Essay on Internet Banking

In this essay we will discuss about Internet Banking. After reading this essay you will learn about: 1. Meaning of Internet Banking 2. Objectives and Drivers of Internet Banking 3. Trends in India 4. Facilities Available 5. Emerging Challenges 6. Main Concerns 7. Strategies to be Adopted by Indian Banks.

- Essay on the Strategies to be Adopted by Indian Banks for Introducing Internet Banking

Essay # 1. Meaning of Internet Banking :

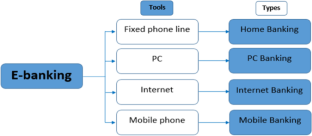

With the growth of internet and wireless communication technologies, telecommunications etc. in recent years, the structure and nature of banking and financial services have gone for a sea change. Internet banking or e-banking is the latest in this series of technological wonders in the recent past which involves use of internet for delivery of banking products and services.

Even the Morgan Stanley Dean Witter Internet Research emphasised that web is more important for retail financial services than that for many other industries. Internet banking or e-banking is changing the banking and its structure and is having major effects on banking relationships.

ADVERTISEMENTS:

Banking activity is now no longer confined to the branches where a customer has to approach the branch in person, for withdrawing cash or deposit a cheque or request for a statement of Accounts.

In accessing a true internet banking, any inquiry or transaction is processed online without any reference to the branch (anywhere banking) at any time. Thus providing Internet banking is gradually becoming a “need to have” than a “nice to have” service.

The net banking is, therefore, more of a norm rather than an exception in many developed countries because it is the cheapest way of providing banking services. Under this system, online banking is possible where every bank customer is provided with a personal identification number (PIN) for making online transactions with the bank through internet connections.

Internet banking or e-banking falls into four main categories, from Level 1—minimum functionality sites that offer only access to deposit account data—to level 4 sites highly sophisticated offering, enabling integrated sales of additional products and access to other financial services—such as investment and insurance.

In other works, a successful internet banking solution offers:

1. Exceptional rates on savings, CDs and IRAs.

2. Checking Account with no monthly fee, free bill payment and rebates on ATM surcharges.

3. Credit card facilities with low rates.

4. Easy online applications for all accounts including personal loans and mortgages.

5. 24-hour account access.

6. Quality customary service with personal attention.

Essay # 2. Objectives and Drivers of Internet Banking :

The internet has developed level playing field and thereby afforded open access to customers in the global market-place. Internet banking is a cost-effective delivery channel for the modernized financial institutions.

In this system, consumers are embracing many benefits of e-banking. To have access to one’s accounts at any time and from any location through world wide web (www) is a convenient practice, which was unknown a short time ago.

Thus, a bank’s internet presence transforms from ‘brochure/ware’ status to ‘internet banking’ status once the bank goes through a technology integration effort so as to enable its customer to access information about his or her specific account details.

Following are the six primary objectives or drivers of internet banking:

1. To improve customer access.

2. To facilitate the offering of more services.

3. To increase customer loyalty.

4. To attract large number of customers.

5. To provide cost-effective services offered by competitors.

6. To reduce customer attrition.

Keeping objectives in mind, the internet banking facilities has been progressing at a rapid pace throughout the world.

Essay # 3. Trends of Internet Banking in India :

In India, initially a beginning was made in internet banking only in some big cities which was just in rudimentary stage. After getting initial success, the internet banking facility is gradually being expanded in all cities and towns to make the system popular.

The banking industry in India is also facing unprecedented competition from non-traditional banking institutions which are now a day’s offering banking and financial services over the Internet. The deregulation of the banking industry along with emergence of new technologies are enabling the new competitors in the banking sector to enter the financial services market quite efficiently and quickly.

Core or Anywhere Banking:

In order to support internet banking facilities another new concept of banking i.e., core or anywhere banking is introduced. Initially introduced by the foreign banks, the same concept in new increasingly adopted by public sector banks and also the private sector banks.

Under this concept of banking, bank customers who have an account with any select branch can easily operate his account from different designated branches on the bank spread throughout the country.

Under this system, a customer can avail cash withdrawal, cash deposit, transfer of funds, inter-city and intra-city transactions, collection of draft and cheques etc. facilities from any of such designated branches conveniently irrespective of its locations.

Core banking concept has improved the standard of the banking services with the help of modern technology. In present times, most of the public sector banks have already adopted this concept and started extending these facilities to its customers gradually by including more and more of its important branches under this category.

Progress of Internet Banking:

In India, internet banking is gradually being developed throughout the country.

As per the recent study it is observed that:

(a) A number of banks have already adopted internet banking and are offering varied kind of services through it,

(b) These internet sites generally offer only most of the basic services. Only 50 per cent are known as ‘entry level’ sites offering little more than company information’s and basic marketing materials and 10 per cent are offering ‘advanced transactions’ such as online funds transfer, transactions and cash management services etc.; and

(c) Most of the foreign and private banks in India are much advanced in terms of the number of sites and their level of development in terms of rendering advanced technology linked services to its customers. Recently, an authority of ICICI Bank observed, “Our Internet banking base has been growing at an exponential pace over the last few years. Currently around 78 per cent of the bank’s customer base is registered for Internet banking.”

Security Precautions :

In order to make their bank account safe, one should follow certain security precautions. Customer should never share personal information like PIN number, passwords etc. with anyone, including employees of the bank. It is important that documents that contain confidential information are safeguarded. PIN or password should be changed immediately and memorized before destroying the mailers.

Customers are also advised not to provide sensitive account-related information over unsecured e-mails or over the phone. He must take simple precautions like changing the ATM, PIN and online login and transaction passwords on a regular basis. It is also important to ensure that the logged in session is properly signed out.

Essay # 4. Facilities Available Under Internet Banking in India:

Following facilities are made available for customers under internet banking in India:

(i) Bill Payment Service:

Bill payment service is a utility service of internet banking. Accordingly, each bank has tie-ups with various utility companies, service providers, insurance companies across the country. Such tie-ups can facilitate online payment of bills of electricity, telephone, mobile phone, credit card, insurance premium bills etc.

In order to make online payment of bills, a simple one-time registration for each bills has to be made and a standing instruction has to be made to make online payment of recurring bills automatically. Most interestingly, the bank usually does not charge customers for such online bill payment.

(ii) Fund Transfer:

Internet banking has made provision for transfer of any amount of fund from one account to another of the same or any other bank. Accordingly, customers can send money anywhere in India. Once a customer logs in his account, he needs to mention the payee’s account number, his bank and the branch. The transfer will take place in a day or so, whereas in a traditional method it takes about three to four working days. ICICI Bank recently reported that its online bill payment and fund transfer facility have been most popular online services.

(iii) Credit Card Customers:

Internet banking provides the facility of credit card to its customers. With internet banking, customers can not only pay their credit card bills online but also gets a loan on their cards. Not just this, they can also apply for an additional card, request a credit line increase and in case the card is lost, one can report lost card online.

(iv) Railway Pass and Online Booking:

Through Internet banking facility to issue Railway pass is also available. Indian Railways has tied up with ICICI bank for this purpose and one can now make railway pass for local trains online. The pass can be delivered to the customer at his doorstep. Initially, the facility was limited to Mumbai, Thane, Nashik, Surat and Pune. The bank would just charge Rs 10 + 12.24 per cent of service tax. Moreover, online booking of e-tickets of Railways, Airlines etc. can also be made with some arrangement with banks through Internet banking.

(v) Investing through Internet Banking:

Through Internet banking, opening a fixed deposit account has become easier. A customer can now open an FD account online through funds transfer. Online banking can also be a great friend for lazy investors. Moreover, investors with interlinked de-mat account and bank account can easily trade in the stock market and the amount will be automatically debited from their respective bank accounts and the shares will be credited in their de-mat account.

