qualify for student loan forgiveness, incoming college freshmen are set to rack up $37,000 in new debt, report finds

Here's why Biden administration believes new student loan forgiveness plan will survive legal challenges

40-year-old delivers for DoorDash to help pay down her $100,000 student loan debt—on top of her full-time job

What loans must be consolidated.

If you have any of the federally managed loans that are listed here, you must consolidate them to get the most credit toward loan cancellation.

- Commercially held Federal Education Loans or FFELs.

- Parent PLUS loans

- Perkins loans

- Health Education Assistance Loan Program or HEAL loans

If you are not sure about what kind of loan you have, log in to your account at StudentAid.gov or call the U.S. Department of Education’s Federal Student Aid Information Center at 1-800-433-3243.

Your new Direct Consolidation Loan will be eligible for the one-time adjustment this summer.

When is the deadline to consolidate?

Tuesday, April 30.

In the News

Student loan borrowers could have up to $20,000 in interest forgiven as early as this fall—here's who qualifies

Millions of older adults with student debt are at risk of losing some Social Security benefits, lawmakers warn

Women with student loan debt face ‘multiple financial pressures,' expert says. These tips may help with repayment

How do i apply to consolidate my loans.

Sign on to StudentAid.gov/loan-consolidation to choose the loans you want to consolidate and determine a monthly repayment plan for your new loan. You can also get help at the Federal Student Aid Information Center at 1-800-433-3243.

There is no application fee.

Some special details about Parent PLUS loans

If you have made at least 25 years or 300 months of repayment toward your Parent PLUS loan managed by the U.S. Department of Education, your loan will be cancelled automatically as part of the one-time adjustment. Otherwise you should consolidate the loan.

This article tagged under:

- Skip to main content

- Keyboard shortcuts for audio player

Is it fair to forgive student loans? Examining 3 of the arguments of a heated debate

Scott Horsley

Student loan borrowers stage a rally in front of The White House on Aug. 25 to celebrate President Biden cancelling student debt. The plan has sparked heated debate, including about its economic fairness. Paul Morigi/Getty Images for We the 45m hide caption

Student loan borrowers stage a rally in front of The White House on Aug. 25 to celebrate President Biden cancelling student debt. The plan has sparked heated debate, including about its economic fairness.

President Biden's plan to forgive hundreds of billions of dollars in student debt is sparking heated debate.

Biden last week announced plans to forgive up to $20,000 in federal student loan debt for Pell Grant recipients and up to $10,000 for others who qualify.

The news will provide relief for borrowers at a time when the cost of higher education has surged.

Student loan forgiveness is politically popular. But not all Democrats are on board

But critics are questioning the fairness of the plan and warn about the potential impact on inflation should the students with the forgiven loans increase their spending.

Here are three key arguments – for and against the wisdom of Biden's decision.

Raising living standards or adding fuel to inflation?

Undoubtedly, student debt is a big burden for a lot of people.

Under Biden's plan, 43 million people stand to have their loan payments reduced, while 20 million would have their debt forgiven altogether.

People whose payments are cut or eliminated should have more money to spend elsewhere – maybe to buy a car, put a down payment on a house or even put money aside for their own kids' college savings plan. So the debt forgiveness has the potential to raise the living standard for tens of millions of people.

Critics, however, say that additional spending power would just pour more gasoline on the inflationary fire in an economy where businesses are already struggling to keep up with consumer demand.

Inflation remains near its highest rate in 40 years and the Federal Reserve is moving to aggressively raise interest rates in hopes of bringing prices back under control.

Not all economists believe the debt forgiveness will do much to fuel inflation.

Debt forgiveness is not like the $1200 relief checks the government sent out last year, which some experts say added to inflationary pressure. Borrowers won't suddenly have $20,000 deposited in their bank accounts. Instead, they'll be relieved of making loan payments over many years.

President Biden announces student loan relief in the Roosevelt Room of the White House in Washington, D.C. on Aug. 24. Olivier Douliery/AFP via Getty Images hide caption

President Biden announces student loan relief in the Roosevelt Room of the White House in Washington, D.C. on Aug. 24.

Because the relief is dribbled out slowly, Ali Bustamante, who's with left-leaning Roosevelt Institute says Biden's move won't move the needle on inflation very much.

"It's just really a drop in the bucket when it come to just the massive level of consumer spending in our very service- and consumer-driven economy," he says.

The White House also notes that borrowers who still have outstanding student debt will have to start making payments again next year. Those payments have been on hold throughout the pandemic.

Restarting them will take money out of borrower's pockets, offsetting some of the additional spending power that comes from loan forgiveness.

Helping lower income Americans or a sop to the rich?

Another big point of contention has to do with fairness.

Forgiving loans would would effectively transfer hundreds of billions of dollars in debt from individuals and families to the federal government, and ultimately, the taxpayers.

Some believe that transfer effectively penalizes people who scrimped and saved to pay for college, as well as the majority of Americans who don't go to college.

They might not mind subsidizing a newly minted social worker, making $25,000 a year. But they might bristle at underwriting debt relief for a business school graduate who's about to go to Wall Street and earn six figures.

