Reading Lists +

The review +, 46 possible stock market strategies from academics get a retest.

9 March 2022

Research by

- Athanasse Zafirov

- Corporate Investment

- Stock Market

- Corporate Finance

- Stock Returns

We won’t call it debunking, but not all investing tips hold up

For nearly 3,000 years, bloodletting was an accepted medical practice for all types of maladies. It was only in the early 1800s when some doctors carefully reviewed data on the practice that they realized bloodletting didn’t improve patients’ health, and may sometimes be harmful.

Such review of accepted theories is currently a growing field among social and natural scientists. Peer-reviewed research is increasingly being thrown back into the review process to see if stands up.

Opt In to the Review Monthly Email Update.

A working paper by the University of Lausanne’s Amit Goyal, UCLA Anderson’s Ivo Welch and Athanasse Zafirov, a Ph.D. student, seeks to prevent the financial equivalent of bloodletting. Their meta-research — the term given for research on research — on papers published in top academic journals finds that many investing factors don’t hold up. To be precise, the 46 variables aren’t full-blown market strategies, but rather observed correlations that could form the basis for a strategy.

Past Performance May Not Be Indicative of Future Results

Building on Goyal and Welch’s 2008 paper that studied the predictive success of 17 variables, the researchers survey 26 papers identifying 29 variables considered useful in predicting the equity premium — the total rate of return on the stock market minus the prevailing short-term interest rate. The 17 variables from the 2008 paper are also reexamined. The researchers’ findings suggest that most of the variables have lost their predictive ability when tested on datasets extended to the end of 2020. A few variables do show flickers of promise but not overwhelming success across the researchers’ evaluation metrics.

The researchers’ first goal was to replicate the original findings of the papers’ authors. This involved recreating the variables and recalculating the reported statistics on the variables’ ability to predict the equity premium. Goyal, Welch and Zafirov were able to confirm the papers’ original findings, using the original dataset, on all but two of the papers. (The two remaining papers had data issues.)

The datasets to create the variables were then extended through December 2020, and the predictions for each of the 29 variables from the papers and the original 17 variables from the 2008 paper were retested.

The datasets in the papers ended between 2000 and 2017 and began as early as 1926. When building a predictive model, a researcher will typically split a dataset into at least two samples —one sample to train the model and another sample, typically the data from the latest years, to test the model. By extending the original datasets with data to the end of 2020 and starting the test sample 20 years after the start of the training sample, the components of these samples were slightly different than the samples used in the papers. It’s worth noting that the new data only made up a small percentage of the overall datasets.

“Because our paper reuses the data that the authors themselves had originally used to discover and validate their variables and theories, all that the predictors had to do in the few added years was not to ‘screw up’ badly.”

Nonetheless, of the 46 variables, only five managed to predict at a statistically significant level on the samples in the extended dataset.

But statistics are one thing, and investment performance is another. As a second test, Goyal, Welch and Zafirov devised simple investment strategies using the variables’ predictions to time investments by determining whether to go long or short the market and weighting the investments. The results of the investment strategies were compared with a buy-and-hold strategy. None of the five variables was able to significantly outperform the buy-and-hold approach in any of the investment strategies. Across all of the variable predictors, half lost money in the simplest investment strategy that used the variable to determine whether to go long or short.

Why Does the Performance Degrade?

The researchers suggest that the deterioration in predictive performance is at least partly explained by the fact that the market has shown greater variety in regimes over the last 20 years with many steep downturns. Campbell R. Harvey of Duke University and Yan Liu of Purdue University have performed similar meta-research and suggest that over-adapting the model to a particular data set may also be a factor due to authors running numerous backtests (simulations over historical data); they further suggest increasing necessary performance thresholds (raising the bar) as the number of backtests increase. Finally, a more generous explanation may be that as the predictive variables become well known by market practitioners, they lose their edge, just like a stock tip — when those tipped off start buying, the stock price rises and the tip loses its value.

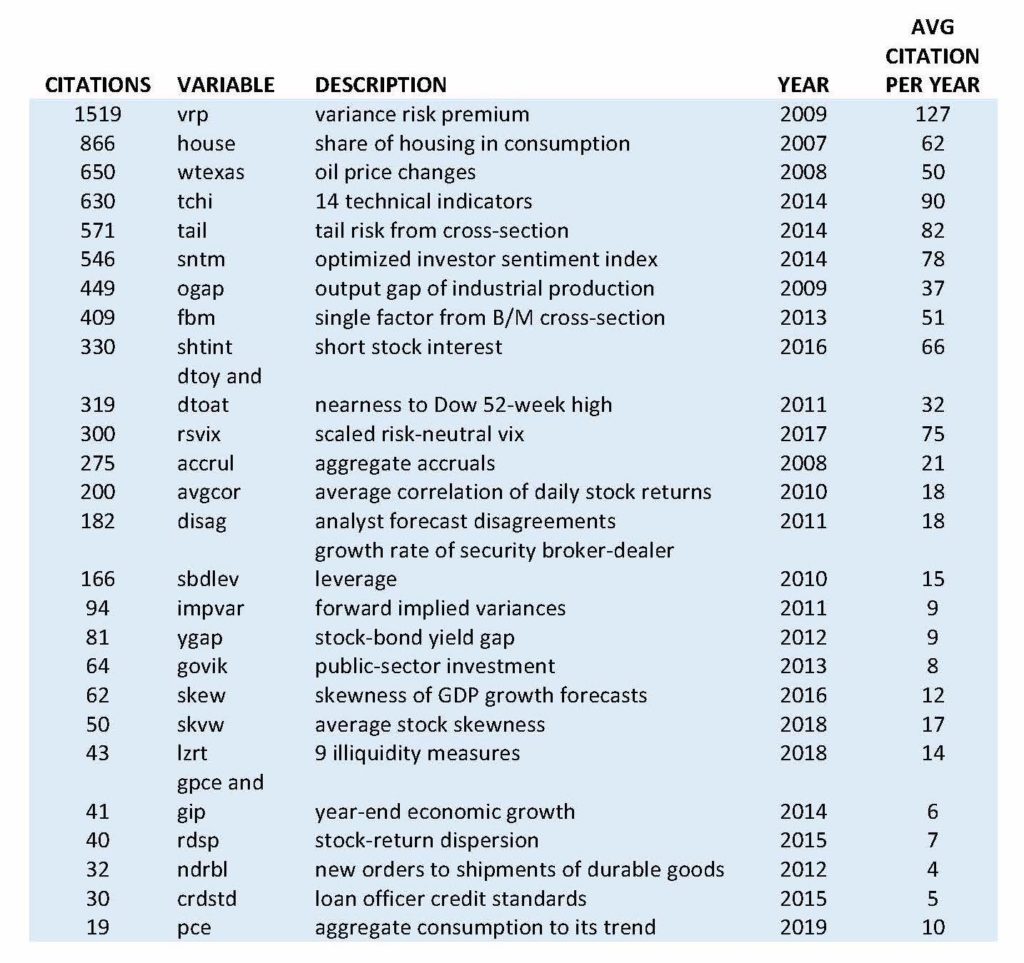

Looking at the table below, the variables that were found to remain statistically significant on the extended dataset were those with the fewest citations and likely less well known among market participants.

The Five Best Variables on a Statistical Basis

Fourth-Quarter Growth Rate in Personal Consumption Expenditures ( gpce) : This macroeconomic variable from researchers Møller and Rangvid posits that high personal consumption growth rates at the end of the year predicts poor stock-market gains in the following year. The researchers found it to be the best, and most consistent, variable in the investment strategies. It outperformed a buy-and-hold approach with three of the four strategies tested. However, the outperformance was only marginal.

Aggregate Accruals (accru) : This is a sentiment-based variable introduced by Hirshleifer, Hou and Teoh and uses aggressive corporate accounting to predict future stock returns — more aggressive accruals lead to lower future returns. The variable also marginally beat buy-and-hold returns in three out of four approaches. Most of its performance came from its prediction of the post-tech market crash in 2000-2002.

Credit Standards (crdstd) : This is another macroeconomic variable and was introduced by Chava, Gallmeyer and Park. It finds that optimistic (loose) credit standards predict poor market returns and comes from survey data by the Fed. This variable did well in the researchers’ investment strategies and had good performance on test sample data, but statistical measures of the variable on the training sample data were not as convincing and much of its performance comes from the first four years in that sample.

The Investment Capital Ratio (i/k) : This a financial ratio introduced by Cochrane all the way back in 1991 and was also included in the 2008 paper from Goyal and Welch. It posits that high capital investment in the current quarter predicts poor stock-market returns in the next quarter. While it was a poor predictor from 1975 to 1998, it has since improved performance yet was not able to outperform a buy-and-hold strategy in three of four of the researchers’ timing strategies.

Treasury-bill Rates (tbl ): This is another variable examined in the 2008 paper. It does well statistically but had poor performance in the investment strategies.

Oft-Cited Papers With Poor-Performing Variables

Variance Risk Premium (vrp) : This variable was introduced by Bollerslev, Tauchen and Zhou and has the most citations. The variable had poor statistical performance, as well as poor performance in all four of the investment strategies.