Besides, some banks provide its customers the facility to purchase mutual funds directly from the online banking system. Nowadays, most leading banks offer both online banking and de-mat account facilities. However, if a customer is having his de-mat account with independent share brokers, then he needs to sign a special form, which will link his two accounts.

(vi) Recharging Prepaid Phone:

Through Internet banking, recharging of prepaid phone has also become possible. It is no longer needed to rush to the vendor to recharge prepaid phones as and when talk time runs out. Here the customer just tops-up his prepaid mobile cards by logging in to Internet banking. By just selecting operator’s name, entering mobile number and the amount of recharge, the prepared phone of the customer is again back in action within few minutes.

(vii) Shopping at Fingertips:

Internet banking provides facility of shopping at fingertips. Leading banks have tied-up with various shopping websites. With a range of all kind of products. One can shop online and the payment is also made conveniently through his account. One can also buy railway and air tickets through Internet banking.

Essay # 5. Emerging Challenges of Internet Banking in India :

In India, a large sophisticated and highly competitive Internet Banking Market is gradually being developed with market pressure and is subjected to the following emerging challenges:

1. Demand side pressure due to increasing access to low cost electronic services.

2. Emergence of open standards for banking functionally.

3. Growing customer awareness and need for transparency.

4. Global players in the fray.

5. Close integration of bank services with web based E-commerce or even disintermediation of service through direct electronic payments (E-cash).

6. More convenient international transactions due to the fact that the Internet along the general deregulation trends, eliminate geographic boundaries.

7. Move from one stop shopping to ‘Banking Portfolio’, i.e., unbundled product purchases.

The Internet and its underlying technologies have been changing and transforming not just banking but all aspects of finance and commerce. It usually represents much more than a new distribution opportunity. Internet banking will also enable nimble players to leverage their traditional brick and mortar presence for improving customer satisfaction and gain share.

Essay # 6. Main Concerns in Internet Banking :

Internet banking in India has its areas of concern. In the mean time, a number of cases related to fraud and cheating of banks and customers by unscrupulous persons have already been lodged in India with this type of banking facilities. Irrespective of that attempts have been made by the RBI and the banking authorities for promoting safety and soundness of online and e-banking facilities in the country by issuing necessary guidelines.

In a recent survey conducted by the Online Banking Association, member institutions rated security as the most important issue of online banking. Thus there is a dual requirement to protect customers privacy and product against fraud.

Banking Securely:

Online Banking provides an overview of Internet Commerce and how one company can handle secure banking practices for its financial institution clients and their customers. Moreover, some basic information on the transmission of confidential data is presented in Security and Encryption on the web. In this respect, PC Magazine Online also offers a primer as to how encryption works.

Besides, a multi-layered security architecture comprising firewalls, filtering routers, encryption and digital certification ensures that customers account information is protected fully from un-authorised access in the following manner:

(i) Firewalls and filtering routers ensure that only the legitimate Internet users are usually allowed to access the system.

(ii) Encryption techniques used by the bank (including the sophisticated public key encryption) would ensure that privacy of data flowing between the browser and the Infinity system is protected.

(iii) Digital certification procedures provide the assurance that the data a customer receive is from the infinity system.

Essay # 7. Strategies to be Adopted by Indian Banks for Introducing Internet Banking :

In present times, Internet banking has no alternatives. Indian banking is gradually getting more and more access of Internet banking. Thus, Internet banking would drive us into an age of creative destruction due to non-physical exchange; complete transparency is also giving rise to perfectly electronic market place and customer supremacy.

At this moment, the question may be asked “what the Indian Banks should do under the present circumstances?” Whatever is the strategy chosen and options adopted, certain key parameters would largely determine the success of banks on web.

In order to attain long term success, in respect of Internet banking, a bank may follow:

(i) Adopting a webs mindset.

(ii) Catching on the first mover’s advantage.

(iii) Recognising the core competencies.

(iv) Enabling handling multiplicity with simplicity.

(v) Initiating senior management to transform the organisation from inward to outward looking.

(vi) Aligning roles and value propositions with customers segments.

(vii) Redesigning optimal channel port-folio.

(viii) Acquiring new capabilities through strategic alliances.

However, the above mentioned steps can be implemented by following four steps mentioned below:

(i) In the first phase, the customer be familiarized to new environment by demo version of software on banks, website. This will enable users to give suggestions for improvements, which can be incorporated in its later versions wherever possible.

(ii) The second phase provides various services such as account information and balances, statement of account, transaction tracking, mail box, check book issue, stop payment, financial and customized information.

(iii) The third phase may include additional multi-utility services like fund transfers, DD issue, standing instructions, opening fixed deposits and intimation of loss of ATM cards.

(iv) The final phase should include advanced corporate banking services like third party payments, utility bill payments, establishment of L/Cs, Cash Management Services etc. Enhanced plan for the customers in future may include requests for demand drafts and pay orders and many more to bring in the ultimate in banking convenience.

Thus by following the above mentioned strategies, it will help banks to translate their traditional business model into a Internet banking one, falling into the following three main categories:

(i) One-stop shop.

(ii) Virtual one stop shop.

(iii) Best of Breed Supplier.

Thus by following the above steps, the Indian bankers can pave the way for the successful introduction and popularizing the new concept of Internet banking on a large scale.

Related Articles:

- Essentials of a Sound Banking System

- Top 12 Functions of the Central Bank | Banking

- Financial Inclusion in Banking in India

- Essay on Indian Postal Services

E-banking Overview: Concepts, Challenges and Solutions

- Published: 28 November 2020

- Volume 117 , pages 1059–1078, ( 2021 )

Cite this article

- Belbergui Chaimaa 1 ,

- Elkamoun Najib 1 &

- Hilal Rachid 1

4331 Accesses

23 Citations

1 Altmetric

Explore all metrics

The expansion of information technology has led to a new form of banking. Traditional banking, based on the physical presence of the customer, is only a part of banking activities. In the last few years, electronic banking has emerged, adopting a new distribution channels like Internet and mobile services. The main goal was to allow businesses to improve the quality of service delivery and reduce transaction cost, and anytime and anywhere service demand for customers. However, it increased the vulnerability to fraudulent activities like spamming, phishing and credit card frauds. Then, the main challenge that opposes electronic banking is ensuring banking security. In this context, this paper aims to provide an overview of the electronic banking service highlighting various aspects, investigating various challenges and risks, and discussing some proposed solutions.

This is a preview of subscription content, log in via an institution to check access.

Access this article

Price includes VAT (Russian Federation)

Instant access to the full article PDF.

Rent this article via DeepDyve

Institutional subscriptions

Similar content being viewed by others

New Trends in the Banking Sector and the Development of E-Banking

A Study of Digital Banking: Security Issues and Challenges

Study of Online Bank in E-Commerce Environment

Kurnia, S., Peng, F., & Liu, Y. R. (2010). Understanding the adoption of electronic banking in China. In 43rd Hawaii International Conference on System Sciences , Honolulu, Hawaii, USA, pp. 1–10.

Vrîncianu, M., & Popa, L. A. (2010). Considerations regarding the security and protection of e-banking services consumers’ interests. The Amfiteatru Economic Journal , 12 (28), 388–403.

Google Scholar

Peotta, L., Holtz, M. D., David, B. M., Deus, F. G., & Timoteo de Sousa, R. (2011). A formal classification of internet banking attacks and vulnerabilities. International Journal of Computer Science and Information Technology, 3 (1), 186–197.

Article Google Scholar

Drig, I., & Isac, C. (2014). E-banking services – Features, challenges and benefits. 10.