Students from George Washington University wear their graduation gowns outside of the White House in Washington, D.C, on May 18. Economists worry President Biden's plan to forgive student loans could encourage more people to take on debt in the hopes of also being forgiven. Stefani Reynolds/AFP via Getty Images hide caption

Students from George Washington University wear their graduation gowns outside of the White House in Washington, D.C, on May 18. Economists worry President Biden's plan to forgive student loans could encourage more people to take on debt in the hopes of also being forgiven.

The White House estimates 90% of the debt relief would go to people making under $75,000 a year. Lower-income borrowers who qualified for Pell Grants in college are eligible for twice as much debt forgiveness as other borrowers.

But individuals making as much as $125,000 and couples making up to $250,000 are eligible for some debt forgiveness. Subsidizing college for those upper-income borrowers might rub people the wrong way.

"I still think a lot of this benefit is going to go to doctors, lawyers, MBAs, other graduates that have very high earnings potential and may even have very high earnings this year already," says Marc Goldwein senior policy director at the Committee for a Responsible Federal Budget.

Helping those in need or making college tuition worse?

Goldwein also complains that the loan forgiveness doesn't address the larger problem of soaring college tuition costs.

In fact, he suggests, it might make that problem worse — like a Band-Aid that masks a more serious infection underneath.

For years, the cost of college education has risen much faster than inflation, which is one reason student debt has exploded.

And now what? The question that follows Biden's student loan forgiveness plan

By forgiving some of that debt, the government will provide relief to current and former students.

But Goldwein says the government might encourage future students to take on even more debt, while doing little to instill cost discipline at schools.

"People are going to assume there's a likelihood that debt is canceled again and again," Goldwein says. "And if you assume there's a likelihood it's canceled, you're going to be more likely to take out more debt up front. That's going to give colleges more pricing power to raise tuition without pressure and to offer more low-value degrees."

The old rule in economics is when the government subsidizes something, you tend to get more of it. And that includes high tuition and college debt.

- student debt forgiveness

- student loans

- student loan debt

- college tuition

Biden's piecemeal student debt forgiveness 'transformational' for borrowers, advocates say

April 23 (UPI) -- In less than a year since the U.S. Supreme Court blocked President Joe Biden's student loan forgiveness, his administration has taken a piecemeal approach to forgiving billions of dollars in debt for millions of borrowers.

The president initially set out to cancel $10,000 to $20,000 of student debt for borrowers who received Pell Grants if they earned less than $125,000 per year. Tens of millions signed up for debt relief before the Supreme Court ruled against the plan in June.

Biden and the Department of Education have since announced more narrowly targeted debt cancellations for borrowers that meet certain requirements. Many who have had their debt canceled have been paying off their student loans for 10 years or more.

As of April 12, the White House said its efforts have resulted in $153 billion in debt relief for 4.3 million borrowers.

Fixing broken programs

Among the most impactful forms of relief, according to borrower advocates, were fixing the Public Service Loan Forgiveness and income-driven repayment programs.

The PSLF program was instituted in 2007 and was set to become active in 2017. It would allow borrowers who made 120 payments while working in public service to have their remaining balance forgiven.

Spencer Dixon, senior policy advisor for the Student Debt Crisis Center, told UPI, however, that the "program was so poorly managed" under President Donald Trump's administration that "only 7,000 people received relief under the program."

"Under Biden so far we've seen more than 100 times as many people benefit from the program," Dixon said.

In October 2022, the Department of Education announced permanent changes to the PSLF program including allowing borrowers working in the public service fields to obtain credit for late, partial or lump sum payments as well as offering credit for months in deferment or forbearance including those related to military service or deferments for economic hardship or cancer treatment.

Following a series of loan discharges the administration said it has since approved $62.8 billion in forgiveness for nearly 876,000 borrowers through the PSLF program.

As of April 12 , the Education Department said that more than 996,000 borrowers have also received relief under additional fixes to IDR programs with the administration approving $49.2 billion in debt relief.

The first relief announcement , following the Supreme Court's decision to block Biden's broader debt cancellation plan, was made on July 14. The Department of Education announced it would notify more than 804,000 borrowers that they qualified to have a total of $39 billion forgiven.

This batch of cancellations took place automatically. Borrowers that had made 240-300 monthly payments, the equivalent of 20-25 years on an IDR plan.

Additionally, in response to the Supreme Court's rejection of his broader student debt relief plan, Biden introduced the Saving on a Valuable Education Plan, or SAVE, which offers automatic relief to borrowers who have been making payments for more than 10 years if they initially took out loans of $12,000 or less.

In February, SAVE borrowers began receiving forgiveness ahead of the originally planned July deadline with $1.2 billion in loans forgiven, impacting nearly 153,000 people . The Education Department said more borrowers will eventually be forgiven as they hit the 10-year repayment threshold. There are about 7.5 million people signed up for the SAVE repayment plan.

In total, the Education Department said $3.6 billion loans for almost 206,800 borrowers have been forgiven under the program as of this month.

'This is transformational'

Repayment flexibility and debt relief have particularly benefited workers in the nonprofit world and government workers, according to Dixon. Lower- and middle-income families and Black and Latino families are also represented among those to be greatly impacted.

The Biden administration has emphasized debt relief for public service workers. Days after announcing the early SAVE plan forgiveness in January, the Biden administration canceled $5 billion for 74,000 public service workers . Teachers, nurses, firefighters and other public servants benefitted.