Share of Housing Consumption (house) : This macroeconomic variable introduced by Piazzesi, Schneider and Tuzel has the second-highest number of citations. It uses housing share of consumer spending to forecast the excess return of stocks. (The higher the spending on housing, the higher the excess returns in the stock market.) The variable had poor statistical performance on the extended dataset and poor performance in the investment strategies.

The Price of West-Texas Intermediate Crude Oil (wtexas) : This was the only commodity-based variable and was introduced by Driesprong, Jacobsen and Maat. The paper posits that changes in the price of oil predict stock returns — higher oil prices lead to lower stock returns — with lags. The variable had poor statistical performance for the extended dataset and inconsistent performance in the investment strategies.

The First Principal Component of 14 Technical Indicators ( tchi ): This variable was introduced by Neely, Rapach, Tu and Zhou and is a linear combination of technical indicators including moving price averages, momentum and volume. It only had marginal statistical performance and inconsistent performance in the trading strategies.

Featured Faculty

Distinguished Professor of Finance; J. Fred Weston Chair in Finance

About the Research

Goyal, A., Welch, I., & Zafirov, A. (2021). A Comprehensive Look at the Empirical Performance of Equity Premium Prediction II . http://dx.doi.org/10.2139/ssrn.3929119

Suggested Articles

New Study Disavows Marshmallow Test’s Predictive Powers

Replicating a Successful Nudge in Health Care: Advice for Skeptics

Calculating a Value for the Government Support Banks Enjoy

Related articles.

Political Football: Inclusion of ESG Funds in 401(k)s

In nation accustomed to litigation, availability of funds has varied by U.S. Circuit Court boundary

Why Do Banks With Little Skin in the Game Still Monitor Borrowers?

Tax policy change triggers an incentive for lenders to be more aggressive

In China, Big Investors Have Brilliant Timing ― Or Do They Know Someone?

A scan of a million brokerage accounts finds the wealthy trade ahead of market-moving news

Low-Quality Earnings: The Uncoupling of Stock Price from Fundamentals

Studying Chinese A and B shares reveals investor uncertainty

Research Topics & Ideas: Finance

120+ Finance Research Topic Ideas To Fast-Track Your Project

If you’re just starting out exploring potential research topics for your finance-related dissertation, thesis or research project, you’ve come to the right place. In this post, we’ll help kickstart your research topic ideation process by providing a hearty list of finance-centric research topics and ideas.

PS – This is just the start…

We know it’s exciting to run through a list of research topics, but please keep in mind that this list is just a starting point . To develop a suitable education-related research topic, you’ll need to identify a clear and convincing research gap , and a viable plan of action to fill that gap.

If this sounds foreign to you, check out our free research topic webinar that explores how to find and refine a high-quality research topic, from scratch. Alternatively, if you’d like hands-on help, consider our 1-on-1 coaching service .

Overview: Finance Research Topics

- Corporate finance topics

- Investment banking topics

- Private equity & VC

- Asset management

- Hedge funds

- Financial planning & advisory

- Quantitative finance

- Treasury management

- Financial technology (FinTech)

- Commercial banking

- International finance

Corporate Finance

These research topic ideas explore a breadth of issues ranging from the examination of capital structure to the exploration of financial strategies in mergers and acquisitions.

- Evaluating the impact of capital structure on firm performance across different industries

- Assessing the effectiveness of financial management practices in emerging markets

- A comparative analysis of the cost of capital and financial structure in multinational corporations across different regulatory environments

- Examining how integrating sustainability and CSR initiatives affect a corporation’s financial performance and brand reputation

- Analysing how rigorous financial analysis informs strategic decisions and contributes to corporate growth

- Examining the relationship between corporate governance structures and financial performance

- A comparative analysis of financing strategies among mergers and acquisitions

- Evaluating the importance of financial transparency and its impact on investor relations and trust

- Investigating the role of financial flexibility in strategic investment decisions during economic downturns

- Investigating how different dividend policies affect shareholder value and the firm’s financial performance

Investment Banking

The list below presents a series of research topics exploring the multifaceted dimensions of investment banking, with a particular focus on its evolution following the 2008 financial crisis.

- Analysing the evolution and impact of regulatory frameworks in investment banking post-2008 financial crisis

- Investigating the challenges and opportunities associated with cross-border M&As facilitated by investment banks.

- Evaluating the role of investment banks in facilitating mergers and acquisitions in emerging markets

- Analysing the transformation brought about by digital technologies in the delivery of investment banking services and its effects on efficiency and client satisfaction.

- Evaluating the role of investment banks in promoting sustainable finance and the integration of Environmental, Social, and Governance (ESG) criteria in investment decisions.

- Assessing the impact of technology on the efficiency and effectiveness of investment banking services

- Examining the effectiveness of investment banks in pricing and marketing IPOs, and the subsequent performance of these IPOs in the stock market.

- A comparative analysis of different risk management strategies employed by investment banks

- Examining the relationship between investment banking fees and corporate performance

- A comparative analysis of competitive strategies employed by leading investment banks and their impact on market share and profitability

Private Equity & Venture Capital (VC)

These research topic ideas are centred on venture capital and private equity investments, with a focus on their impact on technological startups, emerging technologies, and broader economic ecosystems.

- Investigating the determinants of successful venture capital investments in tech startups

- Analysing the trends and outcomes of venture capital funding in emerging technologies such as artificial intelligence, blockchain, or clean energy

- Assessing the performance and return on investment of different exit strategies employed by venture capital firms

- Assessing the impact of private equity investments on the financial performance of SMEs

- Analysing the role of venture capital in fostering innovation and entrepreneurship

- Evaluating the exit strategies of private equity firms: A comparative analysis

- Exploring the ethical considerations in private equity and venture capital financing

- Investigating how private equity ownership influences operational efficiency and overall business performance

- Evaluating the effectiveness of corporate governance structures in companies backed by private equity investments

- Examining how the regulatory environment in different regions affects the operations, investments and performance of private equity and venture capital firms

Asset Management

This list includes a range of research topic ideas focused on asset management, probing into the effectiveness of various strategies, the integration of technology, and the alignment with ethical principles among other key dimensions.

- Analysing the effectiveness of different asset allocation strategies in diverse economic environments

- Analysing the methodologies and effectiveness of performance attribution in asset management firms

- Assessing the impact of environmental, social, and governance (ESG) criteria on fund performance

- Examining the role of robo-advisors in modern asset management

- Evaluating how advancements in technology are reshaping portfolio management strategies within asset management firms

- Evaluating the performance persistence of mutual funds and hedge funds

- Investigating the long-term performance of portfolios managed with ethical or socially responsible investing principles

- Investigating the behavioural biases in individual and institutional investment decisions

- Examining the asset allocation strategies employed by pension funds and their impact on long-term fund performance

- Assessing the operational efficiency of asset management firms and its correlation with fund performance

Hedge Funds

Here we explore research topics related to hedge fund operations and strategies, including their implications on corporate governance, financial market stability, and regulatory compliance among other critical facets.

- Assessing the impact of hedge fund activism on corporate governance and financial performance

- Analysing the effectiveness and implications of market-neutral strategies employed by hedge funds

- Investigating how different fee structures impact the performance and investor attraction to hedge funds

- Evaluating the contribution of hedge funds to financial market liquidity and the implications for market stability

- Analysing the risk-return profile of hedge fund strategies during financial crises

- Evaluating the influence of regulatory changes on hedge fund operations and performance

- Examining the level of transparency and disclosure practices in the hedge fund industry and its impact on investor trust and regulatory compliance

- Assessing the contribution of hedge funds to systemic risk in financial markets, and the effectiveness of regulatory measures in mitigating such risks

- Examining the role of hedge funds in financial market stability

- Investigating the determinants of hedge fund success: A comparative analysis

Financial Planning and Advisory

This list explores various research topic ideas related to financial planning, focusing on the effects of financial literacy, the adoption of digital tools, taxation policies, and the role of financial advisors.

- Evaluating the impact of financial literacy on individual financial planning effectiveness

- Analysing how different taxation policies influence financial planning strategies among individuals and businesses

- Evaluating the effectiveness and user adoption of digital tools in modern financial planning practices

- Investigating the adequacy of long-term financial planning strategies in ensuring retirement security

- Assessing the role of financial education in shaping financial planning behaviour among different demographic groups

- Examining the impact of psychological biases on financial planning and decision-making, and strategies to mitigate these biases

- Assessing the behavioural factors influencing financial planning decisions

- Examining the role of financial advisors in managing retirement savings

- A comparative analysis of traditional versus robo-advisory in financial planning

- Investigating the ethics of financial advisory practices

The following list delves into research topics within the insurance sector, touching on the technological transformations, regulatory shifts, and evolving consumer behaviours among other pivotal aspects.

