About Stanford GSB

- The Leadership

- Dean’s Updates

- School News & History

- Commencement

- Business, Government & Society

- Centers & Institutes

- Center for Entrepreneurial Studies

- Center for Social Innovation

- Stanford Seed

About the Experience

- Learning at Stanford GSB

- Experiential Learning

- Guest Speakers

- Entrepreneurship

- Social Innovation

- Communication

- Life at Stanford GSB

- Collaborative Environment

- Activities & Organizations

- Student Services

- Housing Options

- International Students

Full-Time Degree Programs

- Why Stanford MBA

- Academic Experience

- Financial Aid

- Why Stanford MSx

- Research Fellows Program

- See All Programs

Non-Degree & Certificate Programs

- Executive Education

- Stanford Executive Program

- Programs for Organizations

- The Difference

- Online Programs

- Stanford LEAD

- Seed Transformation Program

- Aspire Program

- Seed Spark Program

- Faculty Profiles

- Academic Areas

- Awards & Honors

- Conferences

Faculty Research

- Publications

- Working Papers

- Case Studies

Research Hub

- Research Labs & Initiatives

- Business Library

- Data, Analytics & Research Computing

- Behavioral Lab

Research Labs

- Cities, Housing & Society Lab

- Golub Capital Social Impact Lab

Research Initiatives

- Corporate Governance Research Initiative

- Corporations and Society Initiative

- Policy and Innovation Initiative

- Rapid Decarbonization Initiative

- Stanford Latino Entrepreneurship Initiative

- Value Chain Innovation Initiative

- Venture Capital Initiative

- Career & Success

- Climate & Sustainability

- Corporate Governance

- Culture & Society

- Finance & Investing

- Government & Politics

- Leadership & Management

- Markets & Trade

- Operations & Logistics

- Opportunity & Access

- Organizational Behavior

- Political Economy

- Social Impact

- Technology & AI

- Opinion & Analysis

- Email Newsletter

Welcome, Alumni

- Communities

- Digital Communities & Tools

- Regional Chapters

- Women’s Programs

- Identity Chapters

- Find Your Reunion

- Career Resources

- Job Search Resources

- Career & Life Transitions

- Programs & Services

- Career Video Library

- Alumni Education

- Research Resources

- Volunteering

- Alumni News

- Class Notes

- Alumni Voices

- Contact Alumni Relations

- Upcoming Events

Admission Events & Information Sessions

- MBA Program

- MSx Program

- PhD Program

- Alumni Events

- All Other Events

- Operations, Information & Technology

- Classical Liberalism

- The Eddie Lunch

- Accounting Summer Camp

- Videos, Code & Data

- California Econometrics Conference

- California Quantitative Marketing PhD Conference

- California School Conference

- China India Insights Conference

- Homo economicus, Evolving

- Political Economics (2023–24)

- Scaling Geologic Storage of CO2 (2023–24)

- A Resilient Pacific: Building Connections, Envisioning Solutions

- Adaptation and Innovation

- Changing Climate

- Civil Society

- Climate Impact Summit

- Climate Science

- Corporate Carbon Disclosures

- Earth’s Seafloor

- Environmental Justice

- Operations and Information Technology

- Organizations

- Sustainability Reporting and Control

- Taking the Pulse of the Planet

- Urban Infrastructure

- Watershed Restoration

- Junior Faculty Workshop on Financial Regulation and Banking

- Ken Singleton Celebration

- Marketing Camp

- Quantitative Marketing PhD Alumni Conference

- Presentations

- Theory and Inference in Accounting Research

- Stanford Closer Look Series

- Quick Guides

- Core Concepts

- Journal Articles

- Glossary of Terms

- Faculty & Staff

- Researchers & Students

- Research Approach

- Charitable Giving

- Financial Health

- Government Services

- Workers & Careers

- Short Course

- Adaptive & Iterative Experimentation

- Incentive Design

- Social Sciences & Behavioral Nudges

- Bandit Experiment Application

- Conferences & Events

- Get Involved

- Reading Materials

- Teaching & Curriculum

- Energy Entrepreneurship

- Faculty & Affiliates

- SOLE Report

- Responsible Supply Chains

- Current Study Usage

- Pre-Registration Information

- Participate in a Study

Grameen Bank

- Priorities for the GSB's Future

- See the Current DEI Report

- Supporting Data

- Research & Insights

- Share Your Thoughts

- Search Fund Primer

- Affiliated Faculty

- Faculty Advisors

- Louis W. Foster Resource Center

- Defining Social Innovation

- Impact Compass

- Global Health Innovation Insights

- Faculty Affiliates

- Student Awards & Certificates

- Changemakers

- Dean Jonathan Levin

- Dean Garth Saloner

- Dean Robert Joss

- Dean Michael Spence

- Dean Robert Jaedicke

- Dean Rene McPherson

- Dean Arjay Miller

- Dean Ernest Arbuckle

- Dean Jacob Hugh Jackson

- Dean Willard Hotchkiss

- Faculty in Memoriam

- Stanford GSB Firsts

- Certificate & Award Recipients

- Teaching Approach

- Analysis and Measurement of Impact

- The Corporate Entrepreneur: Startup in a Grown-Up Enterprise

- Data-Driven Impact

- Designing Experiments for Impact

- Digital Business Transformation

- The Founder’s Right Hand

- Marketing for Measurable Change

- Product Management

- Public Policy Lab: Financial Challenges Facing US Cities

- Public Policy Lab: Homelessness in California

- Lab Features

- Curricular Integration

- View From The Top

- Formation of New Ventures

- Managing Growing Enterprises

- Startup Garage

- Explore Beyond the Classroom

- Stanford Venture Studio

- Summer Program

- Workshops & Events

- The Five Lenses of Entrepreneurship

- Leadership Labs

- Executive Challenge

- Arbuckle Leadership Fellows Program

- Selection Process

- Training Schedule

- Time Commitment

- Learning Expectations

- Post-Training Opportunities

- Who Should Apply

- Introductory T-Groups

- Leadership for Society Program

- Certificate

- 2023 Awardees

- 2022 Awardees

- 2021 Awardees

- 2020 Awardees

- 2019 Awardees

- 2018 Awardees

- Social Management Immersion Fund

- Stanford Impact Founder Fellowships and Prizes

- Stanford Impact Leader Prizes

- Social Entrepreneurship

- Stanford GSB Impact Fund

- Economic Development

- Energy & Environment

- Stanford GSB Residences

- Environmental Leadership

- Stanford GSB Artwork

- A Closer Look

- California & the Bay Area

- Voices of Stanford GSB

- Business & Beneficial Technology

- Business & Sustainability

- Business & Free Markets

- Business, Government, and Society Forum

- Second Year

- Global Experiences

- JD/MBA Joint Degree

- MA Education/MBA Joint Degree

- MD/MBA Dual Degree

- MPP/MBA Joint Degree

- MS Computer Science/MBA Joint Degree

- MS Electrical Engineering/MBA Joint Degree

- MS Environment and Resources (E-IPER)/MBA Joint Degree

- Academic Calendar

- Clubs & Activities

- LGBTQ+ Students

- Military Veterans

- Minorities & People of Color

- Partners & Families

- Students with Disabilities

- Student Support

- Residential Life

- Student Voices

- MBA Alumni Voices

- A Week in the Life

- Career Support

- Employment Outcomes

- Cost of Attendance

- Knight-Hennessy Scholars Program

- Yellow Ribbon Program

- BOLD Fellows Fund

- Application Process

- Loan Forgiveness

- Contact the Financial Aid Office

- Evaluation Criteria

- GMAT & GRE

- English Language Proficiency

- Personal Information, Activities & Awards

- Professional Experience

- Letters of Recommendation

- Optional Short Answer Questions

- Application Fee

- Reapplication

- Deferred Enrollment

- Joint & Dual Degrees

- Entering Class Profile

- Event Schedule

- Ambassadors

- New & Noteworthy

- Ask a Question

- See Why Stanford MSx

- Is MSx Right for You?