About 30,000 of those borrowers had been paying their student loans for 20 years. The rest had been paying for 10 years.

Debt relief has been crucial for educators, whether they are just starting their careers or nearing retirement. Becky Pringle, president of the National Education Association, told UPI that the impact for educators has been almost immediate.

"The early career educators who are taking two or three jobs and living with their colleagues in an apartment, all of that is real," Pringle said. "When that changes for them, they tell us about how it not only encouraged them to stay in the profession but that they can live their lives and start their families."

Pringle added that borrowers are often mischaracterized by opponents of debt relief as not paying their loans. However, those who have received relief have been paying toward their debt for 10 years or more in most cases. Some who have paid for a decade or longer had balances larger than their initial loan.

"They've been [paying] it but can't get out from under it because of the way it was structured," she said. "We found out that over 25% of educators over 61 had still not paid off their student loans. About 35% were carrying more than 45,000 of their debt."

Those debt terms have caused some of those educators to delay retirement or believe that retirement will never be an option.

"That's unbelievable and unacceptable," Pringle said.

Pringle and Amy Czulada, outreach and advocacy manager for the Student Borrower Protection Center, told UPI that student debt has caused many people to delay starting a family or purchasing a home.

"We were surprised to find out how many of our members were delaying starting families or buying houses because they were laboring under this debt," Pringle said."

With relief, Czulada says those people can begin to participate in the economy in a way they were not able to before.

"It's been a really exciting time to be doing this work," Czulada said. "It's the first time we've seen the ledger move down on student debt. In the past decade it's been ballooning. The stories we get from folks about what debt cancellation means to them are really inspiring. They're freer to do things they've wanted to do for a long time. This is transformational."

While the Biden administration has rolled out multiple efforts to broaden debt relief it is also seeking to implement a broader plan like originally intended. Last week it submitted a notice of proposal to waive certain student debt under the authority of the Higher Education Act.

"The plans, if implemented, would provide debt relief to over 30 million Americans when combined with actions the Biden-Harris Administration has already taken to cancel student debt over the past three years," the White House said in a statement.

"This plan b broad-based forgiveness is more targeted," Dixon said. "A reasonable person could say that it's in response to the way in which the first plan was struck down."

Czulada explains that this new proposal would seek to fill some gaps for those who have been missed by previous relief plans. It would also fix more programs that have not been working as intended.

The proposal would introduce a number of new regulations that would lower the debt burden for borrowers who have been making payments, experienced hardship or may have qualified for relief without knowing about it.

A portion of debt, or in some cases the full amount, could be waived if it exceeds the amount of the loan when it entered repayment if the borrower falls at or below certain income levels. Borrowers who were eligible for plans like the IDR plan could have their outstanding balance forgiven even if they are not enrolled.

However, Biden's piecemeal debt forgiveness plans have also come under fire.

Kansas Attorney General Kris Kobach has been among the most ardent opponents of canceling student debt. He organized a coalition of 11 states last month to sue the Biden administration over his efforts to forgive student debt. Alabama, Alaska, Idaho, Iowa, Louisiana, Montana, Nebraska, South Carolina, Texas and Utah joined the lawsuit.

Kobach alleges that Biden's plans have defied the Supreme Court's ruling and circumvented Congress.

Borrowers, don’t miss this important student loan forgiveness deadline

The deadline to consolidate student loans by april 30 is looming..

This is the season of college-related deadlines.

By May, colleges typically ask students to confirm which schools they will attend in the fall.

To be considered for federal student aid for the 2024-2025 academic year, applicants have to complete their Free Application for Federal Student Aid ( FAFSA ) form by June 30.

However, another important deadline is approaching for families already dealing with education debt. If you have student loans, meeting this April 30 deadline could result in thousands of dollars in loan forgiveness. Here’s what you need to know.

Get Michelle’s advice free in your inbox

B.O.M. — The best of Michelle Singletary on personal finance

If you have a personal finance question for Washington Post columnist Michelle Singletary, please call 1-855-ASK-POST (1-855-275-7678).

My mortgage payoff story: My husband and I paid off the house in the spring of 2023 thanks to making extra payments and taking advantage of a mortgage recast . Even though it lowered my perfect 850 credit score and my column about it sparked some serious debate with readers, it was one of the best financial decisions I’ve made.

Credit card debt: If you’re in the habit of carrying credit card debt, stop. It’s just a myth that it will boost your credit score. For those looking to get out of credit card debt, see if a balance transfer is right for you.

Money moves for life: For a more sweeping overview of my timeless money advice, see Michelle Singletary’s Money Milestones . The interactive package offers guidance for every life stage, whether you’re just starting out in your career or planning for retirement. You can also purchase a copy for yourself or as a gift.

Test yourself: Not rich and wondering what it’ll take to build your wealth? Take this quiz for my wealth-building tips.