- Analysing the impact of technology adoption on insurance pricing and risk management

- Analysing the influence of Insurtech innovations on the competitive dynamics and consumer choices in insurance markets

- Investigating the factors affecting consumer behaviour in insurance product selection and the role of digital channels in influencing decisions

- Assessing the effect of regulatory changes on insurance product offerings

- Examining the determinants of insurance penetration in emerging markets

- Evaluating the operational efficiency of claims management processes in insurance companies and its impact on customer satisfaction

- Examining the evolution and effectiveness of risk assessment models used in insurance underwriting and their impact on pricing and coverage

- Evaluating the role of insurance in financial stability and economic development

- Investigating the impact of climate change on insurance models and products

- Exploring the challenges and opportunities in underwriting cyber insurance in the face of evolving cyber threats and regulations

Quantitative Finance

These topic ideas span the development of asset pricing models, evaluation of machine learning algorithms, and the exploration of ethical implications among other pivotal areas.

- Developing and testing new quantitative models for asset pricing

- Analysing the effectiveness and limitations of machine learning algorithms in predicting financial market movements

- Assessing the effectiveness of various risk management techniques in quantitative finance

- Evaluating the advancements in portfolio optimisation techniques and their impact on risk-adjusted returns

- Evaluating the impact of high-frequency trading on market efficiency and stability

- Investigating the influence of algorithmic trading strategies on market efficiency and liquidity

- Examining the risk parity approach in asset allocation and its effectiveness in different market conditions

- Examining the application of machine learning and artificial intelligence in quantitative financial analysis

- Investigating the ethical implications of quantitative financial innovations

- Assessing the profitability and market impact of statistical arbitrage strategies considering different market microstructures

Treasury Management

The following topic ideas explore treasury management, focusing on modernisation through technological advancements, the impact on firm liquidity, and the intertwined relationship with corporate governance among other crucial areas.

- Analysing the impact of treasury management practices on firm liquidity and profitability

- Analysing the role of automation in enhancing operational efficiency and strategic decision-making in treasury management

- Evaluating the effectiveness of various cash management strategies in multinational corporations

- Investigating the potential of blockchain technology in streamlining treasury operations and enhancing transparency

- Examining the role of treasury management in mitigating financial risks

- Evaluating the accuracy and effectiveness of various cash flow forecasting techniques employed in treasury management

- Assessing the impact of technological advancements on treasury management operations

- Examining the effectiveness of different foreign exchange risk management strategies employed by treasury managers in multinational corporations

- Assessing the impact of regulatory compliance requirements on the operational and strategic aspects of treasury management

- Investigating the relationship between treasury management and corporate governance

Financial Technology (FinTech)

The following research topic ideas explore the transformative potential of blockchain, the rise of open banking, and the burgeoning landscape of peer-to-peer lending among other focal areas.

- Evaluating the impact of blockchain technology on financial services

- Investigating the implications of open banking on consumer data privacy and financial services competition

- Assessing the role of FinTech in financial inclusion in emerging markets

- Analysing the role of peer-to-peer lending platforms in promoting financial inclusion and their impact on traditional banking systems

- Examining the cybersecurity challenges faced by FinTech firms and the regulatory measures to ensure data protection and financial stability

- Examining the regulatory challenges and opportunities in the FinTech ecosystem

- Assessing the impact of artificial intelligence on the delivery of financial services, customer experience, and operational efficiency within FinTech firms

- Analysing the adoption and impact of cryptocurrencies on traditional financial systems

- Investigating the determinants of success for FinTech startups

Commercial Banking

These topic ideas span commercial banking, encompassing digital transformation, support for small and medium-sized enterprises (SMEs), and the evolving regulatory and competitive landscape among other key themes.

- Assessing the impact of digital transformation on commercial banking services and competitiveness

- Analysing the impact of digital transformation on customer experience and operational efficiency in commercial banking

- Evaluating the role of commercial banks in supporting small and medium-sized enterprises (SMEs)

- Investigating the effectiveness of credit risk management practices and their impact on bank profitability and financial stability

- Examining the relationship between commercial banking practices and financial stability

- Evaluating the implications of open banking frameworks on the competitive landscape and service innovation in commercial banking

- Assessing how regulatory changes affect lending practices and risk appetite of commercial banks

- Examining how commercial banks are adapting their strategies in response to competition from FinTech firms and changing consumer preferences

- Analysing the impact of regulatory compliance on commercial banking operations

- Investigating the determinants of customer satisfaction and loyalty in commercial banking

International Finance

The folowing research topic ideas are centred around international finance and global economic dynamics, delving into aspects like exchange rate fluctuations, international financial regulations, and the role of international financial institutions among other pivotal areas.

- Analysing the determinants of exchange rate fluctuations and their impact on international trade

- Analysing the influence of global trade agreements on international financial flows and foreign direct investments

- Evaluating the effectiveness of international portfolio diversification strategies in mitigating risks and enhancing returns

- Evaluating the role of international financial institutions in global financial stability

- Investigating the role and implications of offshore financial centres on international financial stability and regulatory harmonisation

- Examining the impact of global financial crises on emerging market economies

- Examining the challenges and regulatory frameworks associated with cross-border banking operations

- Assessing the effectiveness of international financial regulations

- Investigating the challenges and opportunities of cross-border mergers and acquisitions

Choosing A Research Topic

These finance-related research topic ideas are starting points to guide your thinking. They are intentionally very broad and open-ended. By engaging with the currently literature in your field of interest, you’ll be able to narrow down your focus to a specific research gap .

When choosing a topic , you’ll need to take into account its originality, relevance, feasibility, and the resources you have at your disposal. Make sure to align your interest and expertise in the subject with your university program’s specific requirements. Always consult your academic advisor to ensure that your chosen topic not only meets the academic criteria but also provides a valuable contribution to the field.

If you need a helping hand, feel free to check out our private coaching service here.

You Might Also Like:

thank you for suggest those topic, I want to ask you about the subjects related to the fintech, can i measure it and how?

Submit a Comment Cancel reply

Your email address will not be published. Required fields are marked *

Save my name, email, and website in this browser for the next time I comment.

- Print Friendly

A systematic review of fundamental and technical analysis of stock market predictions

- Published: 20 August 2019

- Volume 53 , pages 3007–3057, ( 2020 )

Cite this article

- Isaac Kofi Nti ORCID: orcid.org/0000-0001-9257-4295 1 , 2 ,

- Adebayo Felix Adekoya ORCID: orcid.org/0000-0002-5029-2393 2 &

- Benjamin Asubam Weyori ORCID: orcid.org/0000-0001-5422-4251 2

16k Accesses

193 Citations

Explore all metrics

The stock market is a key pivot in every growing and thriving economy, and every investment in the market is aimed at maximising profit and minimising associated risk. As a result, numerous studies have been conducted on the stock-market prediction using technical or fundamental analysis through various soft-computing techniques and algorithms. This study attempted to undertake a systematic and critical review of about one hundred and twenty-two (122) pertinent research works reported in academic journals over 11 years (2007–2018) in the area of stock market prediction using machine learning. The various techniques identified from these reports were clustered into three categories, namely technical, fundamental, and combined analyses. The grouping was done based on the following criteria: the nature of a dataset and the number of data sources used, the data timeframe, the machine learning algorithms used, machine learning task, used accuracy and error metrics and software packages used for modelling. The results revealed that 66% of documents reviewed were based on technical analysis; whiles 23% and 11% were based on fundamental analysis and combined analyses, respectively. Concerning the number of data source, 89.34% of documents reviewed, used single sources; whiles 8.2% and 2.46% used two and three sources respectively. Support vector machine and artificial neural network were found to be the most used machine learning algorithms for stock market prediction.

This is a preview of subscription content, log in via an institution to check access.

Access this article

Price includes VAT (Russian Federation)

Instant access to the full article PDF.

Rent this article via DeepDyve

Institutional subscriptions

Similar content being viewed by others

Stock Market Prediction Using Machine Learning Techniques: A Comparative Study

A Study on Stock Market Forecasting and Machine Learning Models: 1970–2020

Machine Learning Techniques for Stock Market Predictions: A Case of Mexican Stocks

Abhishek K et al (2012) A stock market prediction model using artificial neural network. In: Third international conference on computing communication & networking technologies (ICCCNT), pp 1–5. https://doi.org/10.1109/icccnt.2012.6396089

Adam AM, Tweneboah G (2008) Macroeconomic factors and stock market movement: evidence from Ghana. University of Leicester, Leicester. https://doi.org/10.2139/ssrn.1289842

Book Google Scholar

Adebayo AD, Adekoya AF, Rahman TM (2017) Predicting stock trends using Tsk-fuzzy rule based system. JENRM 4(7):48–55

Google Scholar

Adebiyi AA et al (2012) Stock price prediction using neural network with hybridized market indicators. J Emerg Trends Comput Inf Sci 3(1):1–9

Adebiyi AA, Adewumi AO, Ayo CK (2014a) Comparison of ARIMA and artificial neural networks models for stock price prediction. J Appl Math 2014:9–11. https://doi.org/10.1155/2014/614342

Article MathSciNet Google Scholar

Adebiyi AA, Adewumi AO, Ayo CK (2014) Stock price prediction using the ARIMA model. In: Proceedings—UKSim-AMSS 16th international conference on computer modelling and simulation, UKSim 2014, pp 106–112. https://doi.org/10.1109/uksim.2014.67