- MSx Stories

- Leadership Development

- Career Advancement

- Career Change

- How You Will Learn

- Admission Events

- Personal Information

- Information for Recommenders

- GMAT, GRE & EA

- English Proficiency Tests

- After You’re Admitted

- Daycare, Schools & Camps

- U.S. Citizens and Permanent Residents

- Requirements

- Requirements: Behavioral

- Requirements: Quantitative

- Requirements: Macro

- Requirements: Micro

- Annual Evaluations

- Field Examination

- Research Activities

- Research Papers

- Dissertation

- Oral Examination

- Current Students

- Education & CV

- International Applicants

- Statement of Purpose

- Reapplicants

- Application Fee Waiver

- Deadline & Decisions

- Job Market Candidates

- Academic Placements

- Stay in Touch

- Faculty Mentors

- Current Fellows

- Standard Track

- Fellowship & Benefits

- Group Enrollment

- Program Formats

- Developing a Program

- Diversity & Inclusion

- Strategic Transformation

- Program Experience

- Contact Client Services

- Campus Experience

- Live Online Experience

- Silicon Valley & Bay Area

- Digital Credentials

- Faculty Spotlights

- Participant Spotlights

- Eligibility

- International Participants

- Stanford Ignite

- Frequently Asked Questions

- Founding Donors

- Location Information

- Participant Profile

- Network Membership

- Program Impact

- Collaborators

- Entrepreneur Profiles

- Company Spotlights

- Seed Transformation Network

- Responsibilities

- Current Coaches

- How to Apply

- Meet the Consultants

- Meet the Interns

- Intern Profiles

- Collaborate

- Research Library

- News & Insights

- Program Contacts

- Databases & Datasets

- Research Guides

- Consultations

- Research Workshops

- Career Research

- Research Data Services

- Course Reserves

- Course Research Guides

- Material Loan Periods

- Fines & Other Charges

- Document Delivery

- Interlibrary Loan

- Equipment Checkout

- Print & Scan

- MBA & MSx Students

- PhD Students

- Other Stanford Students

- Faculty Assistants

- Research Assistants

- Stanford GSB Alumni

- Telling Our Story

- Staff Directory

- Site Registration

- Alumni Directory

- Alumni Email

- Privacy Settings & My Profile

- Success Stories

- The Story of Circles

- Support Women’s Circles

- Stanford Women on Boards Initiative

- Alumnae Spotlights

- Insights & Research

- Industry & Professional

- Entrepreneurial Commitment Group

- Recent Alumni

- Half-Century Club

- Fall Reunions

- Spring Reunions

- MBA 25th Reunion

- Half-Century Club Reunion

- Faculty Lectures

- Ernest C. Arbuckle Award

- Alison Elliott Exceptional Achievement Award

- ENCORE Award

- Excellence in Leadership Award

- John W. Gardner Volunteer Leadership Award

- Robert K. Jaedicke Faculty Award

- Jack McDonald Military Service Appreciation Award

- Jerry I. Porras Latino Leadership Award

- Tapestry Award

- Student & Alumni Events

- Executive Recruiters

- Interviewing

- Land the Perfect Job with LinkedIn

- Negotiating

- Elevator Pitch

- Email Best Practices

- Resumes & Cover Letters

- Self-Assessment

- Whitney Birdwell Ball

- Margaret Brooks

- Bryn Panee Burkhart

- Margaret Chan

- Ricki Frankel

- Peter Gandolfo

- Cindy W. Greig

- Natalie Guillen

- Carly Janson

- Sloan Klein

- Sherri Appel Lassila

- Stuart Meyer

- Tanisha Parrish

- Virginia Roberson

- Philippe Taieb

- Michael Takagawa

- Terra Winston

- Johanna Wise

- Debbie Wolter

- Rebecca Zucker

- Complimentary Coaching

- Changing Careers

- Work-Life Integration

- Career Breaks

- Flexible Work

- Encore Careers

- D&B Hoovers

- Data Axle (ReferenceUSA)

- EBSCO Business Source

- Global Newsstream

- Market Share Reporter

- ProQuest One Business

- Student Clubs

- Entrepreneurial Students

- Stanford GSB Trust

- Alumni Community

- How to Volunteer

- Springboard Sessions

- Consulting Projects

- 2020 – 2029

- 2010 – 2019

- 2000 – 2009

- 1990 – 1999

- 1980 – 1989

- 1970 – 1979

- 1960 – 1969

- 1950 – 1959

- 1940 – 1949

- Service Areas

- ACT History

- ACT Awards Celebration

- ACT Governance Structure

- Building Leadership for ACT

- Individual Leadership Positions

- Leadership Role Overview

- Purpose of the ACT Management Board

- Contact ACT

- Business & Nonprofit Communities

- Reunion Volunteers

- Ways to Give

- Fiscal Year Report

- Business School Fund Leadership Council

- Planned Giving Options

- Planned Giving Benefits

- Planned Gifts and Reunions

- Legacy Partners

- Giving News & Stories

- Giving Deadlines

- Development Staff

- Submit Class Notes

- Class Secretaries

- Board of Directors

- Health Care

- Sustainability

- Class Takeaways

- All Else Equal: Making Better Decisions

- If/Then: Business, Leadership, Society

- Grit & Growth

- Think Fast, Talk Smart

- Spring 2022

- Spring 2021

- Autumn 2020

- Summer 2020

- Winter 2020

- In the Media

- For Journalists

- DCI Fellows

- Other Auditors

- Academic Calendar & Deadlines

- Course Materials

- Entrepreneurial Resources

- Campus Drive Grove

- Campus Drive Lawn

- CEMEX Auditorium

- King Community Court

- Seawell Family Boardroom

- Stanford GSB Bowl

- Stanford Investors Common

- Town Square

- Vidalakis Courtyard

- Vidalakis Dining Hall

- Catering Services

- Policies & Guidelines

- Reservations

- Contact Faculty Recruiting

- Lecturer Positions

- Postdoctoral Positions

- Accommodations

- CMC-Managed Interviews

- Recruiter-Managed Interviews

- Virtual Interviews

- Campus & Virtual

- Search for Candidates

- Think Globally

- Recruiting Calendar

- Recruiting Policies

- Full-Time Employment

- Summer Employment

- Entrepreneurial Summer Program

- Global Management Immersion Experience

- Social-Purpose Summer Internships

- Process Overview

- Project Types

- Client Eligibility Criteria

- Client Screening

- ACT Leadership

- Social Innovation & Nonprofit Management Resources

- Develop Your Organization’s Talent

- Centers & Initiatives

- Student Fellowships

TymeBank Case Study: The Customer Impact of Inclusive Digital Banking

Full report.

This publication is also available in French and Spanish .

Executive Summary

This case study presents insights from customer research with TymeBank clients that bolsters CGAP’s hypotheses around how digital banks can support the mission of financial inclusion. As a fully digital South African bank that disproportionately serves low-income rural customers, TymeBank has created a suite of basic products that cater to the essential financial needs of those customers, namely a low-cost transactional account and a high-yield savings account. Judging from product uptake and client testimonials, these products add to a compelling value proposition that not only resonates with customers but improves their lives.

TymeBank’s distribution network, which is based on its partnerships with the nationwide Boxer and Pick n Pay (PnP) grocery store chains, helps to keep operational costs low and passes cost savings onto customers in the form of more affordable services. A clear majority of the bank’s customers cite affordability as a key source of value and the reason they opened a TymeBank account. The distribution network also extends the bank’s reach to areas that are underserved by traditional players. The affordability and accessibility likely explain why underserved segments, such as low-income women and rural customers, are over-represented in TymeBank’s (active) customer base as compared to the overall banked population in South Africa.

Despite having access to other banking options, TymeBank customers overwhelmingly see no compelling alternatives in the market. Crucially, the value customers see in the bank appears to be inversely related to income, with poorer customers reporting higher levels of satisfaction.

In today’s high-tech financial services landscape, which is often dominated by headlines about fintech startups and tech giants, it is easy to overlook the role banks can play in advancing financial inclusion. The high cost of running brick-and-mortar branch networks has traditionally inhibited banks from serving less profitable client segments, including the low-income groups that are the focus of financial inclusion. Banks have also been slow to adapt the digital innovations that have helped some newcomers reach these segments at lower cost. It is no surprise that some observers have questioned whether banks are even relevant to financial inclusion.

However, there are reasons to believe that banks can play an important role in financial inclusion if they overcome the challenges of their legacy systems and processes and digitize operations. In fact, banks have advantages over other types of financial services providers (FSPs) that may allow them to have an outsized impact on financial inclusion – if they are willing to expand down- market. Most importantly, banks do not face the same regulatory constraints as other providers. Whereas mobile money providers and fintechs generally cannot provide a wide array of financial products (ranging from savings to credit), banks can. License to intermediate retail deposits further plays to a bank’s advantage in the arena of digital credit. Banks can fund their lending portfolios with retail deposits that are typically cheaper than the other funding sources pure lenders use, which further reduces the cost of reaching low-income customers with credit.

CGAP previously presented three emerging business models in banking that we consider to be particularly promising for financial inclusion (Jeník and Zetterli 2020). These models are fully digital retail banks, marketplace banks, and Banking-as-a-Service (BaaS) (see Box 1). We conclude that they have the potential to deepen financial inclusion by:

- Lowering the cost of financial services;

- Improving access to a greater variety of services;

- Creating services that better meet the needs of various customer segments; and

- Improving the customer experience. 1

We analyzed several fully digital retail banks in a series of detailed case studies (Jeník, Flaming, and Salman 2020). One of these cases focused on TymeBank in South Africa. TymeBank is a fully digital retail bank founded with financial inclusion as a core business objective. Since its 2018 launch, the bank has onboarded over 4 million customers.