- Bankruptcy Basics

- Chapter 11 Bankruptcy

- Chapter 13 Bankruptcy

- Chapter 7 Bankruptcy

- Debt Collectors and Consumer Rights

- Divorce and Bankruptcy

- Going to Court

- Property & Exemptions

- Student Loans

- Taxes and Bankruptcy

- Wage Garnishment

Debt Forgiveness: The Options & Consequences

5 minute read • Upsolve is a nonprofit that helps you get out of debt with education and free debt relief tools, like our bankruptcy filing tool. Think TurboTax for bankruptcy. Get free education, customer support, and community. Featured in Forbes 4x and funded by institutions like Harvard University so we'll never ask you for a credit card. Explore our free tool

Debt forgiveness is when one of your lenders forgives or erases some or all of your debt. This debt could be from a credit card, a student loan, or an installment loan. Sometimes you can get a full debt forgiven, but more often, you’ll get partial forgiveness. For example, if you come to a debt settlement agreement with a credit card company, you agree to pay part of your outstanding debt in exchange for having the rest of the debt erased. With many student loan forgiveness programs, you must pay a portion of your debt for a certain period of time before you get the remaining balance forgiven.

Written by Attorney Tina Tran . Updated June 28, 2023

What Is Debt Forgiveness & How Does It Work?

Debt forgiveness is when one of your lenders forgives or erases some or all of your debt . This debt could be from a credit card, a student loan, or an installment loan. Sometimes you can get a full debt forgiven, but more often, you’ll get partial forgiveness. For example, if you come to a debt settlement agreement with a credit card company, you agree to pay part of your outstanding debt in exchange for having the rest of the debt erased.

Debt forgiveness isn’t always easy to come by. Usually, lenders that offer loan forgiveness programs have eligibility requirements. To determine whether and how much of your debt to forgive, your lender will consider your financial circumstances and how much debt you owe.

Debt forgiveness is usually available for unsecured debts like credit cards, personal loans, or student loans. Secured debts like a mortgage or a car loan are not usually eligible for debt forgiveness. If you default on a secured debt, the lender will likely pursue foreclosure or repossession . If you are having difficulty paying the minimum payments on your secured debts, you should look at options like loan modification , a forbearance agreement, refinancing, or bankruptcy .

How Do You Get Debt Forgiveness?

Some people can get debt forgiveness by directly contacting and negotiating with their lenders. Other people prefer to hire a credit counselor , debt settlement company, or debt relief agency to help them manage their monthly payments, negotiate debt settlement agreements or lower interest rates, or get a debt consolidation loan.

When it comes to federal student loan debt relief, StudentAid.gov has the latest information on student loan forgiveness programs. The status of the student loan forgiveness plan and repayment options for federal student loans changes frequently. So pay attention to the news or subscribe to the U.S. Department of Education’s email list to stay caught up on the latest developments that could affect your student loans.

Upsolve Member Experiences

What Are the Pros and Cons of Debt Forgiveness?

Debt forgiveness can help relieve financial stress and may be the ticket to shoring up your finances. But it can be difficult to get and has some consequences you’ll want to consider.

Also, when it comes to debt relief of any kind, be aware of scams . Scam phone calls for student loan debt forgiveness have been on the rise in recent years, and several unreputable companies try to make money off people seeking debt forgiveness for credit card and other debt.

The Benefits of Debt Forgiveness

You can probably guess the biggest benefit of debt forgiveness: You no longer have to repay what was probably a quite burdensome debt. Even if you agree to a debt settlement and only have part of your debt forgiven, you benefit by paying less than the total amount you owed.

Getting into debt can become a vicious cycle. If you’re struggling to repay one debt, odds are good that there are other debts you’re trying to manage as well. Having one debt forgiven can free up the resources to pay down other debts, avoid debt collection , or get on the path to becoming debt-free . If you have a debt management plan , debt forgiveness can expedite your plan and help you pay off your debt even sooner than expected.

The Downsides of Debt Forgiveness

As with most things in life, debt forgiveness has some downsides. You may see a dip in your credit score or have a bigger tax bill.

Your Credit Score May Drop as a Result of Debt Forgiveness or Settlement

Depending on the type of debt and type of forgiveness, you may see your credit score drop as a result. The lender or creditor agreeing to the debt settlement or forgiveness will likely report this activity to the major credit bureaus. Your account may be annotated as “settled” or “settled for less than the full balance.” Both of these are considered negative entries because they signal that you did not repay your debt on time and in full as agreed.

That said, the damage may already be done here. Most lenders won’t agree to forgiveness or settlement until you’ve defaulted on your debt. That means by the time you come to the negotiating table, your credit score has likely already taken a serious hit. Learn more by reading our article How Debt Settlement Affects Your Credit Score .

Debt Forgiveness May Raise Your Taxable Income

Debt forgiveness may also have some tax consequences . The amount that’s forgiven will be counted as income on your upcoming tax return, which means you may have to pay income tax on it.

Some Student Loan Forgiveness Programs Don’t Have These Negative Consequences

There’s one important caveat here. Student loan debt forgiveness programs like the popular Public Service Loan Forgiveness (PSLF) program, Teacher Loan Forgiveness , and Total and Permanent Disability Discharge do not come with these negative consequences. Participating in any of these forgiveness or cancellation programs will not negatively impact your credit score, and you won’t be responsible for paying taxes on student loan debt forgiven through the program.

However, if you participate in a 20–25-year i ncome-driven repayment program , any amount forgiven at the end of the payment period will be considered taxable income and may come with a sizable tax bill.