Chavan, J. (2013). Internet banking – Benefits and challenges in an emerging economy. International Journal of Research in Business Management, 1 (1), 19–26.

MathSciNet Google Scholar

Singhal, D., & Padhmanabhan, V. (2009). A study on customer perception towards internet banking: Identifying major contributing factors. Journal of Nepalese Business Studies, 5 (1), 101–111.

Liao, S., Shao, Y. P., Wang, H., & Chen, A. (1999). The adoption of virtual banking: An empirical study. International Journal of Information Management, 19 (1), 63–74.

Bahl, D. S. (2012). E-banking: Challenges and policy implications. International Journal of Computing & Business Research , 229–6166.

Zarei, S. (2011). Risk management of internet banking. In 10th WSEAS International conference on Artificial Intelligence, Knowledge Engineering and Data Bases , Cambridge, UK, pp. 134–139.

Hanaek, P., Malinka, K., & Schafer, J. (2008). E-banking security - comparative study. In 42nd Annual IEEE International Carnahan Conference on Security Technology , Prague, Czech Republic, pp. 326–330.

Omariba, Z. B., & Masese, N. B. (2012). Security and privacy of electronic banking. International Journal of Computer Science Issues (IJCSI), 9 (4), 432–446.

Park, K. C., Shin, J. W., & Lee, B. G. (2014). Analysis of authentication methods for smartphone banking service using ANP. KSII Transactions on Internet & Information Systems, 8 (6).

Brar, T. P. S., Sharma, D., & Khurmi, S. S. (2012). Vulnerabilities in e-banking: A study of various security aspects in e-banking. International Journal of Computing & Business Research .

Yang, Y. J. (1997). The security of electronic. In International Systems Security Conference , pp. 41–52.

Yang, J., Cheng, L., & Luo, X. (2009). A comparative study on e-banking services between China and USA. International Journal of Electronic Finance, 3 (3), 235–252.

Zahid, N., Mujtaba, A., & Riaz, A. (2010). Consumer acceptance of online banking. European Journal of Economics, Finance and Administrative Sciences, 27 (1).

Geetha, K. T., & Malarvizhi, V. (2011). Acceptance of E-banking among customers: An empirical investigation in India. The Journal of Internet Banking and Commerce, 15 (2), 1–17.

Deb, M., & Lomo-David, E. (2014). An empirical examination of customers’ adoption of m-banking in India. Marketing Intelligence & Planning, 32 (4), 475–494.

Lee, J. H., Lim, W. G., & Lim, J. I. (2013). A study of the security of Internet banking and financial private information in South Korea. Mathematical and Computer Modelling, 58 (1–2), 117–131.

Moga, L., Nor, K., Neculita, M., & Khani, N. (2012). Trust and security in e-banking adoption in Romania. Communications of the IBIMA , 1–10.

Komb, F., Korau, M., Belás, J., & Korauš, A. (2016). Electronic banking security and customer satisfaction in commercial banks. Journal of Security and Sustainability Issues, 5 (3), 411–422.

Ranaweera, H. (2019). Risk of electronic payments of the banking sector in Sri Lanka: Case of Colombo district. 4 (1).

Rajaratnam, A. (2019). The factors influencing on internet banking adoption in Trincomalee District, Sri Lanka, Sri Lanka. International Research Journal of Advanced Engineering and Science, 4 (1), 160–164.

Hasan, A. S., Baten, M. A., Kamil, A. A., & Parveen, S. (2010). Adoption of e-banking in Bangladesh: An exploratory study. African Journal of Business Management, 4 (13), 2718–2727.

Jalal, A., Marzooq, J., & Nabi, H. A. (2011). Evaluating the impacts of online banking factors on motivating the process of e-banking. Journal of Management and Sustainability, 1 (1).

Abukhzam, M., & Lee, A. (2010). Factors affecting bank staff attitude towards E-banking adoption in Libya. The Electronic Journal of Information Systems in Developing Countries, 42 (1), 1–15.

Abdellatif, T., Jinene, C., & Khazmi, N. (2014). Une cartographie de la résistance à l’adoption du M-Banking en Tunisie [Mapping of resistance to the adoption of M-Banking in Tunisia]. 8 (1).

Halime, Z. F., & Kirmi, B. Etude de la résistance à l’adoption et l’utilisation de la banque mobile. Management Research .

Floh, A., & Treiblmaier, H. (2006). What keeps the e-banking customer loyal? A multigroup analysis of the moderating role of consumer characteristics on e-loyalty in the financial service industry. SSRN Electronic Journal .

Gunson, N., Marshall, D., Morton, H., & Jack, M. (2011). User perceptions of security and usability of single-factor and two-factor authentication in automated telephone banking. Computers & Security, 30 (4), 208–220.

Weir, C. S., Douglas, G., Richardson, T., & Jack, M. (2010). Usable security: User preferences for authentication methods in eBanking and the effects of experience. Interacting with Computers, 22 (3), 153–164.

Ahmad, D. T., & Hariri, M. (2012). User acceptance of biometrics in e-banking to improve security.

Tassabehji, R., & Kamala, M. A. (2009). Improving e-banking security with biometrics: Modelling user attitudes and acceptance. In 3rd International Conference on New Technologies, Mobility and Security , Cairo, Egypt, pp. 1–6.

Moeckel, C. Human-computer interaction for security research: The case of EU e-banking systems.

Rifà-Pous, H. (2009). A secure mobile-based authentication system for e-banking. In On the Move to Meaningful Internet Systems: OTM, 5871 , 848–860.

Hamidi, N. A., Mahdi Rahimi, G. K., Nafarieh, A., Hamidi, A., & Robertson, B. (2013). Personalized security approaches in e-banking employing flask architecture over cloud environment. Procedia Computer Science, 21 , 18–24.

Alsaiari, H., Papadaki, M., Dowland, P. S., & Furnell, S. M. (2014). Alternative graphical authentication for online banking environments.

Elkhodr, M., Shahrestani, S., & Kourouche, K. (2012). A proposal to improve the security of mobile banking applications. 2012 Tenth International Conference on ICT and Knowledge Engineering (pp. 260–265). IEEE: Bangkok, Thailand.

Chapter Google Scholar

Islam Khan, B. U., Olanrewaju, R. F., Anwar, F., & Yaacob, M. (2018). Offline OTP based solution for secure internet banking access. In 2018 IEEE Conference on e-Learning, e-Management and e-Services (IC3e) , Langkawi Island, Malaysia, pp. 167–172.

Brodi, D., & Jankovi, R. (2016). Usability analysis of the specific captcha types. In International Scientific Conference , pp. 272–277.

Hoonakker, P., Bornoe, N., & Carayon, P. (2009). Password authentication from a human factors perspective: Results of a survey among end-users. Human Factors and Ergonomics Society Annual Meeting Proceedings, 53 (6), 459–463.

Mridha, F., Nur, K., Kumar, A., & Akhtaruzzaman, M. (2017). A new approach to enhance internet banking security. International Journal of Computer Applications, 160 (8), 35–39.

Chandanshive, A., Sureka, A., Gongiwala, V., & Nalawade, A. (2018). Access control using 3 level authentications for e-banking. International Journal on Recent and Innovation Trends in Computing and Communication, 6 (4).

Shen, L., Zheng, N., Zheng, S., & Li, W. (2010). Secure mobile services by face and speech based personal authentication. In 2010 IEEE International Conference on Intelligent Computing and Intelligent Systems , Xiamen, China, pp. 97–100.