TymeBank offers low-income customers simple products at low prices, such as checking accounts, savings accounts, and debit cards – all through a distribution network that combines online and offline customer interaction based on partnerships with grocery store chains Boxer and PnP. In the area of credit products, TymeBank only offers a “buy now, pay later” option called MoreTyme. This case study provides a compelling example of how challenger banks can leverage digital technology to reach excluded customer segments with more affordable and useful products.

This paper builds on the TymeBank case study by examining the impact the bank’s services have had on low-income customers. By combining a quantitative analysis of TymeBank customer data with a phone-based survey of a randomly selected sample of low-income customers, the paper addresses the following questions:

- Does TymeBank serve low-income customers?

- Are its products relevant to low-income customers?

- What impact do the bank’s products have on low-income customers’ lives, in their own words?

The aim of this research is to shed light on the potential of digital banks to deepen financial inclusion in a way that improves the lives of low-income customers. CGAP is conducting additional research with other providers to better understand the impact of new financial services business models on customers. 2

TymeBank’s main value proposition consists of (i) simple, affordable, and accessible products; (ii) fast and automated onboarding; and (iii) incentive programs that appeal to target segments (e.g., the SmartShopper loyalty program). These are the qualities we would expect customers to point out when talking about the benefits of using TymeBank.

They are also important features that respond to three frequently cited barriers to financial inclusion: (i) expensive services, (ii) limited access points, and (iii) prohibitive know-your-customer (KYC) requirements. 3

Product affordability relies on TymeBank’s ability to maintain low operational costs and proportionally reduce them further as the bank grows. Current cost efficiency is due to the bank’s technology and microservice architecture (Flaming and Jeník 2020), its branchless model, and digitally facilitated onboarding. TymeBank onboards approximately 110,000 customers per month: about 93,500 through kiosks at an estimated cost of US$3 per customer, and about 16,500 via web at approximately US$0.60 per customer. 4

SOUTH AFRICA 5

South Africa enjoys relatively high levels of financial inclusion, including a banked adult population of approximately 85 percent in a market dominated by the country’s well-established commercial banks. However, many customers only use their bank account to receive government benefits; other use cases lag. There is little to no use of non-bank mobile money wallets.

Across demographic, socioeconomic, and geographic factors, financial inclusion levels positively corelate with higher age (people aged 18–29 are among those least included), urban areas, income level and regularity. Only 38 percent of individuals who reported having no income are banked, while 31 percent are entirely excluded.

METHODOLOGY

For the qualitative analysis based on customer interviews, 1,162 customers were screened from an overall sample of 10,000. The aim was to reach those TymeBank customers living in poverty (i.e., 70 percent or more likely to be living on less than US$5.50). Ultimately, 278 customers were identified for in-depth interviews. The screener surveys were conducted partly through interactive voice response (IVR) surveys and partly through live phone calls.

The quantitative analysis used customer data from TymeBank to assess the potential impact of the bank’s offering on its customer base, particularly individuals from groups that generally exhibit lower levels of financial inclusion. The data examined spanned a nine-month period from July 2020 to March 2021. The analyzed data correlated to active EveryDay account customers, defined as those who had performed a transaction within the past 30 days. Various sets of proxies were applied to estimate income level (e.g., onboarding location, outstanding balance, frequency of transactions, average size of transactions).

The analysis considered several important caveats:

a) We recognize that TymeBank is not representative of all fully digital retail banks in South Africa or elsewhere. The findings presented in this paper should not be interpreted as automatically applicable to other digital banks without careful consideration.

b) The research was conducted during the COVID-19 pandemic; some findings were or could be affected (e.g., as customer behavior changes in response to the pandemic).

c) Despite our best efforts to exclusively focus the analysis on low-income segments, we were unable to identify customers based on their stated income levels since TymeBank does not collect that information. Customer segmentation was performed through the previously mentioned set of proxies for the customer data analysis and through the screening questionnaire for the customer interviews. 6

d) The quantitative analysis focused on active customers with at least one transaction performed over the past 30 days, unless otherwise noted.

e) Where customers stated they had been financially excluded before opening a TymeBank account, we did not identify the underlying cause(s) of financial exclusion.

Key Findings

Does tymebank serve low-income customers.

Our research showed that TymeBank serves a higher proportion of low-income customers than the typical bank in South Africa, and a significantly higher portion of the most financially excluded segment.

Low-income customers in South Africa are relatively highly banked, although they are under-represented. South Africans earning US$200 per month or less constitute 47 percent of the population but only 41 percent of the banked population. 7 However, we estimate that this segment represents 48 percent of TymeBank’s active user base. 8

Among the three-quarters of TymeBank customers for whom data are available, 58 percent live in metropolitan areas and 42 percent in rural areas. This compares to South Africa’s rural population of 35 percent (as of 2016); we estimated this share to be even lower in 2021 (approximately 30 percent). 9 Hence, rural customers appeared to be noticeably overrepresented in the TymeBank user base.

Young, rural, low-income women comprise the most financially excluded and underserved segment in South Africa. This group forms 2.3 percent of South Africa’s banked population but 7 percent of TymeBank’s active base – nearly three times as much. 10 Finally, 13 percent of TymeBank’s active customers are first-time bank customers. 11

From a more general perspective, women in the low-income segment represent a higher-than- average share of the bank’s overall customer base sample (65 percent versus 57 percent),12 which suggests that low-income women particularly benefit from TymeBank’s services.

These findings lead us to conclude that TymeBank customers disproportionately seem to come from traditionally unbanked and underserved segments. In fact, the evidence suggests that the bank’s customer base may particularly skew toward the most underserved segments.

DOES TYMEBANK OFFER PRODUCTS THAT ARE RELEVANT TO LOW-INCOME CUSTOMERS?

Customers find TymeBank’s products useful and act upon features designed to promote certain behaviors.

The bank’s customers particularly value the low cost of its services and the convenience of access and usage. The lower their income, the more value customers seem to derive from its services. While the vast majority of TymeBank customers have previously held bank accounts, 67 percent say they see no good alternative to TymeBank (Figure 4). This response is despite the fact that, as of the time the research was conducted, the bank still only had a relatively modest payments and savings offering and had yet to launch credit products. (TymeBank has since launched MoreTyme, a “buy now, pay later” consumer credit product.) Customer endorsement seems driven by the strength of the bank’s value proposition and the low cost of its services. When asked, customers specifically appreciate the low fees (48 percent) and the high-yield savings account (38 percent).

Importantly, women make up a larger share of the total number of GoalSave (savings account) users compared to their representation in the overall customer base (3 percentage points higher). This finding suggests that female customers find value in the product, although they had slightly lower savings per user than men (US$58 versus US$59). The number of their deposits exceeds the number of withdrawals.

We did not find any significant differences in usage and product lifecycle patterns across income groups (aside from the frequency and size of transactions that correlate with income level), which suggests that TymeBank covers its customers’ essential needs across segments. The similarities in lifecycle (behavior patterns across products, such as most frequently performed type of transaction and their change over time) indicate that customers across income levels increase their engagement as they grow confident with the products.

However, important nuances do exist. For instance, the most excluded segment uses till machines for cash-in and cash-out transactions that are free-of-charge (and perhaps more accessible in certain areas), compared to the ATMs other segments prefer. This may be explained by price sensitivity that drives the preference for free till point withdrawals compared to ATM withdrawals, which are charged at US$0.61 per part of US$70.

The value generated for low(er) income customers will hopefully further expand as TymeBank expands its product offering (e.g., insurance and diverse credit products).

WHAT IMPACT DOES TYMEBANK HAVE ON CUSTOMERS’ LIVES?

Most customers report positive life changes due to their use of TymeBank. Importantly, levels of customer satisfaction increase as customer income decreases. This suggests that the TymeBank value proposition tailored to lower-income customers resonates well.

We relied on the actual voices of customers from the demand survey to gauge the impact the TymeBank offering had on its users. When asked, 73 percent of customers reported a positive change in quality of life attributable to TymeBank. The change could be associated with multiple factors. For instance, 80 percent of interviewed customers reported a decrease in the amount spent on bank fees, which is crucial for low-income segments that have historically experienced cost as one of the biggest barriers to financial inclusion. Nearly a third (31 percent) of customers who reported life improvement said that their access to financial services had expanded thanks to TymeBank. Customers also reported an improved ability to digitally transact and receive money (51 percent and 55 percent of all interviewees, respectively).