What Are the Different Types of Debt Forgiveness?

There are as many debt forgiveness options as there are types of debt! You may be able to find debt forgiveness programs or options for credit card debt, student loan debt, medical debt, tax debt, and more.

You may qualify for special debt forgiveness programs if you:

Are a low-income individual

Are on permanent disability

Have been affected by the coronavirus pandemic

Are a full-time student

Work in a qualifying occupation

Here’s more information about common types of debt forgiveness.

Student Loan Debt Forgiveness Options

Student loan forgiveness is a hot topic these days. Most people are familiar with the pandemic-related student loan repayment pause and the Biden administration’s proposed forgiveness plan. With the payment pause sunsetting by October 2023 and Biden’s forgiveness plan still under review by the Supreme Court, you may be wondering if student loan borrowers are left with any forgiveness options.

The good news is that several student debt relief options ]have continued outside the political chaos of Biden’s student loan forgiveness proposal.

The most popular and widely used program is the Public Service Loan Forgiveness (PSLF) program. To be eligible, you must work for a qualifying nonprofit or government organization.

Student loan borrowers who participate in income-driven repayment plans are also eligible to have their remaining loan balances forgiven after the 20–25-year repayment period. Income-based repayment is also a great way to get a more manageable student loan payment since it’s based on your discretionary income and household size (instead of the length of the loan).

How Does Student Loan Forgiveness Work?

Student loan forgiveness works like ordinary debt forgiveness (sometimes called debt cancellation when referring to student loans), but it’s specific to federal student loans issued by the U.S. Department of Education. It doesn’t apply to student loans issued by private lenders like banks.

Credit Card Debt Forgiveness Options

Credit card issuers and lenders are not as willing to negotiate debt forgiveness as you might hope because they have several debt collection tools. That said, credit card debt forgiveness is not impossible — especially if your debt has already been deemed uncollectible and you decide to pursue the path of debt settlement

For example, you might offer to pay 50% of the outstanding debt you owe in one lump sum. If your lender accepts this offer, the remaining 50% of your debt will be forgiven. Again, beware that this may lower your credit score and have tax consequences.

If you want to learn more, check out our article on 5 Solid Steps for Negotiating With Debt Collectors .

Don’t Qualify for Debt Forgiveness? Consider Filing for Bankruptcy

If you feel like you’ve tried everything and just can’t get ahead, you may want to look into filing for bankruptcy .

In Chapter 7 bankruptcy , most of your debts are erased , and you get a fresh start. You can even have federal Direct Loans discharged in bankruptcy if you meet eligibility requirements . Upsolve offers many resources for bankruptcy including a free online filing tool and access to a free consultation with a private attorney .

Let’s Summarize...

Debt forgiveness can be a great tool in the right circumstances. For credit card debt, lenders may require you to pay part of the debt, then forgive the rest. Debt forgiveness can relieve financial stress, but keep in mind your credit score may suffer and your tax bill may increase.

Thankfully, student loan forgiveness programs (except for forgiveness following the completion of an income-based repayment plan) don’t come with these same negative consequences. To help with the federal student loan debt crisis, the U.S. Department of Education offers several loan forgiveness programs that only apply to federal education loans.

Attorney Tina Tran

Tina Tran is the managing bankruptcy attorney for Upsolve, the largest consumer bankruptcy non-profit in the United States. She received her Juris Doctorate degree and Certificate in Advocacy from Loyola University Chicago School of Law. She is licensed to practice law in Illinoi... read more about Attorney Tina Tran

Continue reading and learning!

It's easy to get debt help

Choose one of the options below to get assistance with your debt:

We can help you ask to get your student loans erased

If you qualify, Upsolve can help you file bankruptcy and ask to get rid of your student loan debt.

Private Attorney

Get a free evaluation from an independent law firm.

Learning Center

Research and understand your options with our articles and guides.

Already an Upsolve user?

Bankruptcy Basics ➜

- What Is Bankruptcy?

- Every Type of Bankruptcy Explained

- How To File Bankruptcy for Free: A 10-Step Guide

- Can I File for Bankruptcy Online?

Chapter 7 Bankruptcy ➜

- What Are the Pros and Cons of Filing Chapter 7 Bankruptcy?

- What Is Chapter 7 Bankruptcy & When Should I File?

- Chapter 7 Means Test Calculator

Wage Garnishment ➜

- How To Stop Wage Garnishment Immediately

Property & Exemptions ➜

- What Are Bankruptcy Exemptions?

- Chapter 7 Bankruptcy: What Can You Keep?

- Yes! You Can Get a Mortgage After Bankruptcy

- How Long After Filing Bankruptcy Can I Buy a House?

- Can I Keep My Car If I File Chapter 7 Bankruptcy?

- Can I Buy a Car After Bankruptcy?

- Should I File for Bankruptcy for Credit Card Debt?

- How Much Debt Do I Need To File for Chapter 7 Bankruptcy?

- Can I Get Rid of my Medical Bills in Bankruptcy?

Student Loans ➜

- Can You File Bankruptcy on Student Loans?

- Can I Discharge Private Student Loans in Bankruptcy?

- Navigating Financial Aid During and After Bankruptcy: A Step-by-Step Guide

- Filing Bankruptcy to Deal With Your Student Loan Debt? Here Are 3 Things You Should Know!