Onyesolu, M. O., Odoh, M., Akanwa, A. O., & Nwasor, V. C. (2010). Robust authentication model for ATM: A biometric strategy measure for enhancing e-banking security in Nigeria. International Journal of Advanced Research in Computer Science .

Bhosale, S. T. (2012). Security in e-banking via card less biometric. International Journal of Advanced Technology & Engineering Research, 2 (4), 457–462 2(2250).

Plateaux, A., Lacharme, P., Jøsang, A., & Rosenberger, C. (2014). One-time biometrics for online banking and electronic payment authentication. Availability, Reliability, and Security in Information Systems, 8708 , 179–193.

Darwish, S. M., & Hassan, A. M. (2012). A model to authenticate requests for online banking transactions. Alexandria Engineering Journal, 51 (3), 185–191.

Kumbhar, S., & Sahu, S. (2007). A new framework for online transaction using visual cryptography and steganography. International Journal of Innovative Research in Computer and Communication Engineering, 3 (11), 11418–11422.

Yaseen Khudhur, D., Saad Hameed, S., & Al-Barzinji, S. M. (2018). Enhancing e-banking security: Using whirlpool hash function for card number encryption. International Journal of Engineering & Technology, 7 (2.13).

Thompson, L. (2003). Smart card authentication: Added security for systems and network access.

Karia, A., Patankar, D. A. B., & Tawde, P. (2014). SMS-based one time password vulnerabilities and safeguarding OTP over network. International Journal of Engineering Research, 3 (5).

Al-Fairuz, M., & Renaud, K. (2010). Multi-channel, multi-level authentication for more secure eBanking.

Alarifi, A., Alsaleh, M., & Alomar, N. (2017). A model for evaluating the security and usability of e-banking platforms. Computing, 99 (5), 519–535.

Article MathSciNet Google Scholar

Download references

Author information

Authors and affiliations.

STIC Laboratory, Chouaib Doukkali University, El Jadida, Morocco

Belbergui Chaimaa, Elkamoun Najib & Hilal Rachid

You can also search for this author in PubMed Google Scholar

Corresponding author

Correspondence to Belbergui Chaimaa .

Additional information

Publisher’s Note Springer Nature remains neutral with regard to jurisdictional claims in published maps and institutional affiliations.

Rights and permissions

Reprints and permissions

About this article

Chaimaa, B., Najib, E. & Rachid, H. E-banking Overview: Concepts, Challenges and Solutions. Wireless Pers Commun 117 , 1059–1078 (2021). https://doi.org/10.1007/s11277-020-07911-0

Download citation

Accepted : 29 October 2020

Published : 28 November 2020

Issue Date : March 2021

DOI : https://doi.org/10.1007/s11277-020-07911-0

Share this article

Anyone you share the following link with will be able to read this content:

Sorry, a shareable link is not currently available for this article.

Provided by the Springer Nature SharedIt content-sharing initiative

- Authentication

- Find a journal

- Publish with us

- Track your research

- Open access

- Published: 18 June 2021

Financial technology and the future of banking

- Daniel Broby ORCID: orcid.org/0000-0001-5482-0766 1

Financial Innovation volume 7 , Article number: 47 ( 2021 ) Cite this article

41k Accesses

54 Citations

4 Altmetric

Metrics details

This paper presents an analytical framework that describes the business model of banks. It draws on the classical theory of banking and the literature on digital transformation. It provides an explanation for existing trends and, by extending the theory of the banking firm, it illustrates how financial intermediation will be impacted by innovative financial technology applications. It further reviews the options that established banks will have to consider in order to mitigate the threat to their profitability. Deposit taking and lending are considered in the context of the challenge made from shadow banking and the all-digital banks. The paper contributes to an understanding of the future of banking, providing a framework for scholarly empirical investigation. In the discussion, four possible strategies are proposed for market participants, (1) customer retention, (2) customer acquisition, (3) banking as a service and (4) social media payment platforms. It is concluded that, in an increasingly digital world, trust will remain at the core of banking. That said, liquidity transformation will still have an important role to play. The nature of banking and financial services, however, will change dramatically.

Introduction

The bank of the future will have several different manifestations. This paper extends theory to explain the impact of financial technology and the Internet on the nature of banking. It provides an analytical framework for academic investigation, highlighting the trends that are shaping scholarly research into these dynamics. To do this, it re-examines the nature of financial intermediation and transactions. It explains how digital banking will be structurally, as well as physically, different from the banks described in the literature to date. It does this by extending the contribution of Klein ( 1971 ), on the theory of the banking firm. It presents suggested strategies for incumbent, and challenger banks, and how banking as a service and social media payment will reshape the competitive landscape.

The banking industry has been evolving since Banca Monte dei Paschi di Siena opened its doors in 1472. Its leveraged business model has proved very scalable over time, but it is now facing new challenges. Firstly, its book to capital ratios, as documented by Berger et al ( 1995 ), have been consistently falling since 1840. This trend continues as competition has increased. In the past decade, the industry has experienced declines in profitability as measured by return on tangible equity. This is partly the result of falling leverage and fee income and partly due to the net interest margin (connected to traditional lending activity). These trends accelerated following the 2008 financial crisis. At the same time, technology has made banks more competitive. Advances in digital technology are changing the very nature of banking. Banks are now distributing services via mobile technology. A prolonged period of very low interest rates is also having an impact. To sustain their profitability, Brei et al. ( 2020 ) note that many banks have increased their emphasis on fee-generating services.

As Fama ( 1980 ) explains, a bank is an intermediary. The Internet is, however, changing the way financial service providers conduct their role. It is fundamentally changing the nature of the banking. This in turn is changing the nature of banking services, and the way those services are delivered. As a consequence, in order to compete in the changing digital landscape, banks have to adapt. The banks of the future, both incumbents and challengers, need to address liquidity transformation, data, trust, competition, and the digitalization of financial services. Against this backdrop, incumbent banks are focused on reinventing themselves. The challenger banks are, however, starting with a blank canvas. The research questions that these dynamics pose need to be investigated within the context of the theory of banking, hence the need to revise the existing analytical framework.

Banks perform payment and transfer functions for an economy. The Internet can now facilitate and even perform these functions. It is changing the way that transactions are recorded on ledgers and is facilitating both public and private digital currencies. In the past, banks operated in a world of information asymmetry between themselves and their borrowers (clients), but this is changing. This differential gave one bank an advantage over another due to its knowledge about its clients. The digital transformation that financial technology brings reduces this advantage, as this information can be digitally analyzed.

Even the nature of deposits is being transformed. Banks in the future will have to accept deposits and process transactions made in digital form, either Central Bank Digital Currencies (CBDC) or cryptocurrencies. This presents a number of issues: (1) it changes the way financial services will be delivered, (2) it requires a discussion on resilience, security and competition in payments, (3) it provides a building block for better cross border money transfers and (4) it raises the question of private and public issuance of money. Braggion et al ( 2018 ) consider whether these represent a threat to financial stability.

The academic study of banking began with Edgeworth ( 1888 ). He postulated that it is based on probability. In this respect, the nature of the business model depends on the probability that a bank will not be called upon to meet all its liabilities at the same time. This allows banks to lend more than they have in deposits. Because of the resultant mismatch between long term assets and short-term liabilities, a bank’s capital structure is very sensitive to liquidity trade-offs. This is explained by Diamond and Rajan ( 2000 ). They explain that this makes a bank a’relationship lender’. In effect, they suggest a bank is an intermediary that has borrowed from other investors.

Diamond and Rajan ( 2000 ) argue a lender can negotiate repayment obligations and that a bank benefits from its knowledge of the customer. As shall be shown, the new generation of digital challenger banks do not have the same tradeoffs or knowledge of the customer. They operate more like a broker providing a platform for banking services. This suggests that there will be more than one type of bank in the future and several different payment protocols. It also suggests that banks will have to data mine customer information to improve their understanding of a client’s financial needs.