One of the most important findings concerned the ability to save. Seventy-three percent of interviewed customers reported an increase in their savings balance due to TymeBank. Savings likely drove customers’ ability to achieve their financial goals (68 percent) and improve financial resilience (32 percent).

These findings support our overall hypothesis that digital banks are well placed to deepen financial inclusion with cheaper, better products that reach beyond payments and are relevant to improving the lives of low-income customers.

It is critical to note that the high-interest yield on the GoalSave savings account was among the reasons most prominently cited by customers as driving them toward TymeBank. Our finding that female and young TymeBank customers were more likely to save using the bank service compared to what nationwide averages suggest was also important. While the national numbers show a 9 percentage point gap in formal savings between men and women (35 percent versus 26 percent), the gap among TymeBank customers favored women by 10 percentage points (45 percent versus 55 percent).

Our findings also revealed areas for improvement. Perhaps not surprisingly, TymeBank customers have not been spared the surge of fraud in South Africa. Ten percent of customers reported challenges concerning security and protection of funds. Six percent of respondents mentioned delays in service delivery and nearly the same share complained of issues related to digital access. Complaints were related to system downtime, clearing time (TymeBank is planning to offer real-time clearing), and the general concerns first-time users may have about their funds.

When asked about potential improvements, the presence of physical branches scored the highest (11 percent), followed by improved security (9 percent) related to the challenges mentioned in the previous paragraph and improved digital services (5 percent).

While these findings are encouraging, more research is needed before conclusive statements can be made about the broader role of digital banks in advancing financial inclusion. We encourage other experts to undertake similar research and add to the emerging evidence on the impact of digital banks on financial inclusion.

Acknowledgments

This case study features insights from research commissioned by CGAP and conducted by 60 Decibels and Genesis Analytics under the leadership of Ivo Jeník.

The author thanks CGAP colleagues Gayatri Vikram Murthy and Mehmet Kerse for reviewing this paper, and Gcinisizwe Andrew Mdluli for contributions and insights. Peter Zetterli and Xavier Faz oversaw the effort. Andrew Johnson led the editorial work.

This paper would not have been possible without the time and dedication of the team from TymeBank and TymeGlobal.

Flaming, Mark, and Ivo Jeník. 2020. “ How Does Tech Make a Difference in Digital Banking ?” CGAP blog post, 11 November.

Jeník, Ivo, Mark Flaming, and Arisha Salman. 2020. “ Inclusive Digital Banking: Emerging Markets Case Studies .” Working Paper. Washington, D.C.: CGAP.

Jeník, Ivo, and Peter Zetterli. 2020. “ Digital Banks: How Can They Deepen Financial Inclusion? ” Slide deck. Washington, D.C.: CGAP.

Download a PDF of this Case Study >>

1 To assess bank inclusivity, we developed and implemented a four-dimensional framework focused on cost, access, fit, and experience (CAFE). See Jeník and Zetterli (2020), page 42. In a business-to business (B2B) model, BaaS providers have other FSPs as their customers. Thus, their impact on end users is indirect.

2 see collection of cgap research on fintech and new financial services business models: www.cgap.org/fintech, 3 world bank global findex database (2017)., 4 atm-like machines placed in partner grocery stores – mainly pnp and boxer – allow for automated customer onboarding in less than five minutes., 5 this section is based on data from the finmark trust finscope (south africa) 2018 database., 6 the quantitative analysis used the average monthly inflows of customers originated at pnp value stores (us$271) and boxer stores (us$224) to estimate income level. the qualitative analysis estimated that 35 percent of tymebank’s customers live on less than us$5.50 per day, based on the screener survey findings., 7 the finmark trust finscope (south africa) 2018 database., 8 using place of origination (pnp value and boxer stores) as a proxy for low income., 9 south africa gateway . , 10 the finmark trust finscope (south africa) 2018 database., 11 n = 1,162., 12 comparing screened customers (n = 1,162) and interviewed customers (n = 278)., related resources, inclusive digital banking: emerging markets case studies, digital banks: how can they deepen financial inclusion, related research, open finance self-assessment tool and development roadmap, gender-intentional credit scoring, global landscape: data trails of digitally included poor (dip) people.

© 2024 CGAP

- Privacy Notice

- SUGGESTED TOPICS

- The Magazine

- Newsletters

- Managing Yourself

- Managing Teams

- Work-life Balance

- The Big Idea

- Data & Visuals

- Reading Lists

- Case Selections

- HBR Learning

- Topic Feeds

- Account Settings

- Email Preferences

Case Study: Will a Bank’s New Technology Help or Hurt Morale?

- Leonard A. Schlesinger

A CEO weighs the growth benefits of AI against the downsides of impersonal decision making.

Beth Daniels, the CEO of Michigan’s Vanir Bancorp, sat silent as her chief human resources officer and chief financial officer traded jabs. The trio had founded their community bank three years earlier with the mission of serving small-business owners, particularly those on the lower end of the credit spectrum. After getting a start-up off the ground in a mature, heavily regulated industry, they were a tight-knit, battle-tested team. But the current meeting was turning into a civil war.

- Leonard A. Schlesinger is the Baker Foundation Professor at Harvard Business School, where he serves as chair of its practice-based faculty.

Partner Center

- Browse All Articles

- Newsletter Sign-Up

BanksandBanking →

No results found in working knowledge.

- Were any results found in one of the other content buckets on the left?

- Try removing some search filters.

- Use different search filters.

Academia.edu no longer supports Internet Explorer.

To browse Academia.edu and the wider internet faster and more securely, please take a few seconds to upgrade your browser .

Enter the email address you signed up with and we'll email you a reset link.

- We're Hiring!

- Help Center

Case Study: Diffusion of Innovation, The case of Grameen Bank and BRAC

How innovation can spread is illustrated by the spread of a revolutionary new idea – that of microfinance. Muhammad Yunus, a professor, turned conventional banking on its head by inventing the concept of micro-loans. Returning to Bangladesh in the seventies, Dr Yunus was horrified to discover that just outside his academic compound thousands of people were dying of starvation. He writes in his book, Banker to the Poor, “That night I lay in bed ashamed that I was part of a society which could not provide $27 to forty-two able-bodied, hard-working, skilled persons to make a living for themselves.” How did micro-credit become such a huge industry? The case shows how the idea spread using the following four key elements in the diffusion process.

Related Papers

Tazul Islam

Matthew O. Jackson

Oxford Handbooks Online

Roy Mersland

Journal of Innovation and Entrepreneurship

Abu shaleh Musa

Md Rakibul Islam Rakib

Syed Ledrose

Kabir Hassan

Hans Dieter Seibel

Advances in Social Work

Saleh Ahmed

As one of the countries in the Global South, Bangladesh has experienced numerous development challenges since its liberation in 1971. Bangladesh has showcased how to fight against poverty and to initiate meaningful change and development in human lives. Nobel Prize (2006) winner Grameen Bank is one of the popular development innovations in the country. Since the beginning of this Bank in the early 1970s, microfinance and entrepreneurship development with small amounts of money have proliferated to nearly every corner of the globe with the paramount goal of alleviating global poverty and ensuring human development. Like all other new social science techniques, the societal revolution brought about by microfinance expansion has left substantial room for refinement and further support by empirical evidence. This article critically evaluates a non-governmental initiative to empower extremely poor women through entrepreneurial microfinance, and examines the socioeconomic impacts in achie...

Innovations: Technology, Governance, Globalization

Dr. Imran Matin

RELATED PAPERS

Monserrat Carrizales

Prabhat Pandey

rennes.inra.fr

Olivier Cantat

Pacific Journalism Review

Kate McMillan

Agrovigor: Jurnal Agroekoteknologi

fadjar rianto

Dr. Aroloye O Numbere

Design Philosophy Papers

Anthony H Fry

Andrea Iacovella

Physics Letters B

joseph gutierrez

Proquest Llc

Sandra L . Tarabochia

Materials & Design

Marwan Arbilei

2009 International Conference on Electrical and Electronics Engineering - ELECO 2009

saffet ayasun

Ashwaq T. Hashim

Journal of Financial Services Marketing

Genevieve O'Connor

Gender and women's studies

Cheryl Lawler Lynch, PhD, LCSW

Asian Pacific Journal of Cancer Prevention

Abbas sh mohamud Mohamed

Microchemical Journal

Arissa Pickler

pratyush mishra

European Neuropsychopharmacology

Richard Josiassen

Biochimica et Biophysica Acta (BBA) - Biomembranes

Francesca Oppedisano

Revista Mexicana de Ciencias Pecuarias

Teódulo Quezada Tristan

M. Azougagh

Eva Alfiatus Sholikhah

Maaike Loncke

RELATED TOPICS

- We're Hiring!