Debt Collectors and Consumer Rights ➜

- 3 Steps To Take if a Debt Collector Sues You

- How To Deal With Debt Collectors (When You Can’t Pay)

Taxes and Bankruptcy ➜

- What Happens to My IRS Tax Debt if I File Bankruptcy?

- What Happens to Your Tax Refund in Bankruptcy

Chapter 13 Bankruptcy ➜

- Chapter 7 vs. Chapter 13 Bankruptcy: What’s the Difference?

- Why is Chapter 13 Probably A Bad Idea?

- How To File Chapter 13 Bankruptcy: A Step-by-Step Guide

- What Happens When a Chapter 13 Case Is Dismissed?

Going to Court ➜

- Do You Have to Go To Court to File Bankruptcy?

- Telephonic Hearings in Bankruptcy Court

Divorce and Bankruptcy ➜

- How to File Bankruptcy After a Divorce

- Chapter 13 and Divorce

Chapter 11 Bankruptcy ➜

- Chapter 7 vs. Chapter 11 Bankruptcy

- Reorganizing Your Debt? Chapter 11 or Chapter 13 Bankruptcy Can Help!

State Guides ➜

- Connecticut

- District Of Columbia

- Massachusetts

- Mississippi

- New Hampshire

- North Carolina

- North Dakota

- Pennsylvania

- Rhode Island

- South Carolina

- South Dakota

- West Virginia

Upsolve is a 501(c)(3) nonprofit that started in 2016. Our mission is to help low-income families resolve their debt and fix their credit using free software tools. Our team includes debt experts and engineers who care deeply about making the financial system accessible to everyone. We have world-class funders that include the U.S. government, former Google CEO Eric Schmidt, and leading foundations.

To learn more, read why we started Upsolve in 2016, our reviews from past users, and our press coverage from places like the New York Times and Wall Street Journal.

Watch CBS News

We may receive commissions from some links to products on this page. Promotions are subject to availability and retailer terms.

Credit card debt forgiveness: 3 things to know before signing up

By Joshua Rodriguez

Edited By Angelica Leicht

March 8, 2024 / 11:07 AM EST / CBS News

Credit card debt can be an overwhelming challenge for a lot of people — especially right now. Persistent inflation has caused the Federal Reserve to hike interest rates several times over the last couple of years, and, in turn, credit card rates — which are variable — have also increased. Those higher rates have caused rising credit card balances — now totaling 1.13 trillion nationwide — making it difficult for those with high balances to pay off what they owe.

If you're currently overwhelmed by your credit card debt, you may be considering credit card debt forgiveness programs . While these programs can offer an effective way to get out of credit card debt , it's important to educate yourself on the topic before signing up.

Find out how much relief credit card debt forgiveness may be able to provide today .

Here are a few things you should know before you enroll in a credit card debt forgiveness program:

Credit card debt forgiveness typically takes 24 to 48 months

Debt forgiveness typically happens as part of a debt relief service known as credit card debt settlement. With this process, you typically stop making credit card payments and start sending payments to your debt relief provider instead.

These payments are held in a special-purpose savings account, and once you have enough money saved to settle your debts, the debt relief company starts negotiating settlements with your creditors. If your creditors approve the settlements, they'll accept a lesser amount than what you owe to pay off your credit card debt — forgiving the remainder of your balance.

Depending on the provider, this process generally takes anywhere from 24 to 48 months . However, it can take more or less time depending on the debt forgiveness provider you choose and your unique circumstances.

Learn more and enroll in credit card debt forgiveness now .

Credit card companies don't usually forgive 100% of your debt

In most cases, the only way that credit card companies will forgive 100% of your debt is if you file for bankruptcy . With credit card debt forgiveness, the debt relief provider negotiates settlements after months of nonpayment.

In turn, they may be willing to forgive a portion of your balance to receive at least some payment on what you owe. However, they'll probably want a reasonable settlement amount in return.

There are some potential drawbacks to credit card debt forgiveness

There are a few potential disadvantages to consider before you seek debt forgiveness, including:

- The credit score impact : Stopping your credit card payments is an important part of the credit card debt forgiveness process, but it can damage your credit score. And, once you've settled, your creditors will likely report the debt to credit reporting agencies as "settled" rather than "paid as agreed," potentially causing further harm to your credit score .

- The potential tax implications : If a portion of your credit card debt is forgiven, it's considered income by the IRS. So, you may have to pay income taxes on the forgiven amount.

- There are no guarantees : Credit card companies aren't required to accept settlement offers — so not all negotiations will be successful. However, if your creditors don't agree to settle, the debt relief company will return the money you saved through the program for your settlements.

The bottom line

Credit card debt forgiveness can be a smart way to pay off debt you can't afford, but keep in mind that creditors don't typically forgive 100% of your debt and it can take a while to complete a debt forgiveness program. There are also credit and tax implications to consider. However, if you're facing debt that you can't pay off, credit card debt forgiveness could be an effective way to ease the financial hardship.

Joshua Rodriguez is a personal finance and investing writer with a passion for his craft. When he's not working, he enjoys time with his wife, two kids, two dogs and two ducks.