The key focus of Diamond and Rajan ( 2000 ), however, was to position a traditional bank is an intermediary. Gurley and Shaw ( 1956 ) describe how the customer relationship means a bank can borrow funds by way of deposits (liabilities) and subsequently use them to lend or invest (assets). In facilitating this mediation, they provide a service whereby they store money and provide a mechanism to transmit money. With improvements in financial technology, however, money can be stored digitally, lenders and investors can source funds directly over the internet, and money transfer can be done digitally.

A review of financial technology and banking literature is provided by Thakor ( 2020 ). He highlights that financial service companies are now being provided by non-deposit taking contenders. This paper addresses one of the four research questions raised by his review, namely how theories of financial intermediation can be modified to accommodate banks, shadow banks, and non-intermediated solutions.

To be a bank, an entity must be authorized to accept retail deposits. A challenger bank is, therefore, still a bank in the traditional sense. It does not, however, have the costs of a branch network. A peer-to-peer lender, meanwhile, does not have a deposit base and therefore acts more like a broker. This leads to the issue that this paper addresses, namely how the banks of the future will conduct their intermediation.

In order to understand what the bank of the future will look like, it is necessary to understand the nature of the aforementioned intermediation, and the way it is changing. In this respect, there are two key types of intermediation. These are (1) quantitative asset transformation and, (2) brokerage. The latter is a common model adopted by challenger banks. Figure 1 depicts how these two types of financial intermediation match savers with borrowers. To avoid nuanced distinction between these two types of intermediation, it is common to classify banks by the services they perform. These can be grouped as either private, investment, or commercial banking. The service sub-groupings include payments, settlements, fund management, trading, treasury management, brokerage, and other agency services.

How banks act as intermediaries between lenders and borrowers. This function call also be conducted by intermediaries as brokers, for example by shadow banks. Disintermediation occurs over the internet where peer-to-peer lenders match savers to lenders

Financial technology has the ability to disintermediate the banking sector. The competitive pressures this results in will shape the banks of the future. The channels that will facilitate this are shown in Fig. 2 , namely the Internet and/or mobile devices. Challengers can participate in this by, (1) directly matching borrows with savers over the Internet and, (2) distributing white labels products. The later enables banking as a service and avoids the aforementioned liquidity mismatch.

The strategic options banks have to match lenders with borrowers. The traditional and challenger banks are in the same space, competing for business. The distributed banks use the traditional and challenger banks to white label banking services. These banks compete with payment platforms on social media. The Internet heralds an era of banking as a service

There are also physical changes that are being made in the delivery of services. Bricks and mortar branches are in decline. Mobile banking, or m-banking as Liu et al ( 2020 ) describe it, is an increasingly important distribution channel. Robotics are increasingly being used to automate customer interaction. As explained by Vishnu et al ( 2017 ), these improve efficiency and the quality of execution. They allow for increased oversight and can be built on legacy systems as well as from a blank canvas. Application programming interfaces (APIs) are bringing the same type of functionality to m-banking. They can be used to authorize third party use of banking data. How banks evolve over time is important because, according to the OECD, the activity in the financial sector represents between 20 and 30 percent of developed countries Gross Domestic Product.

In summary, financial technology has evolved to a level where online banks and banking as a service are challenging incumbents and the nature of banking mediation. Banking is rapidly transforming because of changes in such technology. At the same time, the solving of the double spending problem, whereby digital money can be cryptographically protected, has led to the possibility that paper money will become redundant at some point in the future. A theoretical framework is required to understand this evolving landscape. This is discussed next.

The theory of the banking firm: a revision

In financial theory, as eloquently explained by Fama ( 1980 ), banking provides an accounting system for transactions and a portfolio system for the storage of assets. That will not change for the banks of the future. Fama ( 1980 ) explains that their activities, in an unregulated state, fulfil the Modigliani–Miller ( 1959 ) theorem of the irrelevance of the financing decision. In practice, traditional banks compete for deposits through the interest rate they offer. This makes the transactional element dependent on the resulting debits and credits that they process, essentially making banks into bookkeeping entities fulfilling the intermediation function. Since this is done in response to competitive forces, the general equilibrium is a passive one. As such, the banking business model is vulnerable to disruption, particularly by innovation in financial technology.

A bank is an idiosyncratic corporate entity due to its ability to generate credit by leveraging its balance sheet. That balance sheet has assets on one side and liabilities on the other, like any corporate entity. The assets consist of cash, lending, financial and fixed assets. On the other side of the balance sheet are its liabilities, deposits, and debt. In this respect, a bank’s equity and its liabilities are its source of funds, and its assets are its use of funds. This is explained by Klein ( 1971 ), who notes that a bank’s equity W , borrowed funds and its deposits B is equal to its total funds F . This is the same for incumbents and challengers. This can be depicted algebraically if we let incumbents be represented by Φ and challengers represented by Γ:

Klein ( 1971 ) further explains that a bank’s equity is therefore made up of its share capital and unimpaired reserves. The latter are held by a bank to protect the bank’s deposit clients. This part is also mandated by regulation, so as to protect customers and indeed the entire banking system from systemic failure. These protective measures include other prudential requirements to hold cash reserves or other liquid assets. As shall be shown, banking services can be performed over the Internet without these protections. Banking as a service, as this phenomenon known, is expected to increase in the future. This will change the nature of the protection available to clients. It will change the way banks transform assets, explained next.

A bank’s deposits are said to be a function of the proportion of total funds obtained through the issuance of the ith deposit type and its total funds F , represented by α i . Where deposits, represented by Bs , are made in the form of Bs (i = 1 *s n) , they generate a rate of interest. It follows that Si Bs = B . As such,

Therefor it can be said that,

The importance of Eq. 3 is that the balance sheet can be leveraged by the issuance of loans. It should be noted, however, that not all loans are returned to the bank in whole or part. Non-performing loans reduce the asset side of a bank’s balance sheet and act as a constraint on capital, and therefore new lending. Clearly, this is not the case with banking as a service. In that model, loans are brokered. That said, with the traditional model, an advantage of financial technology is that it facilitates the data mining of clients’ accounts. Lending can therefore be more targeted to borrowers that are more likely to repay, thereby reducing non-performing loans. Pari passu, the incumbent bank of the future will therefore have a higher risk-adjusted return on capital. In practice, however, banking as a service will bring greater competition from challengers and possible further erosion of margins. Alternatively, some banks will proactively engage in partnerships and acquisitions to maintain their customer base and address the competition.

A bank must have reserves to meet the demand of customers demanding their deposits back. The amount of these reserves is a key function of banking regulation. The Basel Committee on Banking Supervision mandates a requirement to hold various tiers of capital, so that banks have sufficient reserves to protect depositors. The Committee also imposes a framework for mitigating excessive liquidity risk and maturity transformation, through a set Liquidity Coverage Ratio and Net Stable Funding Ratio.

Recent revisions of theory, because of financial technology advances, have altered our understanding of banking intermediation. This will impact the competitive landscape and therefor shape the nature of the bank of the future. In this respect, the threat to incumbent banks comes from peer-to-peer Internet lending platforms. These perform the brokerage function of financial intermediation without the use of the aforementioned banking balance sheet. Unlike regulated deposit takers, such lending platforms do not create assets and do not perform risk and asset transformation. That said, they are reliant on investors who do not always behave in a counter cyclical way.