- Help Center

- Find new research papers in:

- Health Sciences

- Earth Sciences

- Cognitive Science

- Mathematics

- Computer Science

- Academia ©2024

- Candlesticks Book

- Stock Compare

- Superstar Portfolio

- Stock Buckets

- Nifty Heatmap

- *Now Available in Hindi

HDFC Bank Case Study 2021 – Industry, SWOT, Financials & Shareholding

by Jitendra Singh | Mar 4, 2021 | Case Study , Stocks | 1 comment

HDFC Bank Case Study and analysis 2021: In this article, we will look into the fundamentals of HDFC Bank, focusing on both qualitative and quantitative aspects. Here, we will perform the SWOT Analysis of HDFC Bank, Michael Porter’s 5 Force Analysis, followed by looking into HDFC Bank’s key financials. We hope you will find the HDFC Bank case study helpful.

Disclaimer: This article is only for informational purposes and should not be considered any kind of advisory/advice. Please perform your independent analysis before investing in stocks, or take the help of your investment advisor. The data is collected from Trade Brains Portal .

Table of Contents

About HDFC Bank and its Business Model

Incorporated in 1994, HDFC Bank is one of the earliest private sector banks to get approval from RBI in this segment. HDFC Bank has a pan India presence with over 5400+ banking outlets in 2800+ cities, having a wide base of more than 56 million customers and all its branches interlinked on an online real-time basis.

HDFC Limited is the promoter of the company, which was established in 1977. HDFC Bank came up with its 50 crore-IPO in March 1996, receiving 55 times subscription. Currently, HDFC Bank is the largest bank in India in terms of market capitalization (Nearly Rs 8.8 Lac Cr.). HDFC Securities and HDB Financial Services are the subsidiary companies of the bank.

HDFC Bank primarily provides the following services:

Note: If you want to learn Candlesticks and Chart Trading from Scratch, here’s the best book available on Amazon ! Get the book now!

- Retail Banking (Loan Products, Deposits, Insurance, Cards, Demat services, etc.)

- Wholesale Banking (Commercial Banking. Investment Banking, etc.)

- Treasury (Forex, Debt Securities, Asset Liability Management)

HDFC Bank Case Study – Industry Analysis

There are 12 PSU banks, 22 Private sector banks, 1485 urban cooperative banks, 56 regional rural banks, 46 foreign banks and 96,000 rural cooperative banks in India. The total number of ATMs in India has constantly seen a rise and there are 209,110 ATMs in India as of August 2020, which are expected to further grow to 407,000 by the end of 2021.

In the last four years, bank credit recorded a growth of 3.57% CAGR, surging to $1698.97 billion as of FY20. At the same time, deposits rose with a CAGR of 13.93% reaching $1.93trillion by FY20. However, the growth in total deposits to GDB has fallen to 7.9% in FY20 owing to pandemic crises, which was above 9% before it.

Due to strong economic activity and growth, rising salaries, and easier access to credit, the credit demand has surged resulting in the Credit to GDP ratio advancing to 56%. However, it is still far less than the developed economies of the world. Even in China, it is revolving around 150 to 200%.

As of FY20, India’s Retail lending to GDP ratio is 18% , whereas in developed economies (US, UK) it varies between 70% – 80%).

Michael Porter’s 5 Force Analysis of HDFC Bank

1. rivalry amongst competitors.

- The banking sector has evolved very rapidly in the past few years with technology coming in, and now it is not only limited to depositing and lending but various categories of loans and advances, digital services, insurance schemes, cards, broking services, etc.; hence, the banks face stiff competition from its rivals.

2. A Threat by Substitutes

- For services like mutual funds, investments, insurances, categorized loans, etc., banks are not the only option these days because a lot of niche players have put their foot in the specialized category, surging the threat by substitutes for the banks.

- Another threat for the traditional banks is NEO Banks. The Neo Banks are virtual banks that operate online, are completely digital, and have a minimum physical presence.

3. Barriers to Entry

- Banks run in a highly regulated sector. Strict regulatory norms, huge initial capital requirements and winning the trust of people make it very tough for new players to come out as a national level bank in India. However, if a company enters as a niche player, there are relatively fewer entry barriers.

- With RBI approving the functioning of new small finance banks, payment banks and entry of foreign banks, the competition has further intensified in the Indian banking sector.

4. Bargaining Power of Suppliers

- The only supply which banks need is capital and they have four sources for the capital supply viz. deposits from customers, mortgage securities, loans, and loans from financial institutions. Customer deposits enjoy higher bargaining power as it is totally dependent on income and availability of options.

- Financial Institutions need to hedge inflation, and banks are liable to the rules and regulations of the RBI which makes them a safer bet; hence, they have less bargaining power.

5. Bargaining Power of Customers

- In modern days, customers not only expect proper banking but also the quality and faster services. With the advent of digitalization and the entry of new private banks and foreign banks, the bargaining power of customers has increased a lot.

- In terms of lending, creditworthy borrowers enjoy a high level of bargaining power as there is a large availability of banks and NBFCs which are ready to offer attractive loans and services at low switching and other costs.

HDFC Bank Case Study – SWOT Analysis

Now, moving forward in our HDFC Bank case study, we will perform the SWOT analysis.

1. Strengths

- Currently, HDFC Bank is the leader in the retail loan segment (personal, car and home loans) and credit card business, increasing its market share each year

- The HDFC tag has become a sign of trust in the people as HDFC has come out as a pioneer not only in banking, but loans, insurances, mutual funds, AMC and brokerage.

- HDFC Bank has always been an institution of its words as it has, without fail, delivered its guidance and this has created a strong brand loyalty in the market for them.

- HDFC Bank has very well leveraged the technology to help its profitability, only 34% transaction via Internet Banking in 2010 to 95% transaction in 2020.

2. Weaknesses

- HDFC bank doesn’t have a significant rural presence as compared to its peers. Since its inception, it has focused mainly on high-end clients. However, the focus is shifting in the recent period as nearly 50% of its branches are now in semi-urban and rural areas.

3. Opportunities

- The average age of the Indian population is around 28 years and more than 65% of the population is below 35, with increasing disposable income and rising urbanization, the demand for retail loans is expected to increase. HDFC Bank, being a leader in retail lending, can make the best out of this opportunity.

- With modernization in farming and a rise in rural and semi-urban disposable income, consumer spending is expected to rise. HDFC Bank can increase its market share in these segments by grabbing this opportunity. Currently, the bank has only 21% of the branches in rural areas.

- A lot of niche players have set up their strong branches in respective segments, which has shown stiff competition and has shrined the market share and profit margin for the company. Example – Gold Loans, Mutual Funds , Brokerage, etc.

- In-Vehicle Financing (which is HDFC Bank’s major source of lending income), most of the leading vehicle companies are providing the same service, which is a threat to the bank’s business.

Asian Paints Case Study 2021 – Industry, SWOT, Financials & Shareholding

HDFC Bank’s Management

HDFC Bank has set high standards in corporate governance since its inception.

Right from sticking to their words to proper book writing, HDFC has never compromised with the banking standards, and all the credit goes to Mr. Aditya Puri, the man behind HDFC Bank, who took the bank to such great heights that today its market capitalization is more than that of Goldman Sachs and Morgan Stanley of the US.

In 2020, after 26 years of service, he retired from his position in the bank and passed on the baton of Managing Director to Mr. Shasidhar Jagadishan. He joined the bank as a Manager in the finance function in 1996 and with an experience of over 29 years in banking, Jagadishan has led various segments of the sector in the past.

Financial Analysis of HDFC Bank

- 48% of the total revenue for HDFC bank comes from Retail Banking, followed by Wholesale Banking (27%), Treasury (12%), and 13% of the total comes from other sources.

- Industries receive a maximum share of loans issued by HDFC bank, which is 31.7%, followed by Personal Loans and Services both at a 28.7% share of the total. Only 10.9% of the total loans are issued to Agricultural and allied activities.

- HDFC Bank has a 31.3% market share in credit card transactions, showing a growth of 0.23% from the previous fiscal year, which makes it the market leader, followed by SBI.

- HDFC Bank is the market leader in large corporate Banking and Mid-Size Corporate Banking with 75% and 60% share respectively.

- In Mobile Banking Transaction, the market share of HDFC bank is 11.8%, which has seen a degrowth of 0.66% in the current fiscal year.

- With each year, HDFC Bank has shown increasing net profit, which makes the 1-year profit growth (24.57%) greater than both 3-year CAGR (21.75%) and 5-year CAGR (20.78%).

- Capital Adequacy Ratio, which is a very important figure for any bank stands at 18.52% for HDFC Bank.

- As of Sept 2020 HDFC, is at the second position in bank advances with a 10.1% market share, which has shown a rise from 9.25% a year ago. SBI tops this list with a 22.8% market share, Bank of Baroda is at the third spot with a 6.68% share, followed by Kotak Mahindra Bank (6.35%).