More from CBS News

Here's how much credit card debt the average American has (and how to pay it off)

3 things to do if interest rate cuts are delayed, according to experts

Why you should split your funds between a CD and high-yield savings account now

18 savings accounts to open for May (up to 5.55% APY)

We'll Be Right Back!

Who’s eligible for debt relief under the new plan?

What are the challenges to implementing this new debt relief plan, which loans are eligible for forgiveness , how will forgiving interest help borrowers, what steps should student loan borrowers take in the meantime, where can i apply for the new forgiveness plan , if i’m not eligible for this plan, what other options do i have, will biden’s new student loan forgiveness plan cancel my debt.

Maybe. The new rules are complicated, so we talked to an expert to answer your top questions.

Dashia Milden

Dashia is a staff editor for CNET Money who covers all angles of personal finance, including credit cards and banking. From reviews to news coverage, she aims to help readers make more informed decisions about their money. Dashia was previously a staff writer at NextAdvisor, where she covered credit cards, taxes, banking B2B payments. She has also written about safety, home automation, technology and fintech.

Courtney Johnston

Senior Editor

Courtney Johnston is a senior editor leading the CNET Money team. Passionate about financial literacy and inclusion, she has a decade of experience as a freelance journalist covering policy, financial news, real estate and investing. A New Jersey native, she graduated with an M.A. in English Literature and Professional Writing from the University of Indianapolis, where she also worked as a graduate writing instructor.

CNET staff -- not advertisers, partners or business interests -- determine how we review the products and services we cover. If you buy through our links, we may get paid.

Key takeaways:

- On April 16, the Department of Education published a first draft of the White House’s newest student debt relief plan rules.

- The administration’s latest student loan forgiveness plan could wipe out balances for 25 million borrowers.

- If passed, millions could see their debt automatically cancelled as soon as this fall. It’s unclear yet if others will need to apply for the program.

Last week, the White House announced a new student debt relief plan that would clear outstanding balances for 25 million people if enacted. And yesterday, the Department of Education just released the first draft of the proposal rules, offering clarity on who might be eligible for debt cancellation.

The Biden administration has made several attempts to pass broad federal student loan forgiveness proposals over the past few years. And it’s been a challenging road.

After the White House’s first attempt at widespread loan relief was shot down in the Supreme Court last year, the administration implemented a new income-driven repayment plan, Saving on a Valuable Education or SAVE, that offers a chance at loan forgiveness after repaying your loans for 20 to 25 years. This plan has forgiven a total of $153 billion in student debt relief for nearly 4.3 million Americans to date, including another $7.4 billion in student loans canceled in April.

Its latest endeavor to help lower the student debt burden would erase balances for some borrowers and could decrease runaway interest charges for those who don’t qualify for full relief.

“The new student loan proposals will provide full or partial financial relief to tens of millions of borrowers, especially borrowers who are experiencing financial distress,” said Mark Kantrowitz, a student financial aid expert and member of our CNET Money Expert Review Board .

As someone still repaying student loans nearly ten years later, I wanted to find out the likelihood of this new plan being passed, who will qualify for forgiveness, and what steps (if any) borrowers should take now. I shared my burning questions with Kantrowitz, and here’s what I learned.

If passed, the administration’s latest debt relief plan could wipe out balances for millions of student loan borrowers. Here’s who it could benefit:

- Borrowers with loan balances that have grown significantly due to interest could see up to $20,000 of their interest balances canceled. Those enrolled in an income-driven repayment plan making below $120,000 a year ($240,000 for those married, filing jointly) could receive automatic forgiveness for the full amount their balance has increased due to interest.

- Borrowers with undergraduate federal student loans who began repaying 20 years ago could have their remaining debt forgiven.

- Borrowers with graduate federal student loans who began repaying 25 years ago could have their remaining debt forgiven.

- Borrowers with federal student loans who are eligible for loan forgiveness under SAVE or other programs like Public Service Loan Forgiveness or Teacher Loan Forgiveness could see their balances canceled, even if they haven’t enrolled in the qualifying programs.

- Borrowers who experienced financial hardship or those who attended a school that lost federal funding might also be able to receive relief. The administration is drafting a rule for borrowers facing financial hardship in the coming months.

Since the Biden administration’s first attempt at sweeping loan forgiveness was blocked, I know it’s likely that the latest plan will also face resistance.

“The new regulations for targeted forgiveness will become final this summer,” said Kantrowitz. But he expects them to be blocked -- maybe temporarily -- by the courts.

“The main risk with President Biden’s new proposal is that it is likely to be subject to legal challenges for the same reasons as the original proposal for broad student loan forgiveness,” said Kantrowitz. The administration’s first attempt at widespread student debt relief was not authorized under the Higher Education Relief Opportunities for Students, or the HEROES Act .

And it could face other obstacles. “It may also be subject to challenges under the Administrative Procedures Act based on claims that it is arbitrary, capricious and vague and an abuse of discretion,” said Kantrowitz.

Even though some individual proposals have passed legal challenges, combining all of these proposals into a new plan could increase the chances that the courts will all block it, he added.

It’s too soon to tell what will happen, but expect a bumpy ride. The administration released its first draft of the rules today. The Department of Education will open a 30-day comment period tomorrow (April 17) to help finalize rules in time for relief in the fall. If the measure moves forward, the Biden administration expects more loan balances could be forgiven this fall.