Financial technology in banking is not new. It has been used to facilitate electronic markets since the 1980’s. Thakor ( 2020 ) refers to three waves of application of financial innovation in banking. The advent of institutional futures markets and the changing nature of financial contracts fundamentally changed the role of banks. In response to this, academics extended the concept of a bank into an entity that either fulfills the aforementioned functions of a broker or a qualitative asset transformer. In this respect, they connect the providers and users of capital without changing the nature of the transformation of the various claims to that capital. This transformation can be in the form risk transfer or the application of leverage. The nature of trading of financial assets, however, is changing. Price discovery can now be done over the Internet and that is moving liquidity from central marketplaces (like the stock exchange) to decentralized ones.

Alongside these trends, in considering what the bank of the future will look like, it is necessary to understand the unregulated lending market that competes with traditional banks. In this part of the lending market, there has been a rise in shadow banks. The literature on these entities is covered by Adrian and Ashcraft ( 2016 ). Shadow banks have taken substantial market share from the traditional banks. They fulfil the brokerage function of banks, but regulators have only partial oversight of their risk transformation or leverage. The rise of shadow banks has been facilitated by financial technology and the originate to distribute model documented by Bord and Santos ( 2012 ). They use alternative trading systems that function as electronic communication networks. These facilitate dark pools of liquidity whereby buyers and sellers of bonds and securities trade off-exchange. Since the credit crisis of 2008, total broker dealer assets have diverged from banking assets. This illustrates the changed lending environment.

In the disintermediated market, banking as a service providers must rely on their equity and what access to funding they can attract from their online network. Without this they are unable to drive lending growth. To explain this, let I represent the online network. Extending Klein ( 1971 ), further let Ψ represent banking as a service and their total funds by F . This state is depicted as,

Theoretically, it can be shown that,

Shadow banks, and those disintermediators who bypass the banking system, have an advantage in a world where technology is ubiquitous. This becomes more apparent when costs are considered. Buchak et al. ( 2018 ) point out that shadow banks finance their originations almost entirely through securitization and what they term the originate to distribute business model. Diversifying risk in this way is good for individual banks, as banking risks can be transferred away from traditional banking balance sheets to institutional balance sheets. That said, the rise of securitization has introduced systemic risk into the banking sector.

Thus, we can see that the nature of banking capital is changing and at the same time technology is replacing labor. Let A denote the number of transactions per account at a period in time, and C denote the total cost per account per time period of providing the services of the payment mechanism. Klein ( 1971 ) points out that, if capital and labor are assumed to be part of the traditional banking model, it can be observed that,

It can therefore be observed that the total service charge per account at a period in time, represented by S, has a linear and proportional relationship to bank account activity. This is another variable that financial technology can impact. According to Klein ( 1971 ) this can be summed up in the following way,

where d is the basic bank decision variable, the service charge per transaction. Once again, in an automated and digital environment, financial technology greatly reduces d for the challenger banks. Swankie and Broby ( 2019 ) examine the impact of Artificial Intelligence on the evaluation of banking risk and conclude that it improves such variables.

Meanwhile, the traditional banking model can be expressed as a product of the number of accounts, M , and the average size of an account, N . This suggests a banks implicit yield is it rate of interest on deposits adjusted by its operating loss in each time period. This yield is generated by payment and loan services. Let R 1 depict this. These can be expressed as a fraction of total demand deposits. This is depicted by Klein ( 1971 ), if one assumes activity per account is constant, as,

As a result, whether a bank is structured with traditional labor overheads or built digitally, is extremely relevant to its profitability. The capital and labor of tradition banks, depicted as Φ i , is greater than online networks, depicted as I i . As such, the later have an advantage. This can be shown as,

What Klein (1972) failed to highlight is that the banking inherently involves leverage. Diamond and Dybving (1983) show that leverage makes bank susceptible to run on their liquidity. The literature divides these between adverse shock events, as explained by Bernanke et al ( 1996 ) or moral hazard events as explained by Demirgu¨¸c-Kunt and Detragiache ( 2002 ). This leverage builds on the balance sheet mismatch of short-term assets with long term liabilities. As such, capital and liquidity are intrinsically linked to viability and solvency.

The way capital and liquidity are managed is through credit and default management. This is done at a bank level and a supervisory level. The Basel Committee on Banking Supervision applies capital and leverage ratios, and central banks manage interest rates and other counter-cyclical measures. The various iterations of the prudential regulation of banks have moved the microeconomic theory of banking from the modeling of risk to the modeling of imperfect information. As mentioned, shadow and disintermediated services do not fall under this form or prudential regulation.

The relationship between leverage and insolvency risk crucially depends on the degree of banks total funds F and their liability structure L . In this respect, the liability structure of traditional banks is also greater than online networks which do not have the same level of available funds, depicted as,

Diamond and Dybvig ( 1983 ) observe that this liability structure is intimately tied to a traditional bank’s assets. In this respect, a bank’s ability to finance its lending at low cost and its ability to achieve repayment are key to its avoidance of insolvency. Online networks and/or brokers do not have to finance their lending, simply source it. Similarly, as brokers they do not face capital loss in the event of a default. This disintermediates the bank through the use of a peer-to-peer environment. These lenders and borrowers are introduced in digital way over the internet. Regulators have taken notice and the digital broker advantage might not last forever. As a result, the future may well see greater cooperation between these competing parties. This also because banks have valuable operational experience compared to new entrants.

It should also be observed that bank lending is either secured or unsecured. Interest on an unsecured loan is typically higher than the interest on a secured loan. In this respect, incumbent banks have an advantage as their closeness to the customer allows them to better understand the security of the assets. Berger et al ( 2005 ) further differentiate lending into transaction lending, relationship lending and credit scoring.

The evolution of the business model in a digital world

As has been demonstrated, the bank of the future in its various manifestations will be a consequence of the evolution of the current banking business model. There has been considerable scholarly investigation into the uniqueness of this business model, but less so on its changing nature. Song and Thakor ( 2010 ) are helpful in this respect and suggest that there are three aspects to this evolution, namely competition, complementary and co-evolution. Although liquidity transformation is evolving, it remains central to a bank’s role.

All the dynamics mentioned are relevant to the economy. There is considerable evidence, as outlined by Levine ( 2001 ), that market liberalization has a causal impact on economic growth. The impact of technology on productivity should prove positive and enhance the functioning of the domestic financial system. Indeed, market liberalization has already reshaped banking by increasing competition. New fee based ancillary financial services have become widespread, as has the proprietorial use of balance sheets. Risk has been securitized and even packaged into trade-able products.

Challenger banks are developing in a complementary way with the incumbents. The latter have an advantage over new entrants because they have information on their customers. The liquidity insurance model, proposed by Diamond and Dybvig ( 1983 ), explains how such banks have informational advantages over exchange markets. That said, financial technology changes these dynamics. It if facilitating the processing of financial data by third parties, explained in greater detail in the section on Open Banking.

At the same time, financial technology is facilitating banking as a service. This is where financial services are delivered by a broker over the Internet without resort to the balance sheet. This includes roboadvisory asset management, peer to peer lending, and crowd funding. Its growth will be facilitated by Open Banking as it becomes more geographically adopted. Figure 3 illustrates how these business models are disintermediating the traditional banking role and matching burrowers and savers.

The traditional view of banks ecosystem between savers and borrowers, atop the Internet which is matching savers and borrowers directly in a peer-to-peer way. The Klein ( 1971 ) theory of the banking firm does not incorporate the mirrored dynamics, and as such needs to be extended to reflect the digital innovation that impacts both borrowers and severs in a peer-to-peer environment

Meanwhile, the banking sector is co-evolving alongside a shadow banking phenomenon. Lenders and borrowers are interacting, but outside of the banking sector. This is a concern for central banks and banking regulators, as the lending is taking place in an unregulated environment. Shadow banking has grown because of financial technology, market liberalization and excess liquidity in the asset management ecosystem. Pozsar and Singh ( 2011 ) detail the non-bank/bank intersection of shadow banking. They point out that shadow banking results in reverse maturity transformation. Incumbent banks have blurred the distinction between their use of traditional (M2) liabilities and market-based shadow banking (non-M2) liabilities. This impacts the inter-generational transfers that enable a bank to achieve interest rate smoothing.