Adusei M (2014) The inflation-stock market returns nexus: evidence from the Ghana stock exchange. J Econ Int Finance 6(2):38–46. https://doi.org/10.5958/2321-5763.2016.00010.X

Article Google Scholar

Agarwal P et al (2017) Stock market price trend forecasting using machine learning. Int J Res Appl Sci Eng Technol: IJRASET 5(IV):1673–1676

Agrawal S, Jindal M, Pillai GN (2010) Momentum analysis based stock market prediction using adaptive neuro-fuzzy inference system (ANFIS). In: International multiconference of engineers and computer scientists (IMECS). Hong Kong

Agrawal JG, Chourasia VS, Mittra AK (2013) State-of-the-art in stock prediction techniques. Int J Adv Res Electr Electron Instrum Eng 2(4):1360–1366

Ahmadi E et al (2018) New efficient hybrid candlestick technical analysis model for stock market timing on the basis of the support vector machine and heuristic algorithms of imperialist competition and genetic. Expert Syst Appl 94(April):21–31. https://doi.org/10.1016/j.eswa.2017.10.023

Akinwale Adio T, Arogundade OT, Adekoya AF (2009) Translated Nigeria stock market prices using artificial neural network for effective prediction. J Theor Appl Inf Technol. pp 36–43. http://jatit.org/volumes/research-papers/Vol9No1/6Vol9No1.pdf

Almeida L, Lorena A, De Oliveira I (2010) Expert systems with applications a method for automatic stock trading combining technical analysis and nearest neighbor classification. Expert Syst Appl 37(10):6885–6890. https://doi.org/10.1016/j.eswa.2010.03.033

Anbalagan T, Maheswari SU (2014) Classification and prediction of stock market index based on fuzzy metagraph. Procedia Comput Sci 47(C):214–221. https://doi.org/10.1016/j.procs.2015.03.200

Ansari T et al (2010) Sequential combination of statistics, econometrics and adaptive neural-fuzzy interface for stock market prediction. Expert Syst Appl 37(7):5116–5125. https://doi.org/10.1016/j.eswa.2009.12.083

Anthony J, Maurice L, Eshwar S (2011) Predictive ability of the interest rate spread using neural networks. Procedia Comput Sci 6:207–212. https://doi.org/10.1016/j.procs.2011.08.039

Argiddi VR, Apte SS (2012) Future trend prediction of Indian IT stock market using association rule mining of transaction data. Int J Comput Appl 39(10):30–34. https://doi.org/10.5120/4858-7132

Asadi S et al (2012) Hybridization of evolutionary Levenberg–Marquardt neural networks and data pre-processing for stock market prediction. Knowl Based Syst 35:245–258. https://doi.org/10.1016/j.knosys.2012.05.003

Atsalakis GS, Dimitrakakis EM, Zopounidis CD (2011) Elliott wave theory and neuro-fuzzy systems, in stock market prediction: the WASP system. Expert Syst Appl 38(8):9196–9206. https://doi.org/10.1016/j.eswa.2011.01.068

Ayub A (2018) Volatility transmission from oil prices to agriculture commodity and stock market in Pakistan. Capital University of Science and Technology, Islamabad

Babu MS, Geethanjali N, Satyanarayana PB (2012) Clustering approach to stock market prediction. Int J Adv Netw Appl 03(04):1281–1291

Baker M, Wurgler J (2007) Investor sentiment in the stock market. http://www.nber.org/papers/w13189

Ballings M et al (2015) Evaluating multiple classifiers for stock price direction prediction. Expert Syst Appl 42(20):7046–7056. https://doi.org/10.1016/j.eswa.2015.05.013

Bhagwant C et al (2014) Stock market prediction using artificial neural networks. Int J Comput Sci Inf Technol 5(1):904–907. https://doi.org/10.4028/www.scientific.net/AEF.6-7.1055

Bisoi R, Dash PK (2014) A hybrid evolutionary dynamic neural network for stock market trend analysis and prediction using unscented Kalman filter. Appl Soft Comput J 19:41–56. https://doi.org/10.1016/j.asoc.2014.01.039

Boachie MK et al (2016) Interest rate, liquidity and stock market performance in Ghana. Int J Account Econ Stud 4(1):46. https://doi.org/10.14419/ijaes.v4i1.5990

Bollen J, Mao H, Zeng X-J (2011) Twitter mood predicts the stock market. J Comput Sci 2(1):1–8. https://doi.org/10.1016/j.jocs.2010.12.007

Bordino I et al (2012) Web search queries can predict stock market volumes. PLoS ONE. https://doi.org/10.1371/journal.pone.0040014

Boyacioglu MA, Avci D (2010) Adaptive network-based fuzzy inference system (ANFIS) for the prediction of stock market return: the case of the Istanbul stock exchange. Expert Syst Appl 37(12):7908–7912. https://doi.org/10.1016/j.eswa.2010.04.045

Chakravarty S, Dash PK (2012) A PSO based integrated functional link net and interval type-2 fuzzy logic system for predicting stock market indices. Appl Soft Comput J 12(2):931–941. https://doi.org/10.1016/j.asoc.2011.09.013

Chan K et al (2017) What do stock price levels tell us about the firms? J Corp Finance 46:34–50. https://doi.org/10.1016/j.jcorpfin.2017.06.013

Chang SV et al (2013) A review of stock market prediction with artificial neural network (ANN). In: 2013 IEEE international conference on control system, computing and engineering, pp 477–482. https://doi.org/10.1109/iccsce.2013.6720012

Checkley MS, Higón DA, Alles H (2017) The hasty wisdom of the mob: how market sentiment predicts stock market behavior. Expert Syst Appl 77:256–263. https://doi.org/10.1016/j.eswa.2017.01.029

Chen C et al (2014) Exploiting social media for stock market prediction with factorization machine. In: 2014 IEEE/WIC/ACM international joint conference on web intelligence and intelligent agent technology—workshops, WI-IAT 2014, pp 49–56. https://doi.org/10.1109/wi-iat.2014.91

Chen Y, Hao Y (2017) A feature weighted support vector machine and K-nearest neighbor algorithm for stock market indices prediction. Expert Syst Appl 80:340–355. https://doi.org/10.1016/j.eswa.2017.02.044

Chen R, Lazer M (2013) Sentiment analysis of Twitter feeds for the prediction of stock market movement. Stanf Educ 25:1–5. https://doi.org/10.1016/j.ufug.2017.05.003

Chong E, Han C, Park FC (2017) Deep learning networks for stock market analysis and prediction: methodology, data representations, and case studies. Expert Syst Appl 83:187–205. https://doi.org/10.1016/j.eswa.2017.04.030

Coyne S, Madiraju P, Coelho J (2017) Forecasting stock prices using social media analysis. In: IEEE 15th international conference on big data intelligence and computing and cyber science and technology congress. IEEE Computer Society, pp 1031–1038. https://doi.org/10.1109/dasc-picom-datacom-cyberscitec.2017.169

Dase RK, Pawar DD (2010) Application of artificial neural network for stock market predictions: a review of literature. Int J Mach Intell 2(2):14–17

Dash R, Dash PK (2016) Efficient stock price prediction using a self evolving recurrent neuro-fuzzy inference system optimized through a modified technique. Expert Syst Appl 52:75–90. https://doi.org/10.1016/j.eswa.2016.01.016

de Araújo RA (2010) A quantum-inspired evolutionary hybrid intelligent approach for stock market prediction. Int J Intell Comput Cybern 3(1):24–54

Article MathSciNet MATH Google Scholar

de Araújo RA, Ferreira TAE (2013) A morphological-rank-linear evolutionary method for stock market prediction. Inf Sci 237:3–17. https://doi.org/10.1016/j.ins.2009.07.007

de Oliveira FA, Nobre CN, Zárate LE (2013) Applying artificial neural networks to prediction of stock price and improvement of the directional prediction index—case study of PETR4, Petrobras, Brazil. Expert Syst Appl 40(18):7596–7606. https://doi.org/10.1016/j.eswa.2013.06.071

Demyanyk Y, Hasan I (2010) Financial crises and bank failures: a review of prediction methods. Omega. https://doi.org/10.1016/j.omega.2009.09.007

Ding X et al (2014) Using structured events to predict stock price movement: an empirical investigation. In: The 2014 conference on empirical methods in natural language processing (EMNLP). Association for Computational Linguistics, Doha, pp 1415–1425. https://doi.org/10.3115/v1/d14-1148

Dondio P (2013) Stock market prediction without sentiment analysis: using a web-traffic based classifier and user-level analysis. In: Proceedings of the annual hawaii international conference on system sciences, pp 3137–3146. https://doi.org/10.1109/hicss.2013.498

Dosdoğru AT et al (2018) Assessment of hybrid artificial neural networks and metaheuristics for stock market forecasting. Ç. Ü. Sosyal Bilimler Enstitüsü Dergisi 24(1):63–78