- HDFC Bank is again at the second spot in the market share of Bank deposits with 8.6%. SBI leads with a nearly 24.57% market share. PNB holds 7.5% of the market share in this category, coming out as the third followed by Bank of Baroda with 6.89%.

HDFC Bank Financial Ratios

1. profitability ratios.

- As of FY20, the net profit margin for the bank stands at 22.87%, which has seen a continuous rise for the last 4 fiscal years. This a very positive sign for the bank’s profitability.

- The Net Interest Margin (NIM) has been fluctuating from the range of 3.85% to 4.05% in the last 5 fiscal years. Currently, it stands at 3.82% as of FY20.

- Since FY16, there has been a constant fall in RoE, right from the high of 18.26% to 16.4% as of FY20.

- RoA has been more or less constant for the company, currently at 1.89%, which is a very positive sign.

2. Operational Ratios

- Gross NPA for the bank has fallen from FY19 (1.36) to 1.26, which a positive sign for the company. A similar improvement is also visible in the Net NPA, currently standing at 0.36.

- The CASA ratio for the bank is 42.23%, which has been seeing a continuous fall since FY17 (48.03%). However, there has been a spike rise in FY17 as in FY16, it was 43.25 and in FY18, again came to the almost same level of 43.5.

- In FY19, Advance Growth witnessed a massive spike from 18.71 level in FY18 rising to 24.47%. However, in FY20, it again fell nearly 4 points, coming down to 21.27%.

HDFC Bank Case Study – Shareholding Pattern

- Promoters hold 26% shares in the bank, which has been almost at the same level for the last many quarters. In the December quarter a years ago, the promoter holding was 26.18%. The marginal fall is only due to Aditya Puri retiring and selling few shares for his post-retirement finance, which he stated.

- FIIs own 39.95% shareholding in the bank, which has been increasing for years in every quarter. HDFC bank has been a darling share in the investor community.

- 21.70% of shares are owned by DIIs as of December Quarter 2020. Although it is less than the SeptQ2020(22.90%), it is still far above the year-ago quarter (21.07).

- Public holding in HDFC bank is 12.95% as of Dec Q2020, which has tanked from the year-ago quarter (14.83%) as FIIs increasing their share, which is evident from the rising share prices.

Closing Thoughts

In this article, we tried to perform a quick HDFC Bank case study. Although there are still many other prospects to look into, however, this guide would have given you a basic idea about HDFC Bank.

What do you think about HDFC Bank fundamentals from the long-term investment point of view? Do let us know in the comment section below. Take care and happy investing!

Start Your Stock Market Journey Today!

Want to learn Stock Market trading and Investing? Make sure to check out exclusive Stock Market courses by FinGrad, the learning initiative by Trade Brains. You can enroll in FREE courses and webinars available on FinGrad today and get ahead in your trading career. Join now!!

Nice can I get full case

Submit a Comment Cancel reply

Your email address will not be published. Required fields are marked *

Search Topic or Keyword

Trending articles.

Recent IPO’s

- JNK India IPO Review 2024 – GMP, Financials And More

- Bharti Hexacom IPO Review 2024 – GMP, Financials And More

- SRM Contractors IPO Review 2024 – GMP, Financials And More

- Krystal Integrated Services IPO Review 2024 – GMP, Financials & More

- Popular Vehicles IPO Review – GMP, Financials & More

Easiest Stock Screener Tool!

Best stock discovery tool with +130 filters, built for fundamental analysis. Profitability, Growth, Valuation, Liquidity, and many more filters. Search Stocks Industry-wise, Export Data For Offline Analysis, Customizable Filters.

- — Stock Screener

- — Compare Stocks

- — Stock Buckets

- — Portfolio Backtesting

Start your stock analysis journey with Trade Brains Portal today. Launch here !

Keep the Learning On!

Subscribe to Youtube to watch our latest stock market videos. Subscribe here .

Case Study: The Collapse of Silicon Valley Bank and Its Global Impact

“The downfall of SVB has left investors and depositors scrambling, as the domino effect threatens the stability of the global financial system.”

Introduction

The Silicon Valley Bank (SVB) is one of the leading U.S. banks in the fintech space, and its collapse has created an aftershock effect throughout the global financial system. Investors and depositors have uncertainties about the situation as the Federal Deposit Insurance Corporation (FDIC) intervenes to take control of the bank in question. In this article, we will analyze the international impact of SVB’s downfall on depositors, the financial markets, cryptocurrencies, and other banks.

Why Does It Matter?

As Emil Åkesson, Chairman and President of CLC & Partners, stated in his article on nasdaq.com , “ If things are bad in the U.S., things are bad all over. ” If the SVB issue is not addressed properly, it can lead to greater global problems with a domino effect.

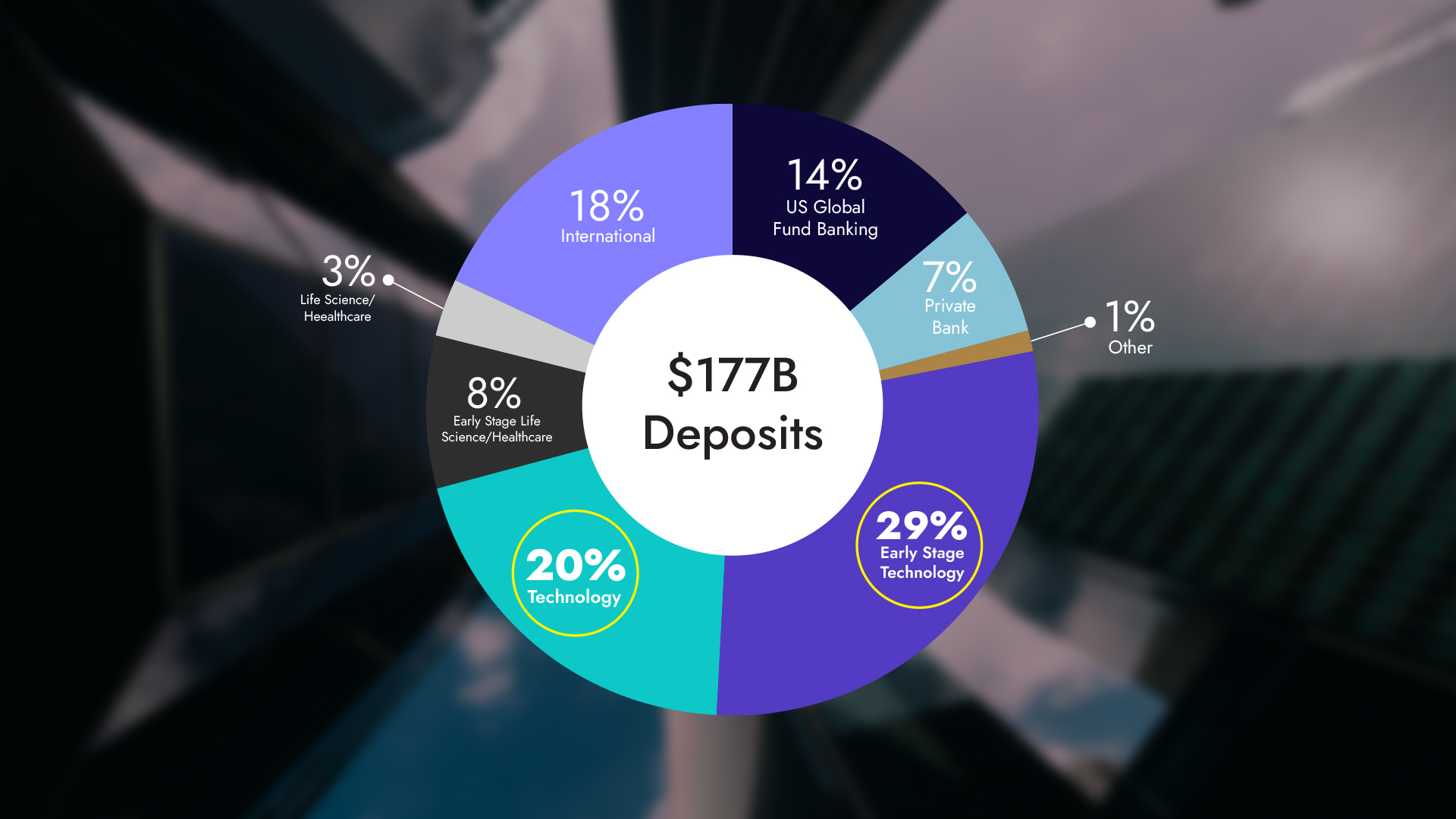

Silicon Valley Bank is distinguished as being a strong stakeholder that serves tech startups, life science and healthcare companies, private equity firms, and venture capital funds. SVB stands out holding the 16th position amongst the largest banks in the U.S. with 4,100+ banks operating all over the country. Its collapse has sent shockwaves throughout the global markets and also raised concerns about the future of fintech, technology startups, and innovation in the U.S. economy.