Securitization has transformed the risk in the banking sector, transferring it to asset management institutions. These include structured investment vehicles, securities lenders, asset backed commercial paper investors, credit focused hedge and money market funds. This in turn has led to greater systemic risk, the result of the nature of the non-traded liabilities of securitized pooling arrangements. This increased risk manifested itself in the 2008 credit crisis.

Commercial pressures are also shaping the banking industry. The drive for cost efficiency has made incumbent banks address their personally costs. Bank branches have been closed as technology has evolved. Branches make it easier to withdraw or transfer deposits and challenger banks are not as easily able to attract new deposits. The banking sector is therefore looking for new point of customer contact, such as supermarkets, post offices and social media platforms. These structural issues are occurring at the same time as the retail high street is also evolving. Banks have had an aggressive roll out of automated telling machines and a reduction in branches and headcount. Online digital transactions have now become the norm in most developed countries.

The financing of banks is also evolving. Traditional banks have tended to fund illiquid assets with short term and unstable liquid liabilities. This is one of the key contributors to the rise to the credit crisis of 2008. The provision of liquidity as a last resort is central to the asset transformation process. In this respect, the banking sector experienced a shock in 2008 in what is termed the credit crisis. The aforementioned liquidity mismatch resulted in the system not being able to absorb all the risks associated with subprime lending. Central banks had to resort to quantitative easing as a result of the failure of overnight funding mechanisms. The image of the entire banking sector was tarnished, and the banks of the future will have to address this.

The future must learn from the mistakes of the past. The structural weakness of the banking business model cannot be solved. That said, the latest Basel rules introduce further risk mitigation, improved leverage ratios and increased levels of capital reserve. Another lesson of the credit crisis was that there should be greater emphasis on risk culture, governance, and oversight. The independence and performance of the board, the experience and the skill set of senior management are now a greater focus of regulators. Internal controls and data analysis are increasingly more robust and efficient, with a greater focus on a banks stable funding ratio.

Meanwhile, the very nature of money is changing. A digital wallet for crypto-currencies fulfills much the same storage and transmission functions of a bank; and crypto-currencies are increasing being used for payment. Meanwhile, in Sweden, stores have the right to refuse cash and the majority of transactions are card based. This move to credit and debit cards, and the solving of the double spending problem, whereby digital money can be crypto-graphically protected, has led to the possibility that paper money could be replaced at some point in the future. Whether this might be by replacement by a CBDC, or decentralized digital offering, is of secondary importance to the requirement of banks to adapt. Whether accommodating crytpo-currencies or CBDC’s, Kou et al. ( 2021 ) recommend that banks keep focused on alternative payment and money transferring technologies.

Central banks also have to adapt. To limit disintermediation, they have to ensure that the economic design of their sponsored digital currencies focus on access for banks, interest payment relative to bank policy rate, banking holding limits and convertibility with bank deposits. All these developments have implications for banks, particularly in respect of funding, the secure storage of deposits and how digital currency interacts with traditional fiat money.

Open banking

Against the backdrop of all these trends and changes, a new dynamic is shaping the future of the banking sector. This is termed Open Banking, already briefly mentioned. This new way of handling banking data protocols introduces a secure way to give financial service companies consensual access to a bank’s customer financial information. Figure 4 illustrates how this works. Although a fairly simple concept, the implications are important for the banking industry. Essentially, a bank customer gives a regulated API permission to securely access his/her banking website. That is then used by a banking as a service entity to make direct payments and/or download financial data in order to provide a solution. It heralds an era of customer centric banking.

How Open Banking operates. The customer generates data by using his bank account. A third party provider is authorized to access that data through an API request. The bank confirms digitally that the customer has authorized the exchange of data and then fulfills the request

Open Banking was a response to the documented inertia around individual’s willingness to change bank accounts. Following the Retail Banking Review in the UK, this was addressed by lawmakers through the European Union’s Payment Services Directive II. The legislation was designed to make it easier to change banks by allowing customers to delegate authority to transfer their financial data to other parties. As a result of this, a whole host of data centric applications were conceived. Open banking adds further momentum to reshaping the future of banking.

Open Banking has a number of quite revolutionary implications. It was started so customers could change banks easily, but it resulted in some secondary considerations which are going to change the future of banking itself. It gives a clear view of bank financing. It allows aggregation of finances in one place. It also allows can give access to attractive offerings by allowing price comparisons. Open Banking API’s build a secure online financial marketplace based on data. They also allow access to a larger market in a faster way but the third-party providers for the new entrants. Open Banking allows developers to build single solutions on an API addressing very specific problems, like for example, a cash flow based credit rating.

Romānova et al. ( 2018 ) undertook a questionnaire on the Payment Services Directive II. The results suggest that Open Banking will promote competitiveness, innovation, and new product development. The initiative is associated with low costs and customer satisfaction, but that some concerns about security, privacy and risk are present. These can be mitigated, to some extent, by secure protocols and layered permission access.

Discussion: strategic options

Faced with these disruptive trends, there are four strategic options for market participants to con- sider. There are (1) a defensive customer retention strategy for incumbents, (2) an aggressive customer acquisition strategy for challenger banks (3) a banking as a service strategy for new entrants, and (4) a payments strategy for social media platforms.

Each of these strategies has to be conducted in a competitive marketplace for money demand by potential customers. Figure 5 illustrates where the first three strategies lie on the tradeoff between money demand and interest rates. The payment strategy can’t be modeled based on the supply of money. In the figure, the market settles at a rate L 2 . The incumbent banks have the capacity to meet the largest supply of these loans. The challenger banks have a constrained function but due to a lower cost base can gain excess rent through higher rates of interest. The peer-to-peer bank as a service brokers must settle for the market rate and a constrained supply offering.

The money demand M by lenders on the y axis. Interest rates on the y axis are labeled as r I and r II . The challenger banks are represented by the line labeled Γ. They have a price and technology advantage and so can lend at higher interest rates. The brokers are represented by the line labeled Ω. They are price takers, accepting the interest rate determined by the market. The same is true for the incumbents, represented by the line labeled Φ but they have a greater market share due to their customer relationships. Note that payments strategy for social media platforms is not shown on this figure as it is not affected by interest rates

Figure 5 illustrates that having a niche strategy is not counterproductive. Liu et al ( 2020 ) found that banks performing niche activities exhibit higher profitability and have lower risk. The syndication market now means that a bank making a loan does not have to be the entity that services it. This means banks in the future can better shape their risk profile and manage their lending books accordingly.

An interesting question for central banks is what the future Deposit Supply function will look like. If all three forms: open banking, traditional banking and challenger banks develop together, will the bank of the future have the same Deposit Supply function? The Klein ( 1971 ) general formulation assumes that deposits are increasing functions of implicit and explicit yields. As such, the very nature of central bank directed monetary policy may have to be revisited, as alluded to in the earlier discussion on digital money.

The client retention strategy (incumbents)

The competitive pressures suggest that incumbent banks need to focus on customer retention. Reichheld and Kenny ( 1990 ) found that the best way to do this was to focus on the retention of branch deposit customers. Obviously, another way is to provide a unique digital experience that matches the challengers.