Dunne M (2015) Stock market prediction. University College Cork, Cork

Dutta A, Bandopadhyay G, Sengupta S (2012) Prediction of stock performance in the indian stock market using logistic regression. Int J Bus Inf 7(1):105–136

Enke D, Mehdiyev N (2013) Stock market prediction using a combination of stepwise regression analysis, differential evolution-based fuzzy clustering, and a fuzzy inference neural network. Intell Autom Soft Comput 19(4):636–648. https://doi.org/10.1080/10798587.2013.839287

Enke D, Grauer M, Mehdiyev N (2011) Stock market prediction with multiple regression, fuzzy type-2 clustering and neural networks. Procedia Comput Sci 6:201–206. https://doi.org/10.1016/j.procs.2011.08.038

Ertuna L (2016) Stock market prediction using neural network time series forecasting (May). https://doi.org/10.13140/rg.2.1.1954.1368

Esfahanipour A, Aghamiri W (2010) Adapted neuro-fuzzy inference system on indirect approach TSK fuzzy rule base for stock market analysis. Expert Syst Appl 37(7):4742–4748. https://doi.org/10.1016/j.eswa.2009.11.020

Fajiang L, Wang J (2012) Fluctuation prediction of stock market index by Legendre neural network with random time strength function. Neurocomputing 83:12–21. https://doi.org/10.1016/j.neucom.2011.09.033

Fama EF (1965) Random walks in stock market prices. Financ Anal J 21:55–59

Fama EF (1970) Efficient capital markets: a review of theory and empirical work. J Finance 25:383–417

Fang Y et al (2014) Improving the genetic-algorithm-optimized wavelet neural network for stock market prediction. In: International joint conference on neural networks. IEEE, Beijing, pp 3038–3042. https://doi.org/10.1109/ijcnn.2014.6889969

Gaius KD (2015) Assessing the performance of active and passive trading on the Ghana stock exchange. University of Ghana, Accra

García F, Guijarro F, Oliver J (2018) Hybrid fuzzy neural network to predict price direction in the German DAX-30 index. Technol Econ Dev Econ 24(6):2161–2178

Geva T, Zahavi J (2014) Empirical evaluation of an automated intraday stock recommendation system incorporating both market data and textual news. Decis Support Syst 57(1):212–223. https://doi.org/10.1016/j.dss.2013.09.013

Ghaznavi A, Aliyari M, Mohammadi MR (2016) Predicting stock price changes of tehran artmis company using radial basis function neural networks. Int Res J Appl Basic Sci 10(8):972–978

Göçken M et al (2016) Integrating metaheuristics and artificial neural networks for improved stock price prediction. Expert Syst Appl 44:320–331. https://doi.org/10.1016/j.eswa.2015.09.029

Goel SK, Poovathingal B, Kumari N (2016) Applications of neural networks to stock market prediction. Int Res J Eng Technol: IRJET 03(05):2192–2197

Gupta A, Sharma SD (2014) Clustering-classification based prediction of stock market future prediction. Int J Comput Sci Inf Technol 5(3):2806–2809

Guresen E, Kayakutlu G, Daim TU (2011) Using artificial neural network models in stock market index prediction. Expert Syst Appl 38(8):10389–10397. https://doi.org/10.1016/j.eswa.2011.02.068

Gyan MK (2015) Factors influencing the patronage of stocks, Knu. Kwame Nkrumah University of Science & Technology (KNUST), Kumasi

Hadavandi E, Shavandi H, Ghanbari A (2010) Knowledge-based systems integration of genetic fuzzy systems and artificial neural networks for stock price forecasting. Knowl Based Syst 23(8):800–808. https://doi.org/10.1016/j.knosys.2010.05.004

Hagenau M, Liebmann M, Neumann D (2013) Automated news reading: stock price prediction based on financial news using context-capturing features. Decis Support Syst 55(3):685–697. https://doi.org/10.1016/j.dss.2013.02.006

Hassan MR et al (2013) A HMM-based adaptive fuzzy inference system for stock market forecasting. Neurocomputing 104:10–25. https://doi.org/10.1016/j.neucom.2012.09.017

Hegazy O, Soliman OS, Salam MA (2013) A machine learning model for stock market prediction. Int J Comput Sci Telecommun 4(12):17–23

Henriksson A et al (2016) Ensembles of randomized trees using diverse distributed representation of clinical events. BMC Med Inf Decis Mak 16(2):69

Ibrahim SO (2017) Forecasting the volatilities of the Nigeria stock market prices. CBN J Appl Stat 8(2):23–45

MathSciNet Google Scholar

Javed K, Gouriveau R, Zerhouni N (2014) SW-ELM: a summation wavelet extreme learning machine algorithm with a priori parameter initialization. Neurocomputing 123:299–307. https://doi.org/10.1016/j.neucom.2013.07.021

Jianfeng S et al (2014) Exploiting social relations and sentiment for stock prediction. In: Conference on empirical methods in natural language processing (EMNLP). Association for Computational Linguistics, Doha, pp 1139–1145. https://doi.org/10.1080/00378941.1956.10837773

Ju-Jie W et al (2012) Stock index forecasting based on a hybrid model. Omega 40(6):758–766. https://doi.org/10.1016/j.omega.2011.07.008

Kannan KS et al (2010) Financial stock market forecast using data mining techniques. In: International multiconference of engineers and computer scientists (IMECS)

Kara Y, Acar Boyacioglu M, Baykan ÖK (2011) Predicting direction of stock price index movement using artificial neural networks and support vector machines: the sample of the Istanbul stock exchange. Expert Syst Appl 38(5):5311–5319. https://doi.org/10.1016/j.eswa.2010.10.027

Kazem A et al (2013) Support vector regression with chaos-based firefly algorithm for stock market price forecasting. Appl Soft Comput J 13(2):947–958. https://doi.org/10.1016/j.asoc.2012.09.024

Kearney C, Liu S (2014) Textual sentiment in finance: a survey of methods and models. Int Rev Financ Anal 33(Cc):171–185. https://doi.org/10.1016/j.irfa.2014.02.006

Khan HZ, Alin ST, Hussain A (2011) Price prediction of share market using artificial neural network “ANN”. Int J Comput Appl 22(2):42–47. https://doi.org/10.5120/2552-3497

Kraus M, Feuerriegel S (2017) Decision support from financial disclosures with deep neural networks and transfer learning. Decis Support Syst 104:38–48. https://doi.org/10.1016/j.dss.2017.10.001

Krollner B, Vanstone B, Finnie G (2010a) Financial time series forecasting with machine learning techniques: a survey. In: European symposium on artificial neural networks: computational and machine learning. Bond University, Bruges, pp 25–30

Krollner B, Vanstone B, Finnie G (2010b) Financial time series forecasting with machine learning techniques: a survey. http://epublications.bond.edu.au/infotech_pubs/110

Kumar DA, Murugan S (2013) Performance analysis of Indian stock market index using neural network time series model. In: Proceedings of the 2013 international conference on pattern recognition, informatics and mobile engineering, PRIME 2013, pp 72–78. https://doi.org/10.1109/icprime.2013.6496450

Kumar M, Thenmozhi M (2006) Forecasting stock index movement: a comparison of support vector machines and random forest. In Indian Institute of capital markets 9th capital markets conference paper.

Kumar D, Meghwani SS, Thakur M (2016) Proximal support vector machine based hybrid prediction models for trend forecasting in financial markets. J Comput Sci 17:1–13. https://doi.org/10.1016/j.jocs.2016.07.006

Kuwornu JKM, Victor O-N (2011) Macroeconomic variables and stock market returns: full information maximum likelihood estimation. Res J Finance Account 2(4):49–64

Kwofie C, Ansah RK (2018) A study of the effect of inflation and exchange rate on stock market returns in Ghana. Int J Math Math Sci. https://doi.org/10.1155/2018/7016792

Laboissiere LA, Fernandes RAS, Lage GG (2015) Maximum and minimum stock price forecasting of Brazilian power distribution companies based on artificial neural networks. Appl Soft Comput J 35:66–74. https://doi.org/10.1016/j.asoc.2015.06.005

Lahmiri S (2011) A Comparison of PNN and SVM for stock market trend prediction using economic and technical information. Int J Comput Appl 29(3):975–8887

Li Q et al (2015) Tensor-based learning for predicting stock movements. In: Twenty-ninth AAAI conference on artificial intelligence-2015, pp 1784–1790. https://doi.org/10.1073/pnas.0601853103

Li Q, Wang T, Gong Q et al (2014a) Media-aware quantitative trading based on public Web information. Decis Support Syst 61(1):93–105. https://doi.org/10.1016/j.dss.2014.01.013

Li Q, Wang T, Li P et al (2014b) The effect of news and public mood on stock movements. Inf Sci 278:826–840. https://doi.org/10.1016/j.ins.2014.03.096

Li X, Huang X et al (2014c) Enhancing quantitative intra-day stock return prediction by integrating both market news and stock prices information. Neurocomputing 142:228–238. https://doi.org/10.1016/j.neucom.2014.04.043

Li X, Xie H et al (2014d) News impact on stock price return via sentiment analysis. Knowl-Based Syst 69(1):14–23. https://doi.org/10.1016/j.knosys.2014.04.022