Before its breakdown, SVB’s holdings and assets were valued around at $210 billion, with $175 billion in deposits. Although this may seem like a small fraction of the total U.S. bank deposits of $18 trillion, it’s important to note that nearly $6 trillion of those deposits are held in small banks. In addition, SVB falls into the category of large banks, with its size and efficacy in the fintech industry being significant factors. In fact, this is the largest bank failure in the U.S. since 2008 Washington Mutual Bank failure.

The impact of SVB’s breakdown extends beyond its immediate clients. As the primary financial supporter of technology startups and venture capital funds, SVB’s failure could hinder the growth and development of future tech giants like Apple, Google, and Tesla in their early days. These startups rely on funding from various sources, especially venture capital firms. SVB plays a critical and central role in this ecosystem by providing commercial banking services to these companies and funds, fueling the technological innovation that has made the U.S. a global powerhouse. Therefore, it is essential for the U.S. to serve a safe and sound banking system to secure its position in the technology race.

Approximately, 29% of SVB’s deposits belong to technology startups and companies, potentially putting the next generation of industry-disrupting ideas at risk. The collapse of SVB is not only a financial crisis but also a potential innovation catastrophe. As these tech startups and venture capital funds search for new banking partners and possible financing opportunities, the U.S. must address the reverberations of SVB’s breakdown to preserve its status as a leader in innovation and prevent a possible slowdown in the growth of its tech sector.

How Did SVB Get Here?

We can trace the roots of SVB’s collapse back to 2022, when the U.S. raised interest rates to combat inflation, successfully lowering the inflation from 9% to 6% and aiming to further reduce it to 4%. As interest rates increased, the availability of capital diminished. SVB and similar banks had been providing cash flow to startups, with investors channeling their money into venture capital funds to support these projects. The startups would then use the funds to grow and eventually repay their debts. If these startups succeeded, the venture capital funds would generate substantial returns for their investors, despite the high risk.

However, the interest rates started to rise in 2022, and investors shifted their attention to low-risk deposits and bonds with higher yields which led to difficulties for venture capital funds in raising capital. Consequently, startups encountered challenges in securing funds and even struggled to pay their employees’ salaries. With the decrease in fundraising traffic, startups had to dip into their SVB bank accounts to cover these expenses, causing SVB’s total deposits to shrink. Simultaneously, SVB’s investments and shares in these sectors suffered as the startups and tech companies could no longer grow.

SVB held the top position in the Q4 of 2022 with 55.4% of their total funds invested. The bank’s deposit funding predominantly consisted of early tech startups and tech companies, providing them with fundraising by acquiring shares and receiving interest payments in return. Both investors and companies held their money in SVB, which the bank then used to make risky investments in more startups. However, with an investment-to-holding ratio of over 55%, SVB’s exposure was a very high and unorthodox one.

Ultimately, SVB failed to accurately assess the risks associated with their investments in these startups given rising interest rates. While it may not be fair to label this approach as inherently flawed, the uncontrolled inflation rate necessitated an increase in the interest rates, which proved to be the tipping point. In the end, SVB found itself unable to repay the $175 billion in deposits. The following day, SVB experienced a bank run and panicked customers withdrew $42 billion from SVB. To cover the shortfall, the bank attempted to sell its shares in tech startups and companies which led to a significant drop in their value and intensified the crisis.

The Bond Backlash

A sudden surge in interest rates can create a chain of events that sends shockwaves throughout the financial landscape, shaking the very foundation of previously issued bonds. The allure of new bonds, offering higher returns in the wake of rising interest rates, leads investors to flee for safer havens with high returns, outshining the older bonds with lower yields. As a result, bondholders seeking to sell their older bonds must reduce the prices to compete with the more appealing new bonds and this eventually leads to a capital loss.

Banks generally tend to have big holdings of government bonds that they can easily liquidate in times of crisis. Unfortunately, SVB had made considerable investments in long-term bonds when the interest rates were much lower than they are now. When the U.S. aggressively raised interest rates by 4.5%, the market value of SVB’s older long-term bonds experienced a sharp decline. This situation resulted in a $1.8 billion loss in the market value of their bond investment for SVB. These consecutive events dealt a double blow to the bank, ultimately contributing to SVB’s collapse.

The FDIC and Depositor Insurance

In the United States, the deposits are insured up to at least $250,000 per depositor in the FDIC-insured banks providing a safety net for depositors in case of bank failures. However, this limit has become a discussion topic with the SVB case.

SVB’s Q4 2022 data revealed that only 2.7% of its account holders had deposits below $250,000, which means 97.3% of the depositors had uninsured amounts exceeding the FDIC limit. These uninsured deposits are at risk of being lost, amounting to over $150 billion.

- The Existentialists : People made their own decisions and therefore should face the consequences of their own choices.

- The Concerned : If the FDIC and the government don’t intervene, it could lead to a much bigger financial crisis, affecting everyone on a global scale.

SVB, Stocks, and Commodities

SVB’s collapse has had a significant impact on global markets, with financial stocks losing $465 billion in market value in just two days. Gold prices have rallied by up to 10% as investors were seeking a safe haven. With this incident, the U.S. might have failed to fight inflation, at least for a while.

SVB and Cryptocurrencies

The collapse of SVB have had a notable impact on cryptocurrencies, particularly Bitcoin and Ethereum being the safe haven of the crypto market, which have surged in value following the bank’s downfall. Around $100 billion has moved to the crypto market in the following week, making Bitcoin, Ethereum, and altcoins such as Solana and Cardano reach new heights. Investors have been driven away from traditional banking towards the decentralised, leading to Bitcoin reaching a nine-month high.

However, every silver lining has a cloud. USDC, a stablecoin pegged to the U.S. dollar and managed by Circle, serves as a reliable medium of exchange without the volatility of other cryptocurrencies. Circle maintains a one-to-one reserve, holding one dollar for each USDC issued. Of the $40 billion raised from users, Circle invested $32 billion in short-term U.S. government bonds, securing 77% of the funds. The remaining 23%, or $3.3 billion, was held in cash, leaving 8% of USDC’s backing at risk. As a result, the theoretical value of 1 USDC should have dropped to $0.92 at the moment, casting a shadow over the stability of stablecoins.

Following the SVB news, Circle’s delayed response caused USDC’s value to plummet to the $0.8 range. Eventually, Circle announced that they had anticipated the situation and requested SVB to return the funds. U.S. regulators intervened, and USDC’s value returned to normal levels.

Circle has also stated that they are also committed to compensating for any losses if they cannot recover the funds from SVB. While this may not be a significant challenge for Circle, as they earn approximately $1.6 billion in interest annually from their bond investments, the primary issue was their delayed statement. However, Circle should have made this statement earlier to prevent panic selling and financial loss for USDC holders.

Why Blockchain Technology Shines?

While all of these were happening, some of the C-levels of the SVB were selling their shares. Gregory W. Becker, CEO of SVB, sold 11% of his shares on 27th February. Some of them started to sell their shares even more than a month ago starting at the beginning of February. Even though it was publicly available, nobody can blame individuals in a situation where the government itself couldn’t foresee and prevent this from happening. On a legal level, there seems no problem with this, but in terms of ethics, it does not look good, and Greg Becker may have a hard time finding support.

The SVB collapse highlights the advantages of blockchain technology, which offers transparency and traceability. In a centralized banking system, individuals must trust the bank, and tracing transactions can be difficult even for governments. With blockchain, all transactions are transparent and immutable, and warning systems such as Blocknative can be put in place for significant withdrawals like the SVB scandal. If this had occurred on a blockchain-based platform, investors could have been warned earlier when the bank’s C-level executives sold their shares. Unfortunately, the fintech industry has failed in educating the public about these warning system benefits. This highlights the need for improved communication and transparency in the financial industry and as CLC & Partners, we are committed to informing our audience.

The 3S Trio: Silvergate, SVB, and Signature Bank

Silvergate Capital, SVB, and Signature Bank, all facing financial issues, have caused turmoil in the crypto-friendly banking space. The closures of these banks, coupled with regulatory and legal investigations, have made it difficult for crypto companies to rely on traditional banking partners.

What’s Next for SVB and Its Depositors?

A consortium of private equity firms led by The Bank of London has submitted formal proposals to His Majesty’s Treasury to acquire SVB, but it remains uncertain whether the U.S. government will allow such a move due to potential privacy concerns.