Most federal student loans, including qualifying undergraduate, graduate, student and parent loans, will be eligible for forgiveness under the new plan, said Kantrowitz.

Some loans don’t qualify, like Federal Family Education Loans or FFEL. If you have one of these loans, you can consolidate them into a Direct loan to qualify for debt relief under an income-driven repayment plan or PSLF. You can do this by visiting Studentaid.gov and completing the steps for consolidation .

Private student loans from banks and online lenders are not eligible for debt relief.

Many student loan borrowers have larger balances now than when they initially started repayment due to runaway interest. If this is the case for you, the new interest forgiveness plan could reduce your loan balance or eliminate it altogether.

According to the White House fact sheet , the plan could help create more financial stability for working families while addressing the debt that people of color face.

The plans could eliminate accrued interest for 23 million borrowers and cancel debt for four million. Additionally, over 10 million borrowers will see relief of $5,000 or more. Black and Latino borrowers, who are more likely to see their student loan balances grow due to interest accumulation, will benefit most from the administration’s new propositions.

Whether this new student loan debt relief plan will be passed is unclear. Until then, Kantrowitz recommends signing up for autopay to ensure you don’t miss any payments. You may also qualify for a 0.25% interest rate reduction when you sign up for autopay.

Claim the student loan interest deduction on your federal income tax return. The deduction excludes up to $2,500 in interest paid on federal and private student loans and saves you money on taxes.

If you qualify for interest relief under the new plan, Kantrowitz said you can try to increase the amount of interest that will be forgiven by switching to an income-driven repayment plan. If you can’t afford payments, you can consider applying for deferment or forbearance if you meet the requirements.

Just make sure you understand how each of these steps could impact your existing loan balance. If you’re approved to make lower monthly payments or temporarily stop paying, your balance may increase due to interest. If the administration’s new debt relief isn’t successful, that could leave you with more to pay off.

If you can afford your current monthly payments but want to apply for an IDR to lower your payment and increase the interest that could be forgiven, it may make sense to contribute the difference to a high-yield savings account .

For example, if you pay $350 per month toward your student loans and an IDR lowers your payment to $150, you could contribute the extra $200 to your savings. Then, if the plan is passed, you could be eligible for more interest forgiven. If not, you can move the funds from your savings to your student loan balance. Either way, you’ve also earned interest on your money in the meantime.

There isn’t an application for the Biden administration’s new debt relief program yet. And it’s currently unclear if you’ll need to apply or if adjustments to your loan balances will be automatic.

“The goal of the new regulations is to make forgiveness automatic so that no application is necessary,” said Kantrowitz. “However, some of the proposals do not seem to be amenable to automatic forgiveness and may require an application.”

If you’re not eligible for full forgiveness or don’t qualify for aid under this latest student loan relief plan, you still have options. “Borrowers who are ineligible may be able to get some financial relief through the SAVE repayment plan, deferments and forbearances,” said Kantrowitz.

Income-driven repayment plans, like SAVE, can help you lower your monthly student loan payment to a more affordable amount. If you still need to check to see if you’re eligible to save money with the SAVE program, you can explore different IDRs at StudentAid.gov .

If you can’t afford your monthly payment, whether you’re on an IDR or not, you can talk to your servicer about deferring your student loans. If you’re experiencing financial hardship, enrolling in school or enlisting in the military, deferring your loans allows you to stop paying your student loans. During deferment, interest will not continue accruing on qualifying loans like subsidized and Perkins loans.

If you don’t qualify for deferment, you may qualify for forbearance, which allows you to stop making payments temporarily. However, interest will accrue while you’re not making payments, so your loan balance will grow. When your forbearance ends, you’ll resume making payments.

Recommended Articles

Another 277,000 borrowers received student loan forgiveness last week. here’s how you can, too, 25 million americans could have student loan debt wiped out under biden’s latest plan, fafsa rollout delayed, leaving students in limbo. what to know about this year’s financial aid deadlines.

CNET editors independently choose every product and service we cover. Though we can’t review every available financial company or offer, we strive to make comprehensive, rigorous comparisons in order to highlight the best of them. For many of these products and services, we earn a commission. The compensation we receive may impact how products and links appear on our site.

Writers and editors and produce editorial content with the objective to provide accurate and unbiased information. A separate team is responsible for placing paid links and advertisements, creating a firewall between our affiliate partners and our editorial team. Our editorial team does not receive direct compensation from advertisers.

CNET Money is an advertising-supported publisher and comparison service. We’re compensated in exchange for placement of sponsored products and services, or when you click on certain links posted on our site. Therefore, this compensation may impact where and in what order affiliate links appear within advertising units. While we strive to provide a wide range of products and services, CNET Money does not include information about every financial or credit product or service.

How does debt forgiveness work and are you eligible?

Debt forgiveness offers relief, but it won’t fix all of your financial problems..

Justin Cupler

Contributing Writer at Tally

April 17, 2020

Debt can add up quickly, making it easy to get in over your head. And some debts can nail you unexpectedly, like a tax bill. While there are many options for repaying your debt, there are some cases where paying it in full will put you in a financial bind. In these situations, debt forgiveness may help.