Lin Z (2018) Modelling and forecasting the stock market volatility of SSE composite index using GARCH models. Future Gener Comput Syst 79:960–972. https://doi.org/10.1016/j.future.2017.08.033

Lin Y, Guo H, Hu J (2013) An SVM-based approach for stock market trend prediction. In: Proceedings of the international joint conference on neural networks. https://doi.org/10.1109/ijcnn.2013.6706743

Liu L et al (2015) A social-media-based approach to predicting stock comovement. Expert Syst Appl 42(8):3893–3901. https://doi.org/10.1016/j.eswa.2014.12.049

Luo F, Wu J, Yan K (2010) A novel nonlinear combination model based on support vector machine for stock market prediction. In: Jinan C (ed) World congress on intelligent control and automation. IEEE, Piscataway, pp 5048–5053

Maknickiene N, Lapinskaite I, Maknickas A (2018) Application of ensemble of recurrent neural networks for forecasting of stock market sentiments. Equilib Q J Econ Econ Policy 13(1):7–27. https://doi.org/10.24136/eq.2018.001

Makrehchi M, Shah S, Liao W (2013) Stock prediction using event-based sentiment analysis. In: Proceedings—2013 IEEE/WIC/ACM international conference on web intelligence, WI 2013, 1, pp 337–342. https://doi.org/10.1109/wi-iat.2013.48

Malkiel BG (1999) A random walk down Wall Street: including a life-cycle guide to personal investing. WW Norton & Company

Metghalchi M, Kagochi J, Hayes LA (2014) Contrarian technical trading rules: evidence from Nairobi stock index. J Appl Bus Res 30(3):833–846

Ming F et al (2014) Stock market prediction from WSJ: text mining via sparse matrix factorization. In: EEE international conference on data mining, ICDM, pp 430–439. https://doi.org/10.1109/icdm.2014.116

Minxia L, Zhang K (2014) A hybrid approach combining extreme learning machine and sparse representation for image classification. Eng Appl Artif Intell 27:228–235. https://doi.org/10.1016/j.engappai.2013.05.012

Mittal A, Goel A (2012) Stock prediction using twitter sentiment analysis. Standford University, CS229, (June). https://doi.org/10.1109/wi-iat.2013.48

Mohapatra P, Raj A (2012) Indian stock market prediction using differential evolutionary neural network model. Int J Electron Commun Comput Technol: IJECCT 2(4):159–166

Murekachiro D (2016) A review of artificial neural networks application to stock market predictions. Netw Complex Syst 6(4):2010–2013

Naeini MP, Taremian H, Hashemi HB (2010) Stock market value prediction using neural networks. IEEE, Piscataway, pp 132–136

Nair BB et al (2010) Stock market prediction using a hybrid neuro-fuzzy system. In: International conference on advances in recent technologies in communication and computing, India, pp 243–247. https://doi.org/10.1109/artcom.2010.76

Nair BB, Mohandas VP, Sakthivel NR (2010) A decision tree-rough set hybrid system for stock market trend prediction. Int J Comput Appl 6(9):1–6

Nassirtoussi AK et al (2014) Text mining for market prediction: a systematic review. Expert Syst Appl 41(16):7653–7670. https://doi.org/10.1016/j.eswa.2014.06.009

Nayak RK, Mishra D, Rath AK (2015) A Naïve SVM-KNN based stock market trend reversal analysis for Indian benchmark indices. Appl Soft Comput J 35:670–680. https://doi.org/10.1016/j.asoc.2015.06.040

Nazário RTF et al (2017) A literature review of technical analysis on stock markets. Q Rev Econ Finance 66:115–126. https://doi.org/10.1016/j.qref.2017.01.014

Neelima B, Jha CK, Saneep BK (2012) Application of neural network in analysis of stock market prediction. Int J Comput Sci Technol: IJCSET 3(4):61–68

Nhu HN, Nitsuwat S, Sodanil M (2013) Prediction of stock price using an adaptive neuro-fuzzy inference system trained by firefly algorithm. In: 2013 international computer science and engineering conference, ICSEC 2013, pp 302–307. https://doi.org/10.1109/icsec.2013.6694798

Nikfarjam A, Emadzadeh E, Muthaiyah S (2010) Text mining approaches for stock market prediction. IEEE, vol 4, pp 256–260

Nisar TM, Yeung M (2018) Twitter as a tool for forecasting stock market movements: a short-window event study. J Finance Data Sci 4(February):1–19. https://doi.org/10.1016/j.jfds.2017.11.002

Olaniyi S, Adewole K, Jimoh R (2011) Stock trend prediction using regression analysis—a data mining approach. ARPN J Syst Softw 1(4):154–157

Paik P, Kumari B (2017) Stock market prediction using ANN, SVM, ELM: a review. Ijettcs 6(3):88–94. https://doi.org/10.1038/33071

Patel J et al (2015a) Predicting stock and stock price index movement using trend deterministic data preparation and machine learning techniques. Expert Syst Appl 42(1):259–268. https://doi.org/10.1016/j.eswa.2014.07.040

Patel J et al (2015b) Predicting stock market index using fusion of machine learning techniques. Expert Syst Appl 42(4):2162–2172. https://doi.org/10.1016/j.eswa.2014.10.031

Pervaiz J, Masih J, Jian-Zhou T (2018) Impact of macroeconomic variables on Karachi stock market returns. Int J Econ Finance 10(2):28. https://doi.org/10.5539/ijef.v10n2p28

Perwej Y, Perwej A (2012) Prediction of the Bombay stock exchange (BSE) market returns using artificial neural network and genetic algorithm. J Intell Learn Syst Appl 04(02):108–119. https://doi.org/10.4236/jilsa.2012.42010

Pimprikar R, Ramachadran S, Senthilkumar K (2017) Use of machine learning algorithms and Twitter sentiment analysis for stock market prediction. Int J Pure Appl Math 115(6):521–526

Porshnev A, Redkin I, Shevchenko A (2013) Improving prediction of stock market indices by analyzing the psychological states of Twitter users. Financ Econ. https://doi.org/10.2139/ssrn.2368151

Prem Sankar C, Vidyaraj R, Satheesh Kumar K (2015) Trust based stock recommendation system—a social network analysis approach. In: Procedia computer science: international conference on information and communication technologies (ICICT 2014). Elsevier Masson SAS, pp 299–305. https://doi.org/10.1016/j.procs.2015.02.024

Pulido M, Melin P, Castillo O (2014) Particle swarm optimization of ensemble neural networks with fuzzy aggregation for time series prediction of the Mexican stock exchange. Inf Sci 342(May):317–329. https://doi.org/10.1007/978-3-319-32229-2_23

Rajashree D, Dash PK, Bisoi R (2014) A self adaptive differential harmony search based optimized extreme learning machine for financial time series prediction. Swarm Evol Comput 19:25–42. https://doi.org/10.1016/j.swevo.2014.07.003

Rather AM, Agarwal A, Sastry VN (2014) Recurrent neural network and a hybrid model for prediction of stock returns. Expert Syst Appl 42(8):3234–3241. https://doi.org/10.1016/j.eswa.2016.05.033

Renu IR, Christie R (2018) Fundamental analysis versus technical analysis—a comparative review. Int J Recent Sci Res 9(1):23009–23013. https://doi.org/10.24327/IJRSR

Sasan B, Azadeh A, Ortobelli S (2017) Fusion of multiple diverse predictors in stock market. Inf Fusion 36:90–102. https://doi.org/10.1016/j.inffus.2016.11.006

Shen S, Jiang H, Zhang T (2012) Stock market forecasting using machine learning algorithms. Department of Electrical Engineering, Stanford University, Stanford, CA, pp 1–5

Sheta A, Farisy H, Alkasassbehz M (2013) A genetic programming model for S&P 500 stock market prediction. Int J Control Autom 6(6):303–314. https://doi.org/10.14257/ijca.2013.6.6.29

Shobana T, Umamakeswari A (2016) A review on prediction of stock market using various methods in the field of data mining. Indian J Sci Technol 9(48):9–14. https://doi.org/10.17485/ijst/2016/v9i48/107985

Shom P Das, Padhy S (2012) Support vector machines for prediction of futures prices in Indian stock market. Int J Comput Appl 41(3):22–26. https://doi.org/10.5120/5522-7555

Si J et al (2013) Exploiting topic based twitter sentiment for stock prediction. In: The 51st annual meeting of the association for computational linguistics, vol 2(2011), pp 24–29. http://www.scopus.com/inward/record.url?eid=2-s2.0-84907356594&partnerID=tZOtx3y1

Solanki H (2013) Comparative study of data mining tools and analysis with unified data mining theory. Int J Comput Appl 75(16):23–28

Soni S (2011) Applications of ANNs in stock market prediction: a survey. In: International conference on computer information systems and industrial management applications (CISIM), vol 2, no. 3, pp 132–136. https://doi.org/10.1177/1040638713493779

Sorto M, Aasheim C, Wimmer H (2017) Feeling the stock market: a study in the prediction of financial markets based on news sentiment. In: Hatzivassiloglou V, Klavans J, Eskin E (eds) Southern association for information systems conference. St. Simons Island, GA, USA, p. 19. http://aisel.aisnet.org/sais2017%0Ahttp://aisel.aisnet.org/sais2017/30%0Ahttp://aisel.aisnet.org/sais2017%0Ahttp://aisel.aisnet.org/sais2017/30

Stanković J, Marković I, Stojanović M (2015) Investment strategy optimization using technical analysis and predictive modeling in emerging markets. Procedia Econ Finance 19(15):51–62. https://doi.org/10.1016/S2212-5671(15)00007-6

Su CH, Cheng CH (2016) A hybrid fuzzy time series model based on ANFIS and integrated nonlinear feature selection method for forecasting stock. Neurocomputing 205:264–273. https://doi.org/10.1016/j.neucom.2016.03.068

Suhaibu I, Harvey SK, Amidu M (2017) The impact of monetary policy on stock market performance: evidence from twelve (12) African countries. Res Int Bus Finance 42(12):1372–1382. https://doi.org/10.1016/j.ribaf.2017.07.075

Sun A, Lachanski M, Fabozzi FJ (2016) Trade the tweet: social media text mining and sparse matrix factorization for stock market prediction. Int Rev Financ Anal 48:272–281. https://doi.org/10.1016/j.irfa.2016.10.009

Sureshkumar KK, Elango NM (2011) An efficient approach to forecast Indian stock market price and their performance analysis. Int J Comput Appl 34(5):44–49. https://doi.org/10.1196/annals.1364.016

Suthar BA, Patel RH, Parikh MS (2012) A comparative study on financial stock market prediction models. Int J Eng Sci: IJES 1(2):188–191. https://doi.org/10.1007/BF00629127

Talib R et al (2016) Text mining-techniques applications and issues. Int J Adv Comput Sci Appl 7(11):414–418

Thanh D Van, Minh Hai N, Hieu DD (2018) Building unconditional forecast model of stock market indexes using combined leading indicators and principal components: application to Vietnamese stock market. Indian J Sci Technol 11(2):1–13. https://doi.org/10.17485/ijst/2018/v11i2/104908

Ticknor JL (2013) A Bayesian regularized artificial neural network for stock market forecasting. Expert Syst Appl 40(14):5501–5506. https://doi.org/10.1016/j.eswa.2013.04.013

Tsai C-F, Hsiao Y-C (2010) Combining multiple feature selection methods for stock prediction: union, intersection, and multi-intersection approaches. Decis Support Syst 50(1):258–269. https://doi.org/10.1016/j.dss.2010.08.028

Tsai MF, Wang C-J (2017) On the risk prediction and analysis of soft information in finance reports. Eur J Oper Res 257(1):243–250. https://doi.org/10.1016/j.ejor.2016.06.069

Tsaurai K (2018) What are the determinants of stock market development in emerging markets? Acad Account Financ Stud J 22(2):1–11

Tziralis G, Tatsiopoulos I (2007) Prediction markets: an extended literature review. J Predict Mark 1:75–91

Umoru D, Nwokoye GA (2018) FAVAR analysis of foreign investment with capital market predictors: evidence on Nigerian and selected African stock exchanges. Acad J Econ Stud 4(1):12–20

Uysal AK, Gunal S (2014) The impact of preprocessing on text classification. Inf Process Manage 50:104–112

Vaisla SK, Bhatt KA (2010) An analysis of the performance of artificial neural network technique for stock market forecasting. Int J Comput Sci Eng 02(06):2104–2109

Vu T-T et al (2012) An experiment in integrating sentiment features for tech stock prediction in Twitter. In: Workshop on information extraction and entity analytics on social media data, pp 23–38. http://www.aclweb.org/anthology/W12-5503

Wang Y (2013) Stock price direction prediction by directly using prices data: an empirical study on the KOSPI and HSI, pp 1–13. https://doi.org/10.1504/ijbidm.2014.065091

Wang L, Qiang W (2011) Stock market prediction using artificial neural networks based on HLP. In: Proceedings—2011 3rd international conference on intelligent human-machine systems and cybernetics, IHMSC 2011, vol 1, pp 116–119. https://doi.org/10.1109/ihmsc.2011.34

Wanjawa BW (2016) Predicting future Shanghai stock market price using ANN in the period 21 Sept 2016 to 11 Oct 2016

Wanjawa BW, Muchemi L (2014) ANN model to predict stock prices at stock exchange markets. Nairobi

Wei LY (2016) A hybrid ANFIS model based on empirical mode decomposition for stock time series forecasting. Appl Soft Comput J 42:368–376. https://doi.org/10.1016/j.asoc.2016.01.027

Wei L-Y, Chen T-L, Ho T-H (2011) A hybrid model based on adaptive-network-based fuzzy inference system to forecast Taiwan stock market. Expert Syst Appl 38(11):13625–13631. https://doi.org/10.1016/j.eswa.2011.04.127

Wensheng D, Wu JY, Lu CJ (2012) Combining nonlinear independent component analysis and neural network for the prediction of Asian stock market indexes. Expert Syst Appl 39(4):4444–4452. https://doi.org/10.1016/j.eswa.2011.09.145

Xi L et al (2014) A new constructive neural network method for noise processing and its application on stock market prediction. Appl Soft Comput J 15:57–66. https://doi.org/10.4171/RLM/692

Yeh C-Y, Huang C-W, Lee S-J (2011) A multiple-kernel support vector regression approach for stock market price forecasting. Expert Syst Appl 38(3):2177–2186. https://doi.org/10.1016/j.eswa.2010.08.004

Yetis Y, Kaplan H, Jamshidi M (2014) Stock market prediction using artificial neural network. In: World Automation Congress. ISI Press, pp 1–5. https://doi.org/10.5120/17399-7959

Yifan L et al (2017) Stock volatility prediction using recurrent neural networks with sentiment analysis. https://doi.org/10.1007/978-3-319-60042-0_22

Yoosin K, Seung RJ, Ghani I (2014) Text opinion mining to analyze news for stock market prediction. Int J Adv Soft Comput Appl 6(1–13):44. https://doi.org/10.1016/S0399-077X(16)30365-1

Yu H, Liu H (2012) Improved stock market prediction by combining support vector machine and empirical mode decomposition. In: 2012 5th international symposium on computational intelligence and design, ISCID 2012, pp 531–534. https://doi.org/10.1109/iscid.2012.138

Zhang X, Fuehres H, Gloor PA (2011) Predicting stock market indicators through Twitter “I hope it is not as bad as I fear”. Procedia Soc Behav Sci 26(2007):55–62. https://doi.org/10.1016/j.sbspro.2011.10.562

Zhang X et al (2014) A causal feature selection algorithm for stock prediction modeling. Neurocomputing 142:48–59. https://doi.org/10.1016/j.neucom.2014.01.057

Zhang X et al (2017) Improving stock market prediction via heterogeneous information fusion. Knowl Based Syst 143:236–247. https://doi.org/10.1016/j.knosys.2017.12.025

Zhou Z, Xu K, Zhao J (2017) Tales of emotion and stock in China: volatility, causality and prediction. https://doi.org/10.1007/s11280-017-0495-4

Zhou X et al (2018) Stock market prediction on high frequency data using generative adversarial nets. Math Probl Eng 2018:1–12. https://doi.org/10.1155/2018/4907423

Download references

The declare that they have not received any funding or Grant for this work.

Author information

Authors and affiliations.

Department of Computer Science, Sunyani Technical University, Sunyani, Ghana

Isaac Kofi Nti

Department of Computer Science and Informatics, University of Energy and Natural Resources, Sunyani, Ghana

Isaac Kofi Nti, Adebayo Felix Adekoya & Benjamin Asubam Weyori

You can also search for this author in PubMed Google Scholar

Corresponding author

Correspondence to Isaac Kofi Nti .

Ethics declarations

Conflict of interest.

The authors declare that they have no conflict of interest.

Ethical approval

This article does not contain any studies with human participants or animals performed by any of the authors.

Additional information

Publisher's note.

Springer Nature remains neutral with regard to jurisdictional claims in published maps and institutional affiliations.

See Tables 2 , 3 , 4 , 5 , 6 and 7 .

Rights and permissions

Reprints and permissions

About this article

Nti, I.K., Adekoya, A.F. & Weyori, B.A. A systematic review of fundamental and technical analysis of stock market predictions. Artif Intell Rev 53 , 3007–3057 (2020). https://doi.org/10.1007/s10462-019-09754-z

Download citation

Published : 20 August 2019

Issue Date : April 2020

DOI : https://doi.org/10.1007/s10462-019-09754-z

Share this article

Anyone you share the following link with will be able to read this content:

Sorry, a shareable link is not currently available for this article.

Provided by the Springer Nature SharedIt content-sharing initiative

- Machine-learning

- Stock-prediction

- Artificial intelligence

- Technical-analysis

- Fundamental-analysis

- Find a journal

- Publish with us

- Track your research

Central Banks, Stock Markets, and the Real Economy

This article summarizes empirical research on the interaction between monetary policy and asset markets, and reviews our previous theoretical work that captures these interactions. We present a concise model in which monetary policy impacts the aggregate asset price, which in turn influences economic activity with lags. In this context: (i) the central bank (the Fed, for short) stabilizes the aggregate asset price in response to financial shocks, using large-scale asset purchases if needed ("the Fed put"); (ii) when the Fed is constrained, negative financial shocks cause demand recessions, (iii) the Fed's response to aggregate demand shocks increases asset price volatility, but this volatility plays a useful macroeconomic stabilization role; (iv) the Fed's beliefs about the future aggregate demand and supply drive the aggregate asset price; (v) macroeconomic news influences the Fed's beliefs and asset prices; (vi) more precise news reduces output volatility but heightens asset market volatility; (vii) disagreements between the market and the Fed microfound monetary policy shocks, and generate a policy risk premium.

When citing this paper, please use the following: Caballero RJ, Simsek A. 2024. Central banks, stock markets, and the real economy. Annu. Rev. Financ. Econ. 16. In press. DOI: https://doi.org/10.1146/annurev-financial-082123-105900. Vicente Jimenez provided outstanding research assistance. Caballero acknowledges support from the National Science Foundation (NSF) under Grant Number SES-1848857. The views expressed herein are those of the authors and do not necessarily reflect the views of the National Bureau of Economic Research.

MARC RIS BibTeΧ

Download Citation Data

- Dynamic link to the most recent draft

More from NBER

In addition to working papers , the NBER disseminates affiliates’ latest findings through a range of free periodicals — the NBER Reporter , the NBER Digest , the Bulletin on Retirement and Disability , the Bulletin on Health , and the Bulletin on Entrepreneurship — as well as online conference reports , video lectures , and interviews .

Rigorous primary research

A framework for allocating to cash: risk, horizon, and funding level

A Rational Multi-Asset Portfolio Rebalancing Decision-Making Framework

Resilient Liquidity: The Robust Reaction of Equity Volume and Spreads to Market Volatility

Filter by topic

Sort by date

Financial wellness & planning

May 26, 2022

For many families, planning for college costs is a top financial priority. A Byzantine landscape of consumer choices, loans, tuition discounting, and public and private aid, however, makes it difficult to answer key questions like "How much will this cost us?” This is especially so for young families, for whom future spending needs are necessarily vague. Vanguard researchers explore how understanding the dynamics of financial aid and net pricing can help parents set a realistic savings target early on and shape a savings plan that evolves with them.

Portfolio considerations

May 20, 2022

A number of factors have fueled the growth of index investing around the world. “The case for low-cost index-fund investing,” a newly revised research paper from Vanguard’s Investment Strategy Group, explores these factors. The paper discusses why the authors expect that index investing will continue to be effective over the long term.

April 14, 2022

The past few decades were a good time for spending from a retirement portfolio. What about the next 30 years? The apparent shifts in capital market conditions seen since the start of 2022 led us to examine sustainable withdrawal rates. Looking at historical return environments our authors developed three scenarios, with rates from 2.8% to 3.3%.

April 13, 2022

Vanguard believes private corporate pension plans should consider a liability-driven investing (LDI) program in the fixed income portion of their portfolio. Based on our analysis, a customized mix of U.S. investment-grade credit bonds and Treasuries aligns well with that liability. Such a mix has historically helped plan sponsors mitigate risk.

March 29, 2022

Personalized indexing (PI) is a flexible portfolio management solution that can track a personalized index and harvest capital losses for tax-saving purposes. This paper presents a portfolio construction plan using PI, touching on how to optimally implement tax-loss harvesting and allocate to PI in the presence of other assets.

August 10, 2022

Investors typically decide whether to convert to a Roth IRA from a traditional IRA by comparing their current and expected future marginal tax rates. The traditional wisdom has been that higher future tax rates make conversion more desirable and lower ones make it less so. Vanguard researchers describe a break-even tax rate (BETR) that yields a more accurate view of what future tax rate would make an investor indifferent to a conversion.

March 15, 2022

New Vanguard research indicates that investors are frequently using non-total market index funds to build portfolios with active exposures, according to “How investors use passive for active,” a paper authored by Vanguard’s Jan-Carl Plagge, Haifeng Wang, and Jim Rowley. The paper was published in The Journal of Beta Investment Strategies .

Behavioral research

February 23, 2022

Investors prefer some aspects of human advice over digital but perceive value in all advice services. Technology can help human advisors scale their businesses while strengthening their uniquely human value proposition.

February 02, 2022

Vanguard shares our current views on best practices for U.S. private-sector pension plan asset allocation. We highlight the value of identifying three targets—the return-seeking asset allocation, interest rate hedge ratio, and credit spread hedge ratio—that can be the foundation for a robust, customized portfolio construction process.

December 15, 2021

Retirees often eschew investing for total returns, relying instead on dividends and interest from high-income-producing assets to support spending from ad hoc portfolios. We introduce a method for building high-income portfolios that maximize the investor’s utility of wealth based on total returns while accounting for yield preferences.

Economics & markets

December 13, 2021

Our annual forecast explains why we expect the global economy to slow, leaving full-year 2022 growth, in our base case, of 4.8%. It also explains why our 10-year market outlook is guarded, as reflected in the low-single-digit range of expected returns for a globally diversified, 60% stock/40% bond portfolio.

November 19, 2021

Tax-loss harvesting (TLH) has been promoted as a “free lunch” for increasing investment returns. Vanguard researchers explore the potential for TLH and demonstrate how to customize a TLH strategy for optimal benefits. A case study is also featured that illustrates how the benefits of TLH can vary considerably from investor to investor.

November 15, 2021

Historically low yields on most global fixed income investments are likely to result in low returns over the next decade, leading some investors to question the allocation to bonds in multi-asset portfolios. In this paper, Vanguard researchers demonstrate the value of bonds as “shock absorbers” for portfolios when equity markets are under stress.

October 29, 2021

This paper examines the effect of automatic escalation on defined contribution plan contribution rates and provides insights into plan designs that maximize participants’ chance of savings at rates necessary for a secure retirement. The motivations of participants to override automatic deferral rates and annual increases are also explored.

October 11, 2021

This study explores how factoring in health care cost uncertainty can benefit retirement planning by enabling the development of more customized plans. Vanguard researchers employ a stochastic health care model to offer more realistic insights into how longevity and health care-related risks affect the viability of spending plans in retirement.

September 08, 2021

Growth in pension liabilities, along with new disclosure requirements and market-based accounting standards, have led defined benefit pension plan sponsors to consider corporate finances as they manage their plans. This paper discusses how pension plan risk can affect corporate finances and the strategies sponsors can use to mitigate that risk.

October 08, 2021

Parents and students face distinct challenges when financing higher education expenses. This research paper discusses financial aid options, tax credits, and 529 savings plans and other savings vehicles, as well as the need to plan strategically and understand how college spending decisions affect one's broader financial situation.

September 28, 2021

With interest rates and inflation expected to rise, the negative stock/bond correlation that supports the diversification properties of a balanced portfolio could also be at risk. In this paper, researchers find that negative correlation will continue and the diversification benefits of a 60% stock/40% bond portfolio will persist.

Vanguard’s Megatrends series examines fundamental shifts in the global economic landscape that are likely to affect the financial services industry and broader society. In this edition, Vanguard researchers explore China’s future as an economic powerhouse and its broad implications for global growth, geopolitics, and financial markets.

September 23, 2021

Vanguard’s Megatrends series examines fundamental shifts in the global economic landscape that are likely to affect the financial services industry and broader society. In this paper, Vanguard economists examine global trade growth and conclude that growth will likely slow, as it has since the global financial crisis, but not decline.

September 13, 2021

Vanguard researchers classify the economic and market environment into five states: recession, recovery, expansion, slowdown, and high inflation. This paper discusses the characteristics, valuations, and return expectations of each and concludes that investors willing to take on active risk should adopt a dynamic, state-dependent approach.

Amid a backdrop of highly accommodative monetary and fiscal policies, how likely are persistently higher rates of inflation in the United States for 2022 and beyond? In this paper, Vanguard researchers present the findings of Vanguard’s state-of-the-art forecasting model to project core inflation over the next two years.

August 30, 2021

Employing machine-learning, Vanguard researchers found that government bonds have historically acted as a counterbalance in an equity/bond portfolio during low-rate periods. Although in some months both equities and bonds fall, the analysis suggests that this can be thought of as market noise and distinctly different from typical outcomes.

Most target-date fund series offer a single post-retirement asset allocation designed to help retirees replace a reasonable portion of pre-retirement income. In this paper, Vanguard researchers offer a framework demonstrating that adding a second asset allocation could support additional goals for those with the resources and desire to pursue them.

A Vanguard survey shows that most investors underestimate the risk of mild cognitive impairment. In addition, while most respondents had some plans to mitigate the effects of cognitive decline, they were less likely to focus on the transfer of control of their finances, the timing of which can have significant implications for financial well-being.

August 05, 2021