U.S. Treasury Secretary Janet Yellen has announced that there will be no bailout for SVB. However, Yellen and the FDIC declared that additional funding will be made available to ensure all deposits will be paid in full regardless of the amount. The Fed also plans to provide funding to eligible depository institutions to support depositor needs. It should be noted that this issue should be solved very carefully to avoid providing freedom and relief to the other banks in the U.S. in terms of taking relentless risks with such a remedy.

All in all, the dramatic downfall of Silicon Valley Bank has left far-reaching consequences, affecting investors, depositors, and the global financial system. While the FDIC and the government are stepping in to prevent a total meltdown, it’s essential to monitor the situation closely and learn from this crisis to better prepare for future financial disruptions. As our chairman and president Emil Åkesson says, “history repeats itself, again,” and it will sure do again. A detailed case study like this article will definitely help us to extract valuable lessons to safeguard against future economic disruptions.

The financial world needs a leap forward, and we at CLC & Partners are eager to provide our community with our team’s valuable insights and extensive experiences to help you stay ahead of the curve. Follow CLC Blog to stay tuned and with truth!

CLC Homepage

© 2023 CLC & Partners All Rights Reserved.

SUBSCRIBE TO OUR UPCOMING NEWSLETTER

- INSTRUCTOR INFORMATION

- SUPPLEMENTAL VIDEOS

- FUNDAMENTAL FACTORS DIRECTIONS

- GLOSSARY OF TERMS

- DAILY NATURAL GAS PRICES

- LIGHT SWEET CRUDE OIL (WTI) FUTURES

- HENRY HUB NATURAL GAS FUTURES

- WEEKLY NATURAL GAS STORAGE REPORT

- WEEKLY PETROLEUM STATUS REPORT

- US NUCLEAR PLANT STATUS REPORT

- Academic Integrity and Citation Style Guides

- Using the Penn State Library

- GETTING HELP

Case Study 1: Barings Bank, PLC.

In February 1995, Nick Leeson, a “rogue” trader for Barings Bank, UK, single-handedly caused the financial collapse of a bank that had been in existence for hundreds of years. In fact, Barings had financed the Louisiana Purchase between the US and France in 1803. Leeson was dealing in risky financial derivatives in the Singapore office of Barings. He was the lone trader there and was betting heavily on options for both the Singapore (SIPEX) and Nikkei exchange indexes. These are similar to the Dow Jones Industrial Average (DJIA) and the S&P500 indexes here in the US.

In the early 90s, Barings decided to get into the expanding futures/options business in Asia. They established a Tokyo office to begin trading on the Tokyo Exchange. Later, they would look to open a Singapore office for trading on the SIMEX. Leeson requested to set up the accounting and settlement functions there and direct trading floor operations (different from trading). The London office granted his request and he went to Singapore in April 1992. Initially, he could only execute trades on behalf of clients and the Tokyo office for "arbitrage" (Lesson 10) purposes. After a good deal of success in this area, he was allowed to pursue an official trading license on the SIMEX. He was then given some "discretion" in his executions, meaning; he could place orders on his own (speculative, or "proprietary" trading).

Even after given the right to trade, Leeson still supervised accounting and settlements. There was no direct oversight of his "book" and he even set up a "dummy" account in which to funnel losing trades. So, as far as the London office of Barings was concerned, he was always making money because they never saw the losses and rarely questioned his request for funds to cover his "margin calls" (Lesson 3). He took on huge positions as the market seemed to "go his way." He also "wrote" options, taking on huge risk (Lesson 10).

He was, in fact, perpetuating a "hoax" in his record-keeping to hide losses. He would set the prices put into the accounting system and "cross-trade" between the legitimate, internal, accounts and his fictitious "88888" account. He would also record trades that were never executed on the Exchange.

In January 1995, a huge earthquake hit Japan, sending its financial markets reeling. The Nikkei crashed, which adversely affected Leeson's position (remember, he had been selling options). It was only then that he tried to hedge his positions, but it was too late. By late February, he faxed a letter of resignation, and when his position was discovered, he had lost $1.4 billion USD. Barings, the bank which financed the Louisiana Purchase between the US and France, became insolvent and was sold to a competing bank for $1.00!

(If you are interested in more details regarding this infamous case, you can read " Rogue Trader " by Nick Leeson himself. There is also a movie of the same name starring Ewan McGregor which should be available on Netflix or DVD.)

The following two case studies are brief descriptions of similar, catastrophic losses by traders with little, or no, oversight.

Optional video: Nick Leeson, The Rogue Trader

You can watch the complete interview here .

- Revolutionizing Digital Communication: The Power of Olly and AI

- AI-Powered Video Editing with Snapy.ai: The Future of Content Creation is Here

- Dawn of AI-Powered Video Editing: Transform Your Videos with Silence Remover Online

- The Dawn of Generative AI: Why and How to Adopt it for your Business

- Harnessing the Power of Generative AI for Business Innovation: An Exclusive Consultancy Approach

Original content with a single minded focus on value addition.

Case Study: The YES Bank Crisis

Harkirat Singh, Ashok Kapur, and Rana Kapoor instituted a bank called YES bank in 2004, which became the 4th largest private sector bank in India. The team at YES bank established a customer-centric and service-driven Indian bank for the future corporates of the country. It released its IPO (Initial public offering) and kept progressing until the global financial crisis of 2008. Harkirat Singh left the bank in a very initial period whereas Ashok Kapur, unfortunately, died in the 2008 terrorist attack in Mumbai. However, to achieve success the bank started aggressively focusing on its operations.

The rise of YES bank:

A lot of companies rely on private banks for their funds. And YES bank turned out to be the go-to bank for them. They acquired many clients for all operations and for some of them, it was the only banking partner for UPI transactions such as Swiggy, Phonepe, Flipkart, Redbus, etc. Looking at the growth of the bank, people started depositing more and more, essentially, this value grew to 2 lakh crores for the bank. YES bank attained its peak and the highest confidence among depositors and rating agencies.

The Collapse:

However, as they say, it is only when everything is looking alright is when things go wrong. As soon as the bank reached its peak of success, the bank (owing to the overwhelming response they received) started lending billions to companies. However, some of their clients were already under financial stress – these included Dewan Housing Finance Corp. Ltd (DHFL), Infrastructure Leasing and Financial Services ( IL&FS ), Anil Ambani’s Reliance group, the Zee group, and Subhash Chandra’s Essel group and the likes.

Now, this led to a huge problem because these companies really had no way to pay their debts back to the bank and were in no way the safe investments. A lot of questions were raised as to why the financial assistance was given to these companies, were the correct contingencies in place?

All of these issues led to the following in the coming years:

- Outstanding loans of YES bank grew from INR 55,000 crore in FY14 to INR 2.41 trillion in FY19

- UBS, a global financial services company raised concerns about the asset quality of the YES bank. They released a report mentioning the rising Non-performing assets (NPAs) of the bank. Despite knowing the financial inability of existing borrowers, the bank lent more money to them which eventually proved to be the NPAs for the bank

- On 5th March 2020 RBI put YES bank under moratorium. With this regulation, the people having accounts with the bank could withdraw only INR 50,000 and this continued till 3rd April 2020

Negative ratings of rating agencies, the UBS report, RBI’s correcting measures on the bank for under-reporting NPAs, and finally the moratorium imposed led to panic among the depositors and the shareholders which triggered them to withdraw their investments and sell the stocks respectively. The confidence of people went down and so the share price. From INR 1400 per share, it came down to mere INR 5 per share in early 2020s. Furthermore, the Enforcement Directorate (ED) arrested Rana Kapoor under the case of money laundering of about INR 4,300 crore.

Current Rescue plan:

- The government took over the bank and came with a draft plan which said State bank of India (SBI) will buy 49% stake and bring in the needed capital

- The investing bank will not reduce its holding in the new bank below 26% before completion of 3 years

- All the employees will continue to work at the same pay for at least for one year

- AT1 bonds of worth around INR 10,800 crore to be wiped out which will bring back capital in the bank but leave the customers with a huge loss

- RBI opened INR 60,000 crore as an emergency credit line for the bank

- ICICI bank took 7.97% stake in YES bank

Needless to say, the current economic situation owing to CoVID-19 is going to be difficult for the bank to recover in the coming months. After PMC bank’s fall, this was the second banking crisis reported in the country. First-ever case in India which cancelled AT1 bonds issued to investors of worth INR 8,415Cr.

That’s it for this piece. If you liked the content, go ahead and share it on WhatsApp or Twitter .

Join the community of 5000+ folks by subscribing to our newsletter.

- Case study: The Rise and Fall of WeWork

- Sony Walkman Case study: How it changed the way we listen to Music

You May Also Like

What is article 370? Kashmir’s special status explained

Winning in Unchartered waters – ZA Consulting’s FMCG case study

Story of Titan: India’s most successful consumer brand