Incumbent banks have a competitive advantage based on the information they have about their customers. Allen ( 1990 ) argues that where risk aversion is observable, information markets are viable. In other words, both bank and customer benefit from this. The strategic issue for them, therefore, becomes the retention of these customers when faced with greater competition.

Open Banking changes the dynamics of the banking information advantage. Borgogno and Colangelo ( 2020 ) suggest that the access to account (XS2A) rule that it introduced will increase competition and reduce information asymmetry. XS2A requires banks to grant access to bank account data to authorized third payment service providers.

The incumbent banks have a high-cost base and legacy IT systems. This makes it harder for them to migrate to a digital world. There are, however, also benefits from financial technology for the incumbents. These include reduced cost and greater efficiency. Financial technology can also now support platforms that allow incumbent banks to sell NPL’s. These platforms do not require the ownership of assets, they act as consolidators. The use of technology to monitor the transactions make the processing cost efficient. The unique selling point of such platforms is their centralized point of contact which results in a reduction in information asymmetry.

Incumbent banks must adapt a number of areas they got to adapt in terms of their liquidity transformation. They have to adapt the way they handle data. They must get customers to trust them in a digital world and the way that they trust them in a bricks and mortar world. It is no coincidence. When you go into a bank branch that is a great big solid building great big facade and so forth that is done deliberately so that you trust that bank with your deposit.

The risk of having rising non-performing loans needs to be managed, so customer retention should be selective. One of the puzzles in banking is why customers are regularly denied credit, rather than simply being charged a higher price for it. This credit rationing is often alleviated by collateral, but finance theory suggests value is based on the discounted sum of future cash flows. As such, it is conceivable that the bank of the future will use financial technology to provide innovative credit allocation solutions. That said, the dual risks of moral hazard and information asymmetries from the adoption of such solutions must be addressed.

Customer retention is especially important as bank competition is intensifying, as is the digitalization of financial services. Customer retention requires innovation, and that innovation has been moving at a very fast rate. Until now, banks have traditionally been hesitant about technology. More recently, mergers and acquisitions have increased quite substantially, initiated by a need to address actual or perceived weaknesses in financial technology.

The client acquisition strategy (challengers)

As intermediaries, the challenger banks are the same as incumbent banks, but designed from the outset to be digital. This gives them a cost and efficiency advantage. Anagnostopoulos ( 2018 ) suggests that the difference between challenger and traditional banks is that the former address its customers problems more directly. The challenge for such banks is customer acquisition.

Open Banking is a major advantage to challenger banks as it facilitates the changing of accounts. There is widespread dissatisfaction with many incumbent banks. Open Banking makes it easier to change accounts and also easier to get a transaction history on the client.

Customer acquisition can be improved by building trust in a brand. Historically, a bank was physically built in a very robust manner, hence the heavy architecture and grand banking halls. This was done deliberately to engender a sense of confidence in the deposit taking institution. Pure internet banks are not able to do this. As such, they must employ different strategies to convey stability. To do this, some communicate their sustainability credentials, whilst others use generational values-based advertising. Customer acquisition in a banking context is traditionally done by offering more attractive rates of interest. This is illustrated in Fig. 5 by the intersect of traditional banks with the market rate of interest, depicted where the line Γ crosses L 2 . As a result of the relationship with banking yield, teaser rates and introductory rates are common. A customer acquisition strategy has risks, as consumers with good credit can game different challenger banks by frequently changing accounts.

Most customer acquisition, however, is done based on superior service offering. The functionality of challenger banking accounts is often superior to incumbents, largely because the latter are built on legacy databases that have inter-operability issues. Having an open platform of services is a popular customer acquisition technique. The unrestricted provision of third-party products is viewed more favorably than a restricted range of products.

The banking as a service strategy (new entrants)

Banking from a customer’s perspective is the provision of a service. Customers don’t care about the maturity transformation of banking balance sheets. Banking as a service can be performed without recourse to these balance sheets. Banking products are brokered, mostly by new entrants, to individuals as services that can be subscribed to or paid on a fee basis.

There are a number banking as a service solutions including pre-paid and credit cards, lending and leasing. The banking as a service brokers are effectively those that are aggregating services from others using open banking to enable banking as a service.

The rise of banking as a service needs to be understood as these compete directly with traditional banks. As explained, some of these do this through peer-to-peer lending over the internet, others by matching borrows and sellers, conducting mediation as a loan broker. Such entities do not transform assets and do not have banking licenses. They do not have a branch network and often don not have access to deposits. This means that they have no insurance protection and can be subject to interest rate controls.

The new genre of financial technology, banking as a service provider, conduct financial services transformation without access to central bank liquidity. In a distributed digital asset world, the assets are stored on a distributed ledger rather than a traditional banking ledger. Financial technology has automated credit evaluation, savings, investments, insurance, trading, banking payments and risk management. These banking as a service offering are only as secure as the technology on which they are built.

The social media payment strategy (disintermediators and disruptors)

An intermediation bank is a conceptual idea, one created solely on a social networking site. Social media has developed a market for online goods and services. Williams ( 2018 ) estimates that there are 2.46 billion social media users. These all make and receive payments of some kind. They demand security and functionality. Importantly, they have often more clients than most banks. As such, a strategy to monetize the payments infrastructure makes sense.

All social media platforms are rich repositories of data. Such platforms are used to buy and sell things and that requires payments. Some platforms are considering evolving their own digital payment, cutting out the banks as middlemen. These include Facebook’s Diem (formerly Libra), a digital currency, and similar developments at some of the biggest technology companies. The risk with social media payment platform is that there is systemic counter-party protection. Regulators need to address this. One way to do this would be to extend payment service insurance to such platforms.

Social media as a platform moves the payment relationship from a transaction to a customer experience. The ability to use consumer desires in combination with financial data has the potential to deliver a number of new revenue opportunities. These will compete directly with the banks of the future. This will have implications for (1) the money supply, (2) the market share of traditional banks and, (3) the services that payment providers offer.

Further research

Several recommendations for research derive from both the impact of disintermediation and the four proposed strategies that will shape banking in the future. The recommendations and suggestions are based on the mentioned papers and the conclusions drawn from them.

As discussed, the nature of intermediation is changing, and this has implications for the pricing of risk. The role of interest rates in banking will have to be further reviewed. In a decentralized world based on crypto currencies the central banks do not have the same control over the money supply, This suggest the quantity theory of money and the liquidity preference theory need to be revisited. As explained, the Internet reduces much of the friction costs of intermediation. Researchers should ask how this will impact maturity transformation. It is also fair to ask whether at some point in the future there will just be one big bank. This question has already been addressed in the literature but the Internet facilities the possibility. Diamond ( 1984 ) and Ramakrishnan and Thakor ( 1984 ) suggested the answer was due to diversification and its impact on reducing monitoring costs.

Attention should be given by academics to the changing nature of banking risk. How should regulators, for example, address the moral hazard posed by challenger banks with weak balance sheets? What about deposit insurance? Should it be priced to include unregulated entities? Also, what criteria do borrowers use to choose non-banking intermediaries? The changing risk environment also poses two interesting practical questions. What will an online bank run look like, and how can it be averted? How can you establish trust in digital services?

There are also research questions related to the nature of competition. What, for example, will be the nature of cross border competition in a decentralized world? Is the credit rationing that generates competition a static or dynamic phenomena online? What is the value of combining consumer utility with banking services?

Financial intermediaries, like banks, thrive in a world of deficits and surpluses supported by information asymmetries and disconnectedness. The connectivity of the internet changes this dynamic. In this respect, the view of Schumpeter ( 1911 ) on the role of financial intermediaries needs revisiting. Lenders and borrows can be connected peer to peer via the